Tesla says price drops are long-term thinking, but it’s really about demand

Tesla has just released its Q1 2023 earnings report amidst several price drops since the beginning of the year. This left investors questioning how these drops would affect margins, and Tesla has an explanation, but it’s perhaps only a partial one.

In a nod to the question on everyone’s lips, Tesla’s earnings report starts off immediately with a couple of paragraphs intended to address the effect of these price drops on its industry-high margins.

In the current macroeconomic environment, we see this year as a unique opportunity for Tesla. As many carmakers are working through challenges with the unit economics of their EV programs, we aim to leverage our position as a cost leader. We are focused on rapidly growing production, investments in autonomy and vehicle software, and remaining on track with our growth investments.

Although we implemented price reductions on many vehicle models across regions in the first quarter, our operating margins reduced at a manageable rate. We expect ongoing cost reduction of our vehicles, including improved production efficiency at our newest factories and lower logistics costs, and remain focused on operating leverage as we scale.

Tesla is pointing out that since its EV volume is so drastically higher than every other automaker’s, it can build cars at a lower cost than the competition.

And indeed, after yesterday’s price drops and other even larger price drops earlier this year, Tesla has gone from being near the top of the EV price range to near the bottom. Last year, Tesla repeatedly hiked prices while the industry faced supply challenges and EV demand well exceeded supply.

After tax credits, the base Model Y is now under $40k, while many electric SUVs have higher starting prices. And the base Model 3 is now available for $40k before credits are taken into account, though it now only qualifies for $3,750 due to the IRS’ new battery guidelines.

Tesla points out that these cuts reduced its margins but says that this margin reduction happened at a “manageable rate.” In Q1 last year, Tesla’s operating margin was 19.2%, and this year it’s 11.4%, a drop of 779 basis points.

This is a big chunk, cutting operating margins almost in half – and note that there have been further price cuts, both in the US and elsewhere, since the end of the quarter. So we could expect average selling prices to go down further in next quarter’s earnings and perhaps another cut to margins.

That said, Tesla is still planning to grow production at a CAGR of 50%, guiding for 1.8 million deliveries next year (about 31% growth from last year’s 1.37 million production). Tesla says it would rather focus on high volume and lower margins.

And it should be noted that higher volume also displaces more gas vehicles, which is better for the environment and public health.

There are other reasons for these price drops. For one, costs have come down, particularly with a massive global drop in the costs of resources like lithium after last year’s massive global spike. Also, as Tesla CEO Elon Musk has pointed out, rising interest rates have made it more expensive to get a loan on a car, which means Tesla has had to lower prices to make purchases seem more attractive (this is a case study in how rising interest rates can lower inflation).

But Tesla claims these margin cuts are manageable, and not only that, the company is taking a long-term view:

Our near-term pricing strategy considers a long-term view on per vehicle profitability given the potential lifetime value of a Tesla vehicle through autonomy, supercharging, connectivity and service. We expect that our product pricing will continue to evolve, upwards or downwards, depending on a number of factors.

Here, Tesla says that despite the vast majority of its revenue coming from sales of cars – in Q1, $19.9b came from cars and only $3.3b came from energy, services, and other – it feels confident that any losses in automotive sales revenue will be made up for in the long term by these other revenue categories.

Tesla currently sells access to its FSD Beta software for an eye-watering $15,000. This is an enormous chunk of change, particularly for a car that sells for $40k new. Tesla CEO Elon Musk has claimed that FSD has enormous value, though most who have used it recognize that it’s definitely not ready for primetime yet. Perhaps this is why timelines for its rollout keep getting pushed back. (Is it next year yet?)

Tesla also mentions Supercharging as a potential revenue center. Right now, Tesla doesn’t make a lot of money on Supercharging, but that may change very soon, as the company has started opening up Superchargers to other brands. Tesla used this opportunity to establish the “North American Charging Standard” using its connector, claiming that, since its connector is on the majority of cars and DC chargers in North America, other automakers should follow Tesla’s lead and use its plug.

This also opens the company up to the availability of billions of federal dollars earmarked for charger installation but which can only be used on chargers that are open to multiple brands of car. Until recently, only Teslas could use Superchargers, but now that they’re open to other cars, Tesla can presumably angle for some of those billions.

Finally, Tesla says that service could be a profit center, a big change from Musk’s original philosophy on the topic. Here’s a video from Tesla’s 2013 shareholder meeting, timestamped to 1:36 when his answer on service begins:

Clearly, things have changed since then, and Tesla is much larger and has different goals and considerations now than before. But in the context of discussing auto dealerships, with which Tesla is still in a battle, one would think that this overarching “philosophy” would not have changed with transient business conditions.

Nevertheless, this is one way in which Tesla could conceivably offer reduced upfront prices, with the hopes that the continual business of servicing vehicles in the field would help to shore up margins. Most other automakers don’t have this option since they don’t own their dealerships, but Tesla does, which gives it the flexibility to capture this portion of revenue. It sounds like the company now explicitly intends to seek this revenue after originally promising not to.

Electrek’s Take

But there’s another reason that Tesla doesn’t mention in its report: demand.

I know; we’ve heard it before. For the last decade, other automakers, media, incumbent industry, oil companies, captured regulators, and so on have all said that there just isn’t enough EV demand. We’ve called them wrong every time, and they’ve been wrong every time.

But specifically, here, we’re talking about demand solely for Tesla, after the huge price hikes that the company engaged in over the course of 2021 and 2022 and amid questionable public behavior by the CEO.

At the time when Tesla was raising prices, EV demand was very high, and EV supply was very low. This gave Tesla, the company with the most EV supply, significant pricing power.

Now, we still have high global EV demand, with many other brands selling out vehicles while gas cars go unsold. But in the US, we have an ever-changing tax credit environment, with some new rules going into place yesterday. This means there’s a lot of shifting happening in the industry, and it’s hard to predict which models will have the most demand as only some qualify for the tax credit (however, you can bypass most restrictions by leasing).

And while Tesla is mostly on the good side of this – its cars are now much lower in price, and most of them qualify for credits – it also has a ton of supply, is continuing to ramp quickly, and may be alienating potential customers.

Anecdotally (and in data), CEO Musk’s recent behavior related to the Twitter “dumpster fire” he keeps burning his money in has affected the company’s reputation. Musk says that TSLA shareholders will benefit in the long term from all the irrelevant nonsense he’s very publicly getting himself into, but we are not convinced.

So between high prices, erratic behavior from the CEO, and availability of other EV models, customers have perhaps looked elsewhere over the last year. As a result, Tesla’s inventory started to grow in a way that the company hasn’t ever really dealt with before, and it had to start pulling demand levers. It first did this with incentives, but this year has focused instead on large price drops.

Those price drops will definitely be able to bring some customers back, but it remains to be seen if some customers were permanently turned off by the high-profile behavior of the CEO.

FTC: We use income earning auto affiliate links. More.

After recently launching its newest electric scooter, the Gogoro JEGO Smartscooter, deliveries of the hot-selling electric scooters are ready to begin. This marks a new page for Gogoro, the world’s largest battery-swapping network operator, and makes swappable battery electric scooters more affordable than ever.

The Gogoro JEGO launched in Taiwan last month, quickly racking up over 6,500 fully-paid pre-orders in that short time.

Gogoro already dominates the local market with around a 90% share of new electric scooter registrations in Taiwain. According to Gogoro, JEGO sales are showing the strongest demand for a Gogoro vehicle since the beginning of the pandemic. The company’s domestic market of Taiwan is by far its largest, though Gogoro scooters and battery swapping stations have now expanded to much of Asia as Gogoro expands its footprint.

With an introductory price that drops as low as just US $760 after government subsidies, the JEGO is positioned as an affordable new model to open up the local market further and entice more price-sensitive combustion engine scooter riders.

The scooter was built around Gogoro’s well-known battery standard, allowing one or two battery packs to power the vehicle around cities and urban areas. Riders buy the scooter but don’t own the batteries, instead subscribing to a swapping plan. That helps reduce the price of the scooter further and ensures Gogoro can get the longest life out of the batteries possible via intelligent charging and swapping doctrines. Having started its swapping programs back in 2015, Gogoro has learned that its batteries are lasting even longer than originally anticipated, with a new estimated lifespan of around 12 years.

An affordable new battery-swapping subscription plan was also announced along with the JEGO, offering new riders a US $7/month plan to cover up to 1,000 km (621 miles) of riding per month when signing up for a three-year plan.

The JEGO’s goal of converting existing combustion engine scooter riders over to electric seems to be working well.

“JEGO has touched a positive chord with a new market segment of Taiwan riders – nearly all of our 6,500 pre-order customers are first-time EV riders. They are looking for a smart, convenient, and sustainable vehicle and are not just embracing JEGO’s innovation and design but also access to Gogoro’s vast battery-swapping network,” said Horace Luke, founder and CEO of Gogoro. “Initial JEGO sales are surpassing our expectations and showing the strongest demand we’ve seen since the beginning of the pandemic. With deliveries beginning this week, we expect to realize JEGO’s pre-order revenue this quarter.”

At the same time as Gogoro expands its entry-level offering with the JEGO, Gogoro is also preparing for the rollout of its recently revealed premium-level Gogoro Pulse. That high-performance model, which also uses the same Gogoro swappable battery packs, includes a number of automotive-style features never before seen in the electric scooter market.

The dual-pronged approach reveals Gogoro’s ability to innovate on both ends of the market, serving both entry-level riders and higher-performance enthusiasts.

FTC: We use income earning auto affiliate links. More.

Listen to a recap of the top stories of the day from Electrek. Quick Charge is now available on Apple Podcasts, Spotify, TuneIn and our RSS feed for Overcast and other podcast players.

New episodes of Quick Charge are recorded Monday through Thursday and again on Saturday. Subscribe to our podcast in Apple Podcast or your favorite podcast player to guarantee new episodes are delivered as soon as they’re available.

Stories we discuss in this episode (with links):

Tesla may start selling its Optimus humanoid robot next year, says Elon Musk

Tesla is in talks with ‘one major automaker about licensing Full Self-Driving’

BETA hits its latest eVTOL milestone, transitioning mid-air with a pilot onboard [Video]

Tesla announces change of plans to build cheaper electric cars

Tesla teases its upcoming Uber-like self-driving ride-hailing app

Listen & Subscribe:

Share your thoughts!

Drop us a line at tips@electrek.co. You can also rate us in Apple Podcasts or recommend us in Overcast to help more people discover the show!

FTC: We use income earning auto affiliate links. More.

You’re reading Electrek— experts who break news about Tesla, electric vehicles, and green energy, day after day. Be sure to check out our homepage for all the latest news, and follow Electrek on Twitter, Facebook, and LinkedIn to stay in the loop. Don’t know where to start? Check out our YouTube channel for the latest reviews.

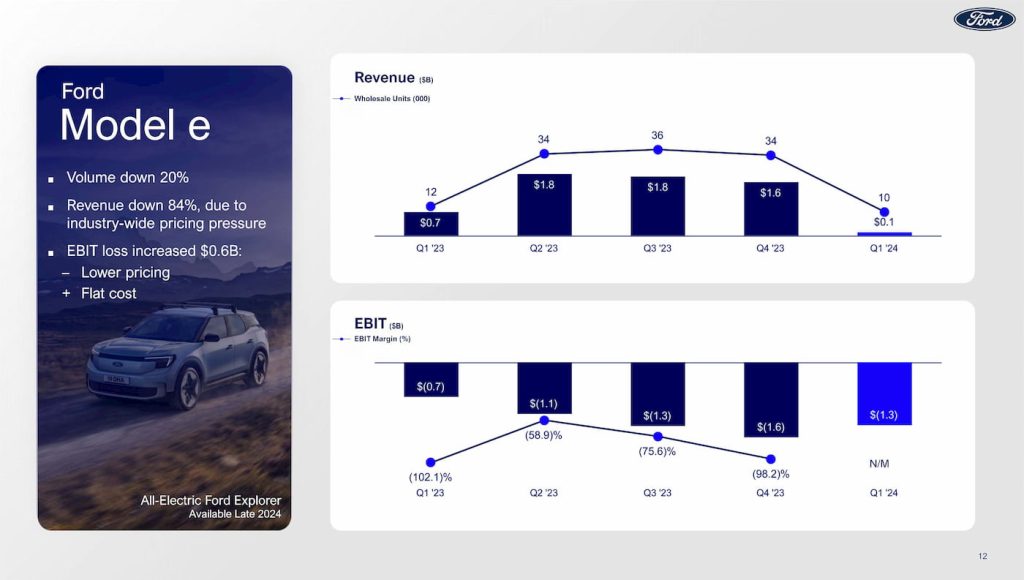

Amid a shifting strategy, Ford (F) reported first-quarter earnings Wednesday, beating analyst expectations. However, due to fierce pricing pressure, Ford’s EV revenue fell 84% in Q1 2024.

Ford shifts EV strategy amid sales upswing

Despite EV sales surging 86% to 20,233 in the first three months of 2024, Ford is pulling back. All Ford electric models saw double (or triple) digit sales growth.

The F-150 Lightning remained the top-selling electric pickup in the US, with 7,743 models sold, up 80% over last year. Ford’s Mustang Mach-E was the second best-selling electric SUV in the US, with 9,589 vehicles delivered, up 77% over Q1 2023.

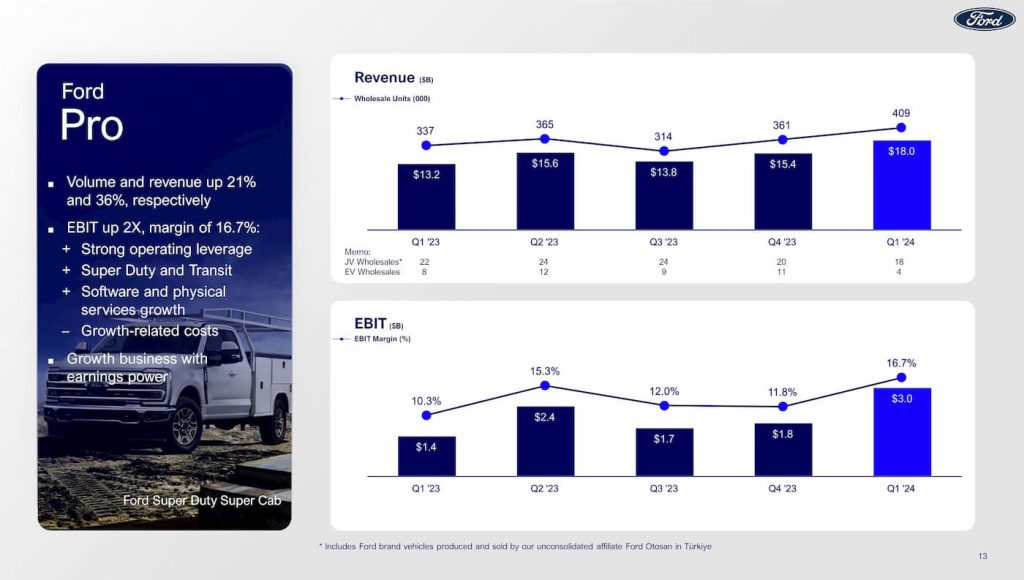

Meanwhile, Ford’s commercial Pro unit continues to appear as a dark horse for the automaker, with EV adoption rising 40%. Ford E-Transit sales were up 148% in Q1, with 2,891 units sold.

Ford’s growth propelled it to second in the US EV market (if you don’t include combined Hyundai and Kia sales).

The sales surge comes after Ford introduced significant price cuts and savings on the Mach-E and Lightning earlier this year.

Despite rising EV sales, Ford announced it is pushing back EV production at its BlueOval City facility to 2026. It is also delaying the launch of its three-row electric SUV to focus on smaller, more affordable EVs.

In the meantime, Ford said it would introduce more hybrids to the mix as it develops its next-gen electric models.

Ford’s Model e EV unit had a net loss of around $4.7 billion last year with “extremely competitive pricing” and new investments. Meanwhile, EBIT loss slipped to $1.6 billion in Q4.

Analysts expect Ford to report $40.10 billion in revenue in its Q1 2024 earnings report. Ford’s Model e, EV unit, is expected to generate around $24.5 billion in revenue with an EBIT loss of $1.65.

Ford Q1 2024 earnings results

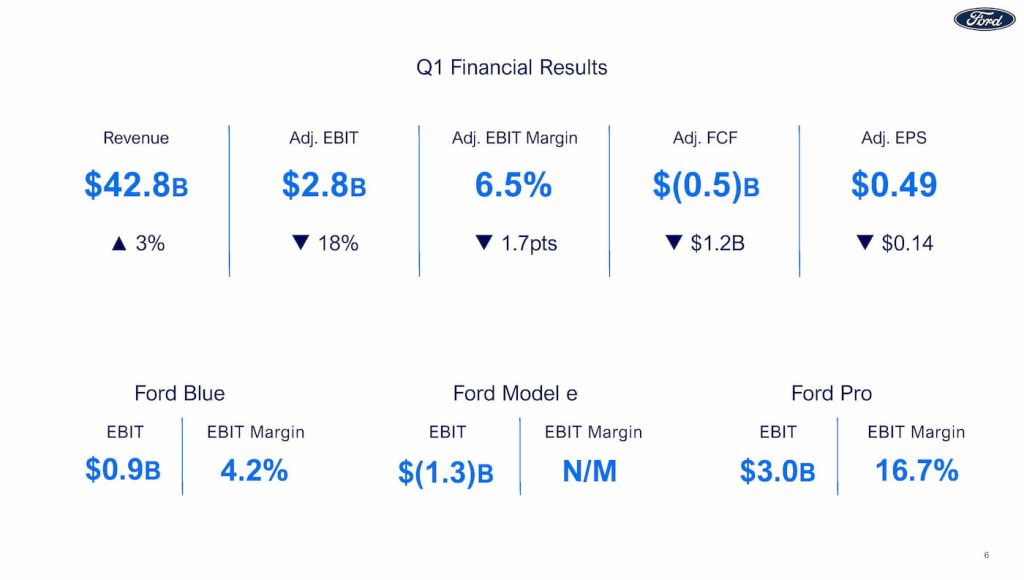

Ford reported first-quarter 2024 revenue rose 3% to $42.8 billion, topping estimates of around $40.10 billion. Ford also topped adjusted EPS estimates with $0.49 per share in Q1 vs $0.42 expected.

The automaker posted net income of $1.3 billion, down from $1.8 billion last year. Adjusted EBIT fell 18% to $2.8 billion due to lower prices and the timing of the F-150 launch.

Ford Blue, the company’s ICE business, saw revenue fall 13%, again due to the new F-150 launch.

Ford Pro was the growth driver, with volume and revenue up 21% and 36%, respectively. The commercial and software business had an EBIT margin of nearly 17%, with first-quarter revenue of $18 billion.

Meanwhile, Ford Model e revenue slipped 84% due to “industry-wide” pricing pressure. With lower prices, the unit’s EBIT loss increased YOY to $1.3 billion. That’s about a $64,000 loss for every EV sold in Q1. However, this is still down from the $1.6 billion EBIT loss in Q4 2023.

Ford expects EV costs to improve going forward, but it will be offset by top-line pressure.

The automaker is maintaining full-year EBIT guidance, expecting to hit the higher end of the $10 billion to $12 billion range. The company now expects to generate between $6.5 billion and $7.5 billion in adjusted free cash flow, up from the previous $6 billion to $7 billion.

According to Ford, the updates reflect recent cost-cutting actions, like the delayed EV investments. Ford’s update comes after rival GM also raised full-year guidance this week.

Meanwhile, Ford is releasing a new brand campaign called “Freedom of Choice” to promote its gas, hybrid, and EV lineup amid the strategy shift.

FTC: We use income earning auto affiliate links. More.

-

Sports2 years ago

Sports2 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Environment11 months ago

Environment11 months agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports3 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports6 months ago

Sports6 months agoGame 1 of WS least-watched in recorded history

-

Environment1 year ago

Environment1 year agoGame-changing Lectric XPedition launched as affordable electric cargo bike

-

Technology3 years ago

Game consoles were once banned in China. Now Chinese developers want a slice of the $49 billion pie

-

Politics2 years ago

Have the last few wobbly weeks seen a turning point for Johnson as PM?