World

Business Secretary Grant Shapps hints at autumn budget windfall tax expansion on energy firms due to ‘unexpected profits’

Business Secretary Grant Shapps has hinted that the government may extend the windfall tax on oil and gas companies in this month’s autumn budget as it tries to stabilise the UK’s public finances.

Speaking to Sky News with just 10 days to go before the government’s fiscal plans are unveiled, Mr Shapps said: “I mean, it is the case that because fuel prices have been so high, there have been unexpected profits, of course.

“But I think it’s important that we do carry on investing in making sure not on fossil fuels, but on the renewable energy as well, that we’ve we’ve got the capacity, we’ve got the ability to get that market moving as well.”

Sunak to raise migrant crossings with Macron – Politics latest

He added that the general public will “have to wait until the 17th” to know exactly which measures the government is going to pursue to tackle what the Resolution Foundation thinktank has said is a £40bn financial black hole.

Last week, an initial report in The Times suggested that Prime Minister Rishi Sunak and Chancellor Jeremy Hunt were planning to extend windfall taxes on oil and gas companies to raise an estimated £40bn over five years.

Mr Sunak and Mr Hunt want to maximise revenues from the windfall tax by increasing the rate from 25% to 30%, extending the policy until 2028, and expanding it to cover electricity generators – according to the paper.

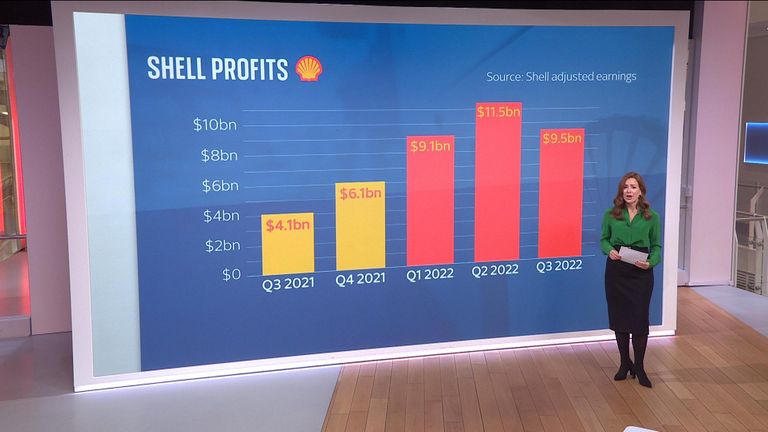

With BP unveiling profits that doubled to more than £7.1bn in the three months to September, pressure is continuing to mount for an enhanced windfall tax on oil and gas giants to help fill the Treasury coffers.

COP26 president Alok Sharma, who was demoted from the cabinet by Mr Sunak, has backed the move, saying: “We need to raise more money from a windfall tax on oil and gas companies and actively encourage them to invest in renewables.”

The Resolution Foundation said in a report last week that tax raises are “likely” to come soon as the government faces an “unpalatable menu” to find ways to re-balance the nation’s finances after former chancellor Kwasi Kwarteng’s ill-fated economic plans.

A combination of tax rises and spending cuts is likely to find the £40bn needed, it said.

Mr Sunak and Mr Hunt are currently figuring out how to tackle the abysmal economic forecast ahead of the autumn statement on 17 November, which was pushed back soon after Mr Sunak reappointed Mr Hunt.

Why do Shell’s profits matter?

The Resolution Foundation’s report added that a recession next year could be predicted by the government’s independent forecaster, the Office for Budget Responsibility.

Last week, the Bank of England raised its official interest rates by 0.75 percentage points to 3% and said the UK was already in recession.

It was the single biggest increase in more than three decades.

While GDP forecasts could be cut by up to 4% by the end of 2024.

BoE interest rate hike explained

The autumn statement this month will likely encompass “rough” tax rises, Sky News has been told by a source in the Treasury.

The tax rises are likely to be across the board, although Mr Sunak and Mr Hunt are said to have agreed those with the “broadest shoulders” should bear the greatest burden, it is understood.

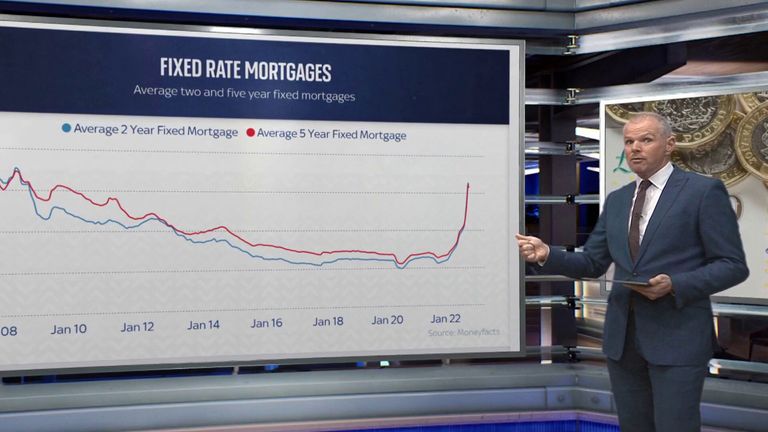

Read more: Demand for mortgages falls as customers grapple with high interest rates

Few concrete details have emerged but, according to The Times, public sector workers could face deep real-terms cuts to wages, with the Treasury reportedly looking at an increase of 2% across the board for 2023-24, at a time when inflation is expected to be well above that threshold.

The Resolution Foundation has said £9bn could be saved by the government choosing not to raise benefits and pensions in line with rising prices next year, but any such move would have a “huge” impact on those already struggling to make ends meet.

Another option would be to re-instate the health and social care levy to raise £15bn by 2026-2027, while around £2bn could be raised by extending the “stealth” freezes in income tax threshold by a further year to 2026-2027.