Borrowing is falling but Sunak faces the most challenging situation for a chancellor in decades

During the last 17 months we have become almost inured to the terrifying increases in government borrowing incurred in grappling with the pandemic.

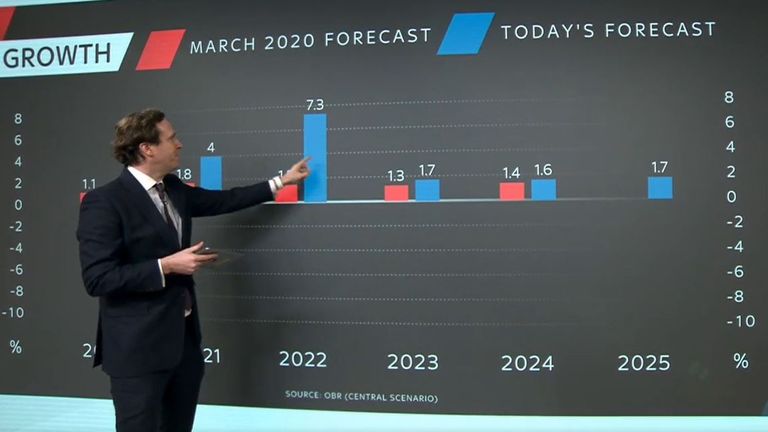

The government borrowed £303bn during the 2020-21 financial year, a peacetime record, equivalent to 14.5% of UK GDP.

Yet something interesting has been happening during the current financial year.

Tax burden to reach highest level since 1960s

In each of the first four months government borrowing, while still high, has come in significantly below the levels forecast by the independent Office for Budget Responsibility (OBR).

The latest figures for the public sector finances, published today, revealed that the government borrowed £10.4bn in July.

Make no mistake, this is still a terrifyingly high number, equivalent to borrowing of nearly £233,000 every minute.

It was, however, £10.1bn less than in July last year – and also significantly lower than the £11.8bn that City economists had been expecting.

The figure means that, during the first four months of the current financial year, the government borrowed £78bn – some £26bn less than the OBR had been forecasting at this stage.

There are a couple of key points to make about the numbers.

July’s figures are normally boosted by self-assessed tax returns

First of all, July is usually a strong month for tax receipts and therefore the public finances, because it is one of two months in the year – the other is January – in which the deadline falls due for payments by those completing self-assessed tax returns.

It was not unusual, pre-pandemic, for the government to record a surplus during July.

That appears to have been a key factor this month.

The government enjoyed tax receipts of £70bn during July – up £9.5bn on the same month last year.

Behind that was a £3.7bn improvement in self-assessed tax receipts on the same month last year, when HMRC allowed tax payments to be deferred, chiefly to support the self-employed.

But it probably also reflects that the economy is starting to recover.

VAT receipts were up by £1.2bn on July last year, fuel duty was up by £400m – partly reflecting higher petrol and diesel prices – and regular income tax payments were up by £800m.

There was also a big jump in stamp duty receipts, which at £1.4bn were double the level they were in July last year, reflecting a rush to beat the deadline for the end of the temporary £500,000 nil-rate band.

Fuel duty was up by £400m

Receipts from corporation tax, which is levied on company profits, also came in higher than the OBR had been expecting.

Secondly, government spending was lower, with the government shelling out £79.8bn during the month.

That was down £2.9bn on July last year and probably reflects that, not only did the government begin to taper away its furlough scheme, but also that there were fewer workers participating in the scheme.

Government spending on the furlough scheme during July was down £4.2bn on the same month last year while spending on the equivalent scheme for the self-employed was down £200m.

Worryingly, though, interest payments on the national debt came in at £3.4bn during the month – up £1.1bn on July last year.

As for the national debt, that stood at £2.216trn at the end of July, equivalent to 98.8% of GDP, which the Office for National Statistics (ONS) said was the highest it has been since March 1962.

The figures were welcomed by Rishi Sunak, the chancellor, who has been spelling out the need to restore order to the public finances.

He said: “Our recovery from the pandemic is well under way, boosted by the huge amount of support government has provided.

A rise in stamp duty receipts reflected a rush to complete deals before the winding down of a stamp duty holiday

“But the last 18 months have had a huge impact on our economy and public finances, and many risks remain.

“We’re committed to keeping the public finances on a sustainable footing, which is why at the budget in March I set out the steps we are taking to keep debt under control in the years to come.”

That is not to say the chancellor faces anything other than a major challenge on that front.

Isabel Stockton, research economist at the Institute for Fiscal Studies said: “Even if, as recent revisions to economic forecasts suggest, some of this improvement persists the coming Spending Review will still require some very difficult decisions and, most likely, more generous spending totals than currently pencilled in by the chancellor given the myriad pressures on public services and the benefit system following the pandemic.”

That is why the government sought to cut its overseas aid budget by £4bn – but that is a comparatively small sum in the context of overall government finances.

Elsewhere the government has committed to raise public spending by £55bn this year to help clear backlogs in the NHS and in the courts system.

Most economists believe the ultimate bill will be higher.

That is why the chancellor is dropping heavy hints that a rise in state pensions this year under the “triple lock” – whereby the benefit increases by the highest of 2.5%, inflation or average earnings – is not going to happen.

The government has committed to spending increases to clear NHS backlogs

Were the triple lock to apply, the state pension will have to match the rise in average earnings for May to July which, if as expected comes in at about 8% could cost the Treasury an extra £7bn a year.

Accordingly, Mr Sunak is arguing the lock should not apply.

He can reasonably point out that average earnings growth has been flattered by the fact that, a year ago, it was depressed by pay cuts, mass redundancies and the furlough scheme.

Yet the decision will be politically fraught.

The triple lock was a Conservative manifesto pledge and opinion polls suggest the public opposes scrapping it, even younger voters, despite the intergenerational unfairness implicit in the policy.

Mr Sunak is due already to announce the government’s three year Spending Review this autumn but there is also currently speculation in Westminster about the timing of the next budget.

Some Treasury officials would rather, it is said, have an early budget to nail down the government’s spending and taxation plans for the coming year in order to prevent the prime minister from making outlandish spending commitments ahead of the COP26 summit in November.

Others would prefer to postpone the budget until spring next year so the chancellor can better assess the strength of the recovery and the lasting damage done to the economy by the pandemic.

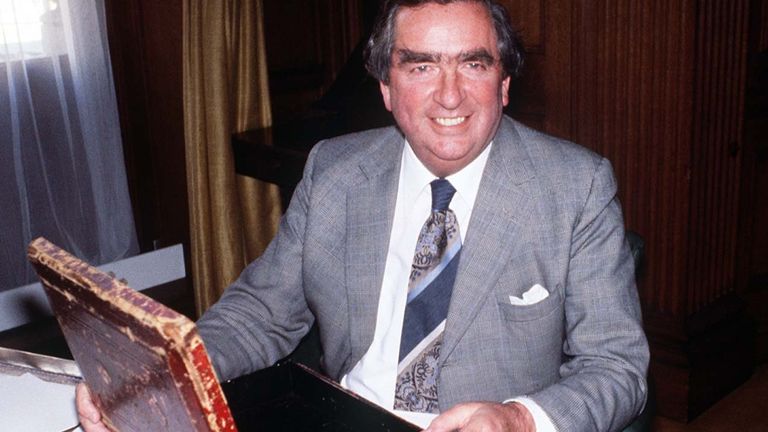

It is arguably the most challenging situation any chancellor has faced since, Labour’s Denis Healey in 1976

That happened last time when the budget was pushed back from autumn last year to March this year.

Making the chancellor’s job much harder would be an earlier than expected rise in interest rates.

This is due to the way the Bank of England’s asset purchase programme – quantitative easing in the jargon – works.

When the Bank buys a government bond, it credits the account of the seller, who effectively receives a deposit at the Bank.

These are known as “reserves” and the Bank pays interest on those reserves at Bank rate – currently 0.1%.

It means that the cost of QE rises if interest rates do.

All of this adds up to the most challenging situation any chancellor has faced since, arguably, Labour’s Denis Healey was forced in 1976 to seek a bail-out from the International Monetary Fund and possibly since the war.

Winter is closing in on the Bidston Rise housing estate in Birkenhead, but there’s one front garden that hasn’t given in yet.

A hydrangea is thriving in a shady spot and the borders are still in bloom. The man inside can give his neighbours advice on everything from ericaceous compost and fertiliser but he can’t earn a living from it.

Mick is a landscape gardener by trade but has been unemployed for almost a decade now because of his health, which deteriorated rapidly after a heart attack in his 30s.

Mick

A few years later, an operation to remove a clot in his right leg resulted in an amputation.

In 2016, he also lost his left leg to vascular disease. Now in his 60s, he still wants to work but the opportunities available to him are slim.

Bidston Rise, Birkenhead

Mick’s garden

Still, he counts himself lucky. “I know I’m getting on a bit now. I’ve lost my legs, but I can still do certain amounts of stuff.

“There are people out there who struggle to get out of bed in the morning, but they’re having their benefits cut because they’re saying they are fit for work. It’s ridiculous.”

Statistics met with ‘surprise and disbelief’

Mick is among the 10.4 million people of working age who report a disability in Britain today – that’s around a quarter of all 16-64 year olds.

It is a statistic that has been met with both surprise and disbelief as policymakers grapple for explanations behind the nation’s declining health, which is apparently so bad that 2.8 million people have dropped out of the labour market altogether, meaning they have stopped looking for work.

In Westminster, alarm has slowly crept in as the government struggles to digest the bill: Disabled people are entitled to benefits that support them with the costs of their disability.

They are also less likely to be in work than the rest of the population. The natural consequence is that Britain’s benefits bill has ballooned.

One-in-10 people now claim either incapacity or disability benefits. At £76.8bn, about 6% of everything the government spends now goes on these benefits and the costs are only forecast to rise.

Health-related benefits: What are they?

People with health conditions in this country can apply for two types of health benefits – incapacity and/or disability benefits.

They are very different.

Incapacity benefits are offered to people whose health limits their ability to work.

These are means-tested and only given to people in low-income families.

Applicants have to undergo a work assessment.

If they are judged to have “a limited capability for work-related activity”, they receive a top-up of £4,994 a year above their standard Universal Credit payment.

These people do not have to continue looking for work to receive the award.

Disability benefits help people cover the additional living costs of their disability.

The main one for working-age adults is the personal independence payment, also known as PIP.

PIP is not means-tested.

You can get it even if you have a job and about one-in-six people who claim it have jobs.

Applicants are tested on their ability to complete a range of tasks and, if they meet the criteria, receive between £1,500 and £9,610 a year.

About 45% of people claiming this benefit report mental or behavioural problems as their main condition.

Mental ill health

So what is actually going on?

There are no clear-cut answers but a few theories have been put forward: Some say the pandemic has had a clear long-term impact on our health, particularly our mental health.

The workforce is also getting older, so more of us are living with chronic conditions. Then there’s the cost of living crisis, which might have pushed more people to claim benefits when they may not have needed to in the past.

In the absence of any concrete explanations, however, the data has also fostered suspicions. Some people believe the system is too soft and that “everyday woes” are being medicalised.

Those “everyday woes” are mental health conditions, like depression and anxiety, which are driving the increase in reported disability.

The vast majority- 86% – of people on health-related benefits now have a mental health condition, even if it is not their primary condition.

After a failed attempt to reform disability benefits, the government has ordered a review into the diagnosis of mental health conditions, as well as autism and attention-deficit hyperactivity disorder (ADHD).

The health secretary has spoken about “overdiagnosis”.

Meanwhile, Conservative leader Kemi Badenoch has proposed a “crackdown on people exploiting the system”, including those with “mild” conditions like anxiety or depression.

But on the streets of Bidston, where NHS figures suggest 27.7% of people experience depression (more than double the national average), and where almost 40% of working-age people aren’t even looking for work, these debates seem to skip over the nuances and, in turn, miss the point.

Bidston Rise

A combination of ailments

For someone like Mick, who is so physically disabled that no one can accuse him of making it up, it isn’t his wheelchair that stops him from looking for work but his periodic bouts of depression. The mental anguish – when it hits – is far more disabling than his physical condition. He would know because he experiences both.

Mick and Gurpreet

“Oh, God. If it wasn’t for my dog, I’ll guarantee you, I probably wouldn’t be here now because I was in such a dark place,” he said.

“So many things were going on in my life at the time, and I was constantly in major pain, but I couldn’t get rid of it, no matter what medication I took or anything.

“I wasn’t coming out of my house, I didn’t open my blinds, I didn’t do hardly anything at all, and that’s not me.”

“Mental health problems have gone through the roof recently,” he said. “A lot of people are struggling mentally. I mean, I’ve gone through it myself.”

The trouble with trying to determine “how sick is too sick?” or “how disabled is too disabled?” is that most people report more than one condition, sometimes a mixture of mental and physical conditions.

Read more:

As GDP shrinks, it’s unclear where the economic jump-start will come from

Sickness bill costs £85bn a year, says report warning of ‘economic crisis’

For those on incapacity benefits, which are given to people deemed unfit to work, the average is about 2.7 conditions per person.

It could be a bad back that flares up with depression. Or, hearing loss that triggers anxiety.

Eventually, one might take over the other as the primary condition.

Then there are the agonies of life – perhaps a divorce during the cost-of-living crisis that caused emotional despair.

The medical perspective and the cost of living

Dr Mark Fraser, a local GP at the Fender Way Medical Centre, has seen it all.

“Demand has gone up considerably. An awful big driver of that probably is mental health, but we’re also seeing a general deterioration in people’s health and well-being,” he said.

“So, more chronic disease, certainly more cancers, more people are coming to us with lifestyle-related problems.”

Across the country, spending on health-related benefits accelerated significantly from 2022, when energy bills started to soar and inflation climbed above 11%.

Dr Mark Fraser

Dr Fraser is seeing more patients than he used to and almost all of them – from pensioners to young people – are in debt.

“It’s more expensive just to stay alive now. The cost of food, the cost of energy, the cost of housing, the cost of clothes, have gone up considerably in price over the last five or 10 years,” he said.

“And if you’re down at the lower end of income, the impact on that is massively disproportionate. Where the bread line used to be. We’re down to the breadcrumbs line.

“There’s no doubt that it’s very difficult for you to contemplate healthy living when you’re awake all night worrying about if you can afford the next bill or if you can afford the next shop.”

Increasingly anxious children

The degradation in young people’s mental health has been striking, with local GPs increasingly prescribing antidepressants to young people.

At the Fender Way Medical Centre, doctors are increasingly dealing with anxious children and young adults, some of whom are struggling to function and hold down jobs even when they get them.

Dr Mark Fraser and Sky’s Gurpreet Narwan

Dr Fraser said children might be growing up less resilient but they also appear to have been deeply affected by lockdowns, the loss of routine and the closure of local clubs and leisure centres.

“They don’t see a bright future for themselves. So they are a little bit resigned… there is despair later,” he said.

That despair is also finding its way into his surgery.

“There are more people in acute mental health crises, more often.

“I think that that used to be kind of unusual in general practice for you to be dealing with someone who you were worried wasn’t going to make it through the night if you let them go… a person at the point of ending their life… deciding that there is no point in carrying on, what’s the point?.. And it’s more frequent than it ever used to be.”

A nationwide issue

This is likely to ring true for GPs across the country.

Across the country, the number of people in contact with NHS mental health services has risen, as has antidepressant use.

Then there are deaths caused by alcohol, drugs or suicide, which have increased substantially among the working-age population since the pandemic.

They were up 24% – 3,700 deaths – in 2023 compared with pre-pandemic levels in England and Wales.

‘Deaths of despair’

It’s a phenomenon more closely associated with the US, where deaths linked to opioid use among middle-aged Americans – largely those without college degrees – led economists to first coin the phrase “deaths of despair” about a decade ago.

In Britain, we don’t have the same issues but among 45 to 54-year-olds, these deaths are now a bigger killer than heart disease.

So, while greater levels of reporting and diagnosis might be playing a part in the explosion of reported mental health conditions, there is clear evidence that our mental well-being has deteriorated over the past few years in very real ways.

The actual health conditions only tell one part of the story.

The austerity impact

Economic decline, wage stagnation and loss of community might tell another.

Changes to our benefit system, going back decades, could also be playing a part.

During the austerity years, the country’s safety net was pared back, with the government cutting housing benefits, raising the state pension age for women and lowering the benefit cap.

But they may have been a false economy. New research by the Institute of Fiscal Studies suggests that they nudged more people onto health-related benefits instead.

David Finch, assistant director at the Health Foundation, which funded the study, said: “Cuts to one part of the welfare system can push people to claim health-related benefits, potentially driven by the cuts worsening health.

“This creates a long-term risk that they spend longer out of the workforce and with lower incomes. Future welfare reform must learn the lessons of the past.”

Those lessons are not always immediately obvious but policymakers will have to reach into all corners of society to find them.

Resolving Britain’s problem with worklessness will take more than just a carrot or a stick.

A co-founder of Ben & Jerry’s has accused its owners of a fresh attempt to “silence” its social mission through the departures of three members of its independent board.

Ben Cohen spoke up after it emerged that its chair Anuradha Mittal, who had previously resisted parent company pressure to remove her, had left Ben & Jerry’s in the wake of new rules imposed by the US brand that included nine-year term limits for board members.

It is understood that two other long-standing directors, Daryn Dodson and Jennifer Henderson, will see their terms expire on 31 December.

Ben & Jerry’s has, since last week, been owned by The Magnum Ice Cream Company (TMICC) which was created by a spin-off from the UK-based consumer goods firm Unilever.

The demerger from Unilever created an ice cream firm with 20% of the global market. Pic:TMICC

Unilever bought Ben & Jerry’s in 2000 but the relationship has been sour since, despite the creation of the independent board at that time which was aimed at protecting the brand’s social mission.

The most high-profile spat came in 2021 when Ben & Jerry’s took the decision not to sell ice cream in Israeli-occupied Palestinian territories on the grounds that sales would be “inconsistent” with its values.

Unilever responded by selling the business to its licensee in Israel.

Sept: ‘Free Ben & Jerry’s’

A series of rows have followed akin to a tug of war, with Magnum refusing repeated demands by the co-founders of Ben & Jerry’s to sell the brand back.

Magnum and Unilever argue its mission has strayed beyond what was acceptable back in 2000, with the brand evolving into one-sided advocacy on polarising topics that risk reputational and business damage.

Co-founders Jerry Greenfield (right) with Ben Cohen in September 2024. Pic: AP

TMICC declared last month that Ms Mittal “no longer meets the criteria” to serve after internal investigations.

An audit of the separate Ben & Jerry’s Foundation, where she is also a trustee, found deficiencies in financial controls and governance. Magnum said the charitable arm risked having funding removed unless the alleged problems were addressed.

Ms Mittal had accused Magnum of attempts to “discredit” her and undermine the authority of the independent board.

Neither she, or the other two directors set to leave the board, were yet to comment.

Mr Cohen said the three directors had served the company with integrity and courage, calling their departure “another step in Magnum’s systematic effort to dismantle Ben & Jerry’s from the inside and silence the very social mission that gives the brand its value.”

Magnum said it fully supported the steps Ben & Jerry’s was taking to enhance board governance.

Acres of sweet, red strawberries are ripening in West Sussex this winter ready to be sold in UK supermarkets.

LED lighting in vast glasshouses is enabling berries to be grown all year on a commercial scale for the first time ever.

It means less reliance on fruit flown in from countries like Egypt.

Bartosz Pinkosz

“The LED lighting is the prime reason for successful growing,” said Bartosz Pinkosz, operations director of The Summer Berry.

“If it was not a sunny day, the LED lighting would create enough energy for leaves to absorb that energy, take it in and deliver the energy to the berries.

“We are able to have the right sweetness in the berries and the right shape, right size.”

There are 36,000 square metres of the greenhouses at the site in Chichester, partially powered by renewable energy and buzzing with bees as pollinators.

Acres of strawberries ripening in West Sussex

And the new strand to the business means year-round work for 50 people.

But while it might cut the food miles dramatically, there’s still an inevitable environmental impact when a colossal space is created warm enough for pickers to wear short sleeves in winter.

Dr Tara Garnett, director of food systems platform TABLE, said: “You’re going to need a lot of heat and you’re going to need a lot of light in order to reproduce those summer growing conditions so everything hinges on the energy source you’re going to be using.

“And when we look at the UK self sufficiency levels in fruit and vegetables they are appalling – 16% of the fruit we consume is UK-grown, so the vast majority is imported, and when it comes to vegetables we’re looking more at 50% or so, so there’s a lot more we can do to build up, and should be doing.”

Around 1.5 million punnets of strawberries are expected to be picked on the site over the full stretch of winter, allowing British strawberries to be eaten this Christmas.

But for some, it’s simple – strawberries should be saved for summer, even if it is a much shorter journey from plant to plate.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024