Borrowing is falling but Sunak faces the most challenging situation for a chancellor in decades

During the last 17 months we have become almost inured to the terrifying increases in government borrowing incurred in grappling with the pandemic.

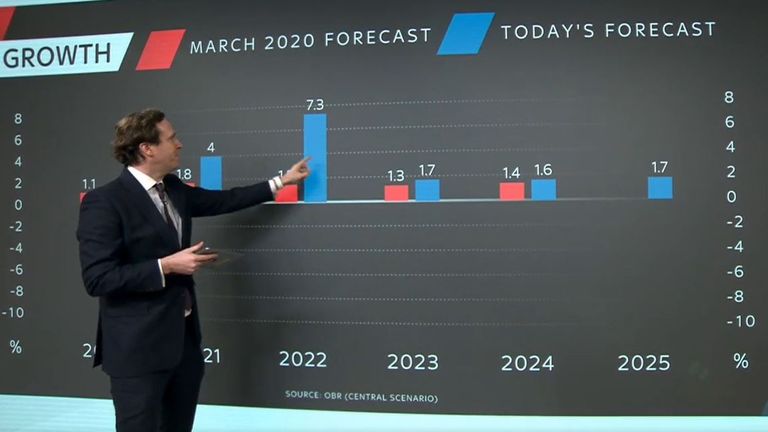

The government borrowed £303bn during the 2020-21 financial year, a peacetime record, equivalent to 14.5% of UK GDP.

Yet something interesting has been happening during the current financial year.

Tax burden to reach highest level since 1960s

In each of the first four months government borrowing, while still high, has come in significantly below the levels forecast by the independent Office for Budget Responsibility (OBR).

The latest figures for the public sector finances, published today, revealed that the government borrowed £10.4bn in July.

Make no mistake, this is still a terrifyingly high number, equivalent to borrowing of nearly £233,000 every minute.

It was, however, £10.1bn less than in July last year – and also significantly lower than the £11.8bn that City economists had been expecting.

The figure means that, during the first four months of the current financial year, the government borrowed £78bn – some £26bn less than the OBR had been forecasting at this stage.

There are a couple of key points to make about the numbers.

July’s figures are normally boosted by self-assessed tax returns

First of all, July is usually a strong month for tax receipts and therefore the public finances, because it is one of two months in the year – the other is January – in which the deadline falls due for payments by those completing self-assessed tax returns.

It was not unusual, pre-pandemic, for the government to record a surplus during July.

That appears to have been a key factor this month.

The government enjoyed tax receipts of £70bn during July – up £9.5bn on the same month last year.

Behind that was a £3.7bn improvement in self-assessed tax receipts on the same month last year, when HMRC allowed tax payments to be deferred, chiefly to support the self-employed.

But it probably also reflects that the economy is starting to recover.

VAT receipts were up by £1.2bn on July last year, fuel duty was up by £400m – partly reflecting higher petrol and diesel prices – and regular income tax payments were up by £800m.

There was also a big jump in stamp duty receipts, which at £1.4bn were double the level they were in July last year, reflecting a rush to beat the deadline for the end of the temporary £500,000 nil-rate band.

Fuel duty was up by £400m

Receipts from corporation tax, which is levied on company profits, also came in higher than the OBR had been expecting.

Secondly, government spending was lower, with the government shelling out £79.8bn during the month.

That was down £2.9bn on July last year and probably reflects that, not only did the government begin to taper away its furlough scheme, but also that there were fewer workers participating in the scheme.

Government spending on the furlough scheme during July was down £4.2bn on the same month last year while spending on the equivalent scheme for the self-employed was down £200m.

Worryingly, though, interest payments on the national debt came in at £3.4bn during the month – up £1.1bn on July last year.

As for the national debt, that stood at £2.216trn at the end of July, equivalent to 98.8% of GDP, which the Office for National Statistics (ONS) said was the highest it has been since March 1962.

The figures were welcomed by Rishi Sunak, the chancellor, who has been spelling out the need to restore order to the public finances.

He said: “Our recovery from the pandemic is well under way, boosted by the huge amount of support government has provided.

A rise in stamp duty receipts reflected a rush to complete deals before the winding down of a stamp duty holiday

“But the last 18 months have had a huge impact on our economy and public finances, and many risks remain.

“We’re committed to keeping the public finances on a sustainable footing, which is why at the budget in March I set out the steps we are taking to keep debt under control in the years to come.”

That is not to say the chancellor faces anything other than a major challenge on that front.

Isabel Stockton, research economist at the Institute for Fiscal Studies said: “Even if, as recent revisions to economic forecasts suggest, some of this improvement persists the coming Spending Review will still require some very difficult decisions and, most likely, more generous spending totals than currently pencilled in by the chancellor given the myriad pressures on public services and the benefit system following the pandemic.”

That is why the government sought to cut its overseas aid budget by £4bn – but that is a comparatively small sum in the context of overall government finances.

Elsewhere the government has committed to raise public spending by £55bn this year to help clear backlogs in the NHS and in the courts system.

Most economists believe the ultimate bill will be higher.

That is why the chancellor is dropping heavy hints that a rise in state pensions this year under the “triple lock” – whereby the benefit increases by the highest of 2.5%, inflation or average earnings – is not going to happen.

The government has committed to spending increases to clear NHS backlogs

Were the triple lock to apply, the state pension will have to match the rise in average earnings for May to July which, if as expected comes in at about 8% could cost the Treasury an extra £7bn a year.

Accordingly, Mr Sunak is arguing the lock should not apply.

He can reasonably point out that average earnings growth has been flattered by the fact that, a year ago, it was depressed by pay cuts, mass redundancies and the furlough scheme.

Yet the decision will be politically fraught.

The triple lock was a Conservative manifesto pledge and opinion polls suggest the public opposes scrapping it, even younger voters, despite the intergenerational unfairness implicit in the policy.

Mr Sunak is due already to announce the government’s three year Spending Review this autumn but there is also currently speculation in Westminster about the timing of the next budget.

Some Treasury officials would rather, it is said, have an early budget to nail down the government’s spending and taxation plans for the coming year in order to prevent the prime minister from making outlandish spending commitments ahead of the COP26 summit in November.

Others would prefer to postpone the budget until spring next year so the chancellor can better assess the strength of the recovery and the lasting damage done to the economy by the pandemic.

It is arguably the most challenging situation any chancellor has faced since, Labour’s Denis Healey in 1976

That happened last time when the budget was pushed back from autumn last year to March this year.

Making the chancellor’s job much harder would be an earlier than expected rise in interest rates.

This is due to the way the Bank of England’s asset purchase programme – quantitative easing in the jargon – works.

When the Bank buys a government bond, it credits the account of the seller, who effectively receives a deposit at the Bank.

These are known as “reserves” and the Bank pays interest on those reserves at Bank rate – currently 0.1%.

It means that the cost of QE rises if interest rates do.

All of this adds up to the most challenging situation any chancellor has faced since, arguably, Labour’s Denis Healey was forced in 1976 to seek a bail-out from the International Monetary Fund and possibly since the war.

Shares in UK banks have fallen sharply on the back of a report which urges the chancellor to place their profits in her sights at the coming budget.

As Rachel Reeves stares down a growing deficit – estimated at between £20bn-£40bn heading into the autumn – the Institute for Public Policy Research (IPPR) said there was an opportunity for a windfall by closing a loophole.

It recommended a new levy on the interest UK lenders receive from the Bank of England, amounting to £22bn a year, on reserves held as a result of the Bank’s historic quantitative easing, or bond-buying, programme.

Money latest: Ryanair changes cabin bag sizing

It was first introduced at the height of the financial crisis, in 2009.

The left-leaning think-tank said the money received by banks amounted to a subsidy and suggested £8bn could be taken from them annually to pay for public services.

It argued that the loss-making scheme – a consequence of rising interest rates since 2021 – had left taxpayers footing the bill unfairly as the Treasury has to cover any loss.

Why taxes might go up

The Bank recently estimated the total hit would amount to £115bn over the course of its lifetime.

The publication of the report coincided with a story in the Financial Times which spoke of growing fears within the banking sector that it was firmly in the chancellor’s sights.

Her first budget, in late October last year, put businesses on the hook for the bulk of its tax-raising measures.

Ms Reeves is under pressure to find more money from somewhere as she has ruled out breaking her own fiscal rules to help secure the cash she needs through heightened borrowing.

Is Labour plotting a ‘wealth tax’?

Other measures understood to be under consideration include a wealth tax, new property tax and a shake-up that could lead to a replacement for council tax.

Analysts at Exane told clients in a note: “In the last couple of years, the chancellor has been protective of the banks and has avoided raising taxes.

“However, public finances may require additional cash and pressures for a bank tax from within the Labour party seem to be rising,” it concluded.

The investor flight saw shares in Lloyds and NatWest plunge by more than 5%. Those for Barclays were more than 4% lower at one stage.

A spokesperson for the Treasury said the best way to strengthen public finances was to speed up economic growth.

“Changes to tax and spend policy are not the only ways of doing this, as seen with our planning reforms,” they added.

The man dubbed “Britain’s most hated boss” for his controversial policy of sacking hundreds of seafarers and replacing them with cheaper agency staff is to quit.

Sky News can exclusively reveal that Peter Hebblethwaite, the chief executive of P&O Ferries, is leaving the company.

Sources said he had decided to resign for personal reasons.

Money latest: The exact time to book train ticket at bargain price

Mr Hebblethwaite joined the ranks of Britain’s most notorious corporate figures in 2022 when P&O Ferries – a subsidiary of the giant Dubai-based ports operator DP World – said it was sacking 800 staff with immediate effect – some of whom learned their fate via a video message.

The policy, which Mr Hebblethwaite defended to MPs during subsequent select committee hearings, erupted into a national scandal, prompting changes in the law to give workers greater protection.

Under the new legislation, the government plans to tighten collective redundancy requirements for operators of foreign vessels.

In a statement issued in response to a request from Sky News, a P&O Ferries spokesperson said: “Peter Hebblethwaite has communicated his intention to resign from his position as chief executive officer to dedicate more time to family matters.

Peter Hebblethwaite gives evidence to a committee of MPs in 2022. Pic: PA

“P&O Ferries extends its gratitude to Peter Hebblethwaite for his contributions as CEO over the past four years.

“During his tenure the company navigated the challenges of the COVID-19 pandemic, initiated a path towards financial stability, and introduced the world’s first large double-ended hybrid ferries on the Dover-Calais route, thereby enhancing sustainability.

“We extend our best wishes to him for his future endeavours.”

A source close to the company said it anticipated making an announcement on Mr Hebblethwaite’s successor in the near term.

A former executive at J Sainsbury, Greene King and Alliance Unichem, Mr Hebblethwaite joined P&O Ferries in 2019, before taking over as chief executive in November 2021.

Insiders claimed on Friday that he had “transformed” the business following the bitter blows dealt to its finances by the COVID-19 pandemic and – to some degree – by the impact of Britain’s exit from the European Union.

A union protest is shown at the height of the mass sackings row in 2022

P&O Ferries carries 4.5 million passengers annually on routes between the UK and continental European ports including Calais and Rotterdam.

It also operates a route between Northern Ireland and Scotland, and is a major freight carrier.

The company’s losses soared during the pandemic, with DP World – its sole shareholder – supporting it through hundreds of millions of pounds in loans.

Its most recent accounts, which were significantly delayed, showed a significant reduction in losses in 2023 to just over £90m.

The reduction from the previous year’s figure of almost £250m was partly attributed to cost reduction exercises.

The accounts also showed that Mr Hebblethwaite received a pay package of £683,000, including a bonus of £183,000.

“I reflected on accepting that payment, but ultimately I did decide to accept it,” he told MPs.

“I do recognise it is not a decision that everybody would have made.”

The row over his pay was especially acute because of his admission that P&O Ferries’ lowest-paid seafarers received hourly pay of just £4.87.

Mr Hebblethwaite had argued since the mass sackings of 2022 that the company would have gone bust without the drastic cost-cutting that it entailed.

The company insisted at the time that those affected by the redundancies had been offered “enhanced” packages to leave.

Last October, the then transport secretary, Louise Haigh, said: “The mass sacking by P&O Ferries was a national scandal which can never be allowed to happen again,” adding that measures to protect seafarers from “rogue employers” would prevent a repetition.

“This issue has been ignored for over 2 years, but this new government is moving fast and bringing forward measures within 100 days,” Ms Haigh added.

“We are closing the legal loophole that P&O Ferries exploited when they sacked almost 800 dedicated seafarers and replaced them with low-paid agency workers and we are requiring operators to pay the equivalent of National Minimum Wage in UK waters.

“Make no mistake – this is good for workers and good for business.”

The minister’s description of P&O Ferries as “rogue”, and suggestion that consumers should boycott the company, sparked a row which threatened to overshadow the government’s International Investment Summit last October.

Sky News’s business and economics correspondent, Paul Kelso, revealed that DP World had withdrawn from participating in the event, and paused a £1bn investment announcement.

The company relented after Sir Keir Starmer publicly distanced the government from Ms Haigh’s characterisation of DP World.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment11 months ago

Environment11 months agoHere are the best electric bikes you can buy at every price level in October 2024