Two more household suppliers fail as wholesale energy prices hit new record levels

The energy watchdog has moved to reassure customers of two failed household suppliers as wholesale prices hit record levels, threatening a leap in bills in and after the winter months ahead.

Ofgem said the demise of Utility Point – first reported by Sky News – and People’s Energy meant their respective customer bases, totalling more than half a million, would fall under its ‘safety net’ protocol where a supplier is appointed to take them on.

It marked a further deterioration in the domestic supply market that has now seen four companies collapse this month alone amid a natural gas crunch.

Experts have pointed to difficulties restoring stocks following a cold end to last winter, exacerbated by low levels of wind over the summer forcing up demand for gas.

Gas-fired power accounts for almost half of the UK’s electricity generation.

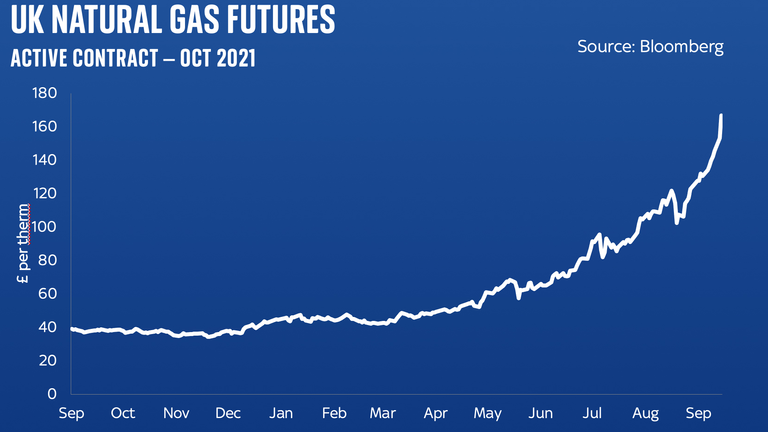

Reuters data seen by Sky News on Tuesday showed within-day wholesale gas prices had hit a record 167pence-per therm – a rise of 8% on the previous day while October contracts were at similar levels after crossing the 100p barrier in July.

Prices reached a previous peak of 60.7p-per therm during the winter of 2018/19.

Demands on the grid have forced coal-fired stations to be utilised at short notice to keep the lights on this month at a greater cost to the environment but also the system operator National Grid.

The gas shortfall, which has forced energy costs across Europe to balloon, is set to be reflected in household bills in future as consumers’ fixed price deals expire.

Homes are already grappling the effects of higher inflation – much of it a consequence of rising energy costs since economies got back in gear following COVID-19 disruption.

Families fear energy price hike

While the Bank of England expects this period of rising prices to be temporary, Ofgem confirmed last month that the energy price cap on so-called default tariffs would rise by at least £139 from October, affecting 15 million families.

That was to take account of wholesale costs rising by 50% over six months despite warnings it could push an additional half a million homes into fuel poverty at a time when the Universal Credit uplift of £20 a week will have ended.

The failure of challenger suppliers – seven this year – can be attributed to wafer thin profit margins being eroded by rising energy costs with smaller companies also not having the capital behind them to fully hedge their positions.

Britain’s climate reputation ‘on the line’

An Ofgem spokesman warned: “We do expect that gas prices will remain high for some time, unfortunately putting pressure on both customers and energy companies.”

Neil Lawrence, the regulator’s director of retail, added: “Although the news that a supplier going out of business can be unsettling, Utility Point and People’s Energy customers do not need to worry.

“Under our safety net we’ll make sure your energy supplies continue. If you are a domestic customer with credit on your Utility Point or People’s Energy account this is protected and you will not lose the money that is owed to you.

“Ofgem will choose a new supplier for you and while we are doing this our advice is to wait until we appoint a new supplier and do not switch in the meantime.

“You can rely on your energy supply as normal. We will update you when we have chosen a new supplier, who will then get in touch about your new tariff.”

Utility Point had accused Ofgem of playing a role in its collapse.

The boss of Utility Point told Sky News that suppliers were undercharging for energy because of Ofgem rules

Chief executive Ben Bolt told Sky News earlier on Thursday: “Recent international and national circumstances have created a perfect storm of events in the energy market which has meant that Utility Point has not been able to find a buyer for its business.

“Wholesale energy prices have soared to record levels and with the added price cap on default tariffs, the costs of supplying energy have increased dramatically.

“With every supplier undercharging for energy means that the fair cost that the regulator was trying to encourage has in fact had the opposite effect.

“This mix of unfortunate circumstances and lack of commercialism in the industry made it impossible to continue.

“With great sadness, Utility Point will cease trading.

“Our priority is with our 200 colleagues in Poole and Bournemouth, who have fought hard in the face of tough challenges and helping 225,000 customers transfer to another energy provider with minimal disruption.”

Business

Budget 2025: Hospitality pleads for ‘lifeline’ as Rachel Reeves accused of imposing ‘stealth tax’

Rachel Reeves has been accused of failing to “support the great British pub” as she promised in the budget, with owners facing skyrocketing business rates bills.

In her speech in the House of Commons on Wednesday, the chancellor said she was backing small businesses by introducing “permanently lower tax rates for over 750,000 retail, hospitality and leisure properties – the lowest tax rates since 1991”.

But while the government gave itself the powers to discount the business rates bills for high street businesses through legislation earlier this year, the chancellor only implemented a reduction of a quarter of what the government is able to, and she is being accused of imposing a “stealth tax”.

It has left small retail, hospitality, and leisure businesses questioning whether their businesses will be viable beyond April next year.

Sky’s Ed Conway looks at the aftermath of the budget and explains who the winners and losers are.

A Treasury spokesperson said: “We’re protecting pubs, restaurants and cafes with the budget’s £4.3bn support package – capping bill rises so a typical independent pub will pay around £4,800 less next year than they otherwise would have.

“This comes on top of cutting licensing costs to help more venues offer pavement drinks and al fresco dining, maintaining our cut to alcohol duty on draught pints, and capping corporation tax.”

Business rates, which are a tax on commercial properties in England and Wales, are calculated through a complex formula of the value of the property, assessed by a government agency every three years, combined with a national “multiplier” set by the Treasury, giving a final cash amount.

Chancellor Rachel Reeves has been accused of imposing a “stealth tax” on hospitality businesses. Pic: PA

Over the last few years, small businesses were given business rates relief of 75% to support them over the COVID pandemic, and Ms Reeves reduced that to 40% at last year’s budget.

The idea was that at the budget this year, the chancellor would remove that remaining relief in favour of reforming the business rates system to compensate for that drop, while shifting the tax burden on to much bigger businesses and companies like Amazon with lots of warehouse space.

However, the chancellor only announced a 5p in the pound discount for small retail, hospitality, and leisure businesses, rather than the assumed 20p drop which the government gave itself the powers to implement, and which trade bodies had been lobbying for.

How will your personal finances change following the budget announced by the chancellor?

On top of that, small businesses have seen the government-assessed value of their property increase dramatically, which wipes out the discount, and sees their business rates bill shoot far above what they had previously been paying.

One pub owner near Hull, Sam Caroll, has seen the assessed value of one of his two properties increase from £67,000 to £110,000 in just three years – a 64% increase.

He told Sky News that there is a “continual question” of business viability, and while he thinks they can “adapt” in the short term, “there will be a tipping point at some point”. Even at the moment, packing out their pubs seven nights a week, “it’s difficult for us to break even”, he said.

There will be a discount for small businesses to transition to the higher business rates level, but by year three, almost the full amount is expected to be payable, and Mr Carroll described it as “getting f***** slowly, instead of getting f***** overnight”.

👉 Listen to Sky News Daily on your podcast app 👈

Sean Hughes, who owns multiple hospitality venues in St Albans, has also seen vast increases in the assessed value of his properties, and was sharply critical of the transitional arrangements the government is implementing.

He told Sky News: “Fundamental business rate reform was promised and we have total chaos. If [the system] was fair, why would they need transitional relief periods?”

A spokesperson of the Valuation Office Agency (VOA), which assesses the value of commercial properties for business rates purposes, told Sky News: “At the last revaluation, some sectors including hospitality were significantly affected by the pandemic, which resulted in much lower rateable values than they would have seen otherwise. Businesses that have now seen a recovery in trade are also likely to see an increase in their rateable value.”

Read more:

Reeves accused of deliberately making UK finances look worse

Budget is a big risk for Labour’s election plans

However, Sky News has seen evidence of businesses whose assessed value did not decrease when assessed during the pandemic, but actually rose, and has risen dramatically this year.

Data compiled by the Pubs Advisory Service, shows that the number of pubs in the UK has decreased by nearly 5% in three years, but the average value of the properties has risen by an average of 36.82% per pub.

And analysis by UK Hospitality, the trade body that represents hospitality businesses, has found that over the next three years, the average pub will pay an extra £12,900 in business rates, even with the transitional arrangements, while an average hotel will see its bill soar by £205,200.

The prime minister has defended the budget after he and the chancellor were accused of breaking their promise to voters.

The body adds that by 2028/29, an average pub’s business rates will have increased by 76% and an average hotel’s by 115%, compared to 16% for a distribution warehouse like the ones the web giants use.

It’s not just the business rates rise that is worrying owners – it is the increase in employers’ national insurance implemented at the last budget, the increase in energy bills over the last few years, and the rise in the minimum wage, particularly for young people.

With the budget set to squeeze disposal income, there is little room for price increases to make up the shortfall either.

In a letter to the chancellor on Friday, Liberal Democrat deputy leader Daisy Cooper said small business owners “have been pushed to tears as they’re hit with the bombshell of higher business rates bills”, noting that “the government has chosen not to use the full powers it gave itself to throw high streets a lifeline”.

She added that businesses had been promised “permanently lower business rates”, but it appears the government has “broken yet another promise, by imposing a stealth tax not just on people, but on treasured high street businesses too”, and called on ministers to “throw our high streets and Britain’s hospitality sector a lifeline”.

Conservative shadow business secretary Andrew Griffith published his own analysis of the government’s budget measures on Friday morning, that found they will “hammer British pubs”.

Of the chancellor, he said: “She pretended in her budget speech to be supportive, whilst the true detail is that a combination of rate revaluations and scrapping reliefs will leave most pubs paying thousands of pounds more than they cannot afford.”

Kate Nicholls, Chair of UKHospitality, said in a statement: “The government promised in its manifesto that it would level the playing field between the high street and online giants. The plan in the budget to achieve this is quickly unravelling, and will deliver the exact opposite.”

She said they “repeatedly warned the Treasury” of the impending impacted of the value reassessment, but nonetheless, hospitality businesses are now facing “eye-watering increases”.

She added: “We agree with its reforms to deliver permanently lower business rates for hospitality and we appreciate the package of transitional relief, but its current proposal is not delivering lower bills. A 20p discount for hospitality would. We urge the chancellor to revisit.”

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024