Two more household suppliers fail as wholesale energy prices hit new record levels

The energy watchdog has moved to reassure customers of two failed household suppliers as wholesale prices hit record levels, threatening a leap in bills in and after the winter months ahead.

Ofgem said the demise of Utility Point – first reported by Sky News – and People’s Energy meant their respective customer bases, totalling more than half a million, would fall under its ‘safety net’ protocol where a supplier is appointed to take them on.

It marked a further deterioration in the domestic supply market that has now seen four companies collapse this month alone amid a natural gas crunch.

Experts have pointed to difficulties restoring stocks following a cold end to last winter, exacerbated by low levels of wind over the summer forcing up demand for gas.

Gas-fired power accounts for almost half of the UK’s electricity generation.

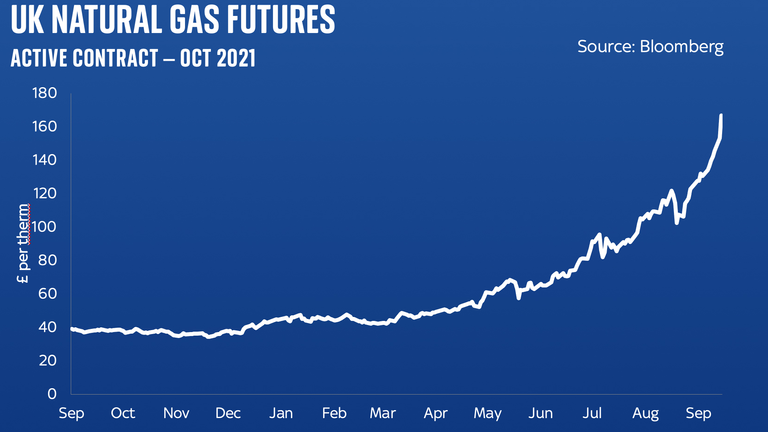

Reuters data seen by Sky News on Tuesday showed within-day wholesale gas prices had hit a record 167pence-per therm – a rise of 8% on the previous day while October contracts were at similar levels after crossing the 100p barrier in July.

Prices reached a previous peak of 60.7p-per therm during the winter of 2018/19.

Demands on the grid have forced coal-fired stations to be utilised at short notice to keep the lights on this month at a greater cost to the environment but also the system operator National Grid.

The gas shortfall, which has forced energy costs across Europe to balloon, is set to be reflected in household bills in future as consumers’ fixed price deals expire.

Homes are already grappling the effects of higher inflation – much of it a consequence of rising energy costs since economies got back in gear following COVID-19 disruption.

Families fear energy price hike

While the Bank of England expects this period of rising prices to be temporary, Ofgem confirmed last month that the energy price cap on so-called default tariffs would rise by at least £139 from October, affecting 15 million families.

That was to take account of wholesale costs rising by 50% over six months despite warnings it could push an additional half a million homes into fuel poverty at a time when the Universal Credit uplift of £20 a week will have ended.

The failure of challenger suppliers – seven this year – can be attributed to wafer thin profit margins being eroded by rising energy costs with smaller companies also not having the capital behind them to fully hedge their positions.

Britain’s climate reputation ‘on the line’

An Ofgem spokesman warned: “We do expect that gas prices will remain high for some time, unfortunately putting pressure on both customers and energy companies.”

Neil Lawrence, the regulator’s director of retail, added: “Although the news that a supplier going out of business can be unsettling, Utility Point and People’s Energy customers do not need to worry.

“Under our safety net we’ll make sure your energy supplies continue. If you are a domestic customer with credit on your Utility Point or People’s Energy account this is protected and you will not lose the money that is owed to you.

“Ofgem will choose a new supplier for you and while we are doing this our advice is to wait until we appoint a new supplier and do not switch in the meantime.

“You can rely on your energy supply as normal. We will update you when we have chosen a new supplier, who will then get in touch about your new tariff.”

Utility Point had accused Ofgem of playing a role in its collapse.

The boss of Utility Point told Sky News that suppliers were undercharging for energy because of Ofgem rules

Chief executive Ben Bolt told Sky News earlier on Thursday: “Recent international and national circumstances have created a perfect storm of events in the energy market which has meant that Utility Point has not been able to find a buyer for its business.

“Wholesale energy prices have soared to record levels and with the added price cap on default tariffs, the costs of supplying energy have increased dramatically.

“With every supplier undercharging for energy means that the fair cost that the regulator was trying to encourage has in fact had the opposite effect.

“This mix of unfortunate circumstances and lack of commercialism in the industry made it impossible to continue.

“With great sadness, Utility Point will cease trading.

“Our priority is with our 200 colleagues in Poole and Bournemouth, who have fought hard in the face of tough challenges and helping 225,000 customers transfer to another energy provider with minimal disruption.”

The UK will miss the White House-imposed deadline to agree a trade deal on steel and aluminium this week, according to insiders from government and industry.

Donald Trump had insisted that unless Britain could finalise the details of its metals trade deal with the US by 9 July, he would raise the tariffs faced by steel and aluminium imports from the 25% the UK currently pays to the 50% paid by other countries. If it could seal the deal, those tariffs could drop to zero.

Money blog: 10 happiest and unhappiest professions for shift workers

However, despite weeks of negotiations and promises that the deal would be completed by the end of June, talks have foundered on two key issues. First, the US is insisting that only steel “melted and poured” in the UK (in other words, forged in blast furnaces or electric arc furnaces) can be included in the deal. However, one of Britain’s biggest steel exporters to the US, Tata Steel, is not melting and pouring its UK steel because of the closure of its blast furnaces.

Second, the US is wary of the fact that while the government has taken control of British Steel, which operates Britain’s last remaining blast furnaces in Scunthorpe, the company itself still legally has Chinese owners.

Government insiders have told businesses they still expect to have a deal done by the end of this month, and that they are confident the White House will not impose the 50% tariffs for the time being. They say one of the chief challenges they face is that the administration is so overwhelmed by attempts to negotiate with other countries that they lack the bandwidth to deal with the small print on Britain’s deal.

Inside the UK’s last blast furnaces

“As far as the Americans are concerned, the UK is already a done deal,” said one person close to the negotiations. The problem is that while a deal has been done on car and aerospace exports to the US, the metals element of the trade agreement is still some way from being signed. In the meantime, steel exports continue to incur tariffs – albeit lower than those imposed on other countries around the world.

Business

At least 13 postmasters may have taken their own lives, public inquiry into Post Office scandal finds

At least 13 postmasters may have taken their own lives after being accused of wrongdoing based on evidence from the Horizon IT system that the Post Office and developers Fujitsu knew could be false, the public inquiry has found.

A further 59 people told the inquiry they considered ending their lives, 10 of whom tried on at least one occasion, while other postmasters and family members recount suffering from alcoholism and mental health disorders including anorexia and depression, family breakup, divorce, bankruptcy and personal abuse.

Follow latest on public inquiry into Post Office scandal

Writing in the first volume of the Post Office Horizon IT Inquiry report, chairman Sir Wyn Williams concludes that this enormous personal toll came despite senior employees at the Post Office knowing the Horizon IT system could produce accounts “which were illusory rather than real” even before it was rolled out to branches.

Sir Wyn said: “I am satisfied from the evidence that I have heard that a number of senior, and not so senior, employees of the Post Office knew or, at the very least, should have known that Legacy Horizon was capable of error… Yet, for all practical purposes, throughout the lifetime of Legacy Horizon, the Post Office maintained the fiction that its data was always accurate.”

Referring to the updated version of Horizon, known as Horizon Online, which also had “bugs errors and defects” that could create illusory accounts, he said: “I am satisfied that a number of employees of Fujitsu and the Post Office knew that this was so.”

The first volume of the report focuses on what Sir Wyn calls the “disastrous” impact of false accusations made against at least 1,000 postmasters, and the various redress schemes the Post Office and government has established since miscarriages of justice were identified and proven.

‘It stole a lot from me’

Recommendations regarding the conduct of senior management of the Post Office, Fujitsu and ministers will come in a subsequent report, but Sir Wyn is clear that unjust and flawed prosecutions were knowingly pursued.

“All of these people are properly to be regarded as victims of wholly unacceptable behaviour perpetrated by a number of individuals employed by and/or associated with the Post Office and Fujitsu from time to time and by the Post Office and Fujitsu as institutions,” he says.

What are the inquiry’s recommendations?

Calling for urgent action from government and the Post Office to ensure “full and fair compensation”, he makes 19 recommendations including:

• Government and the Post Office to agree a definition of “full and fair” compensation to be used when agreeing payouts

• Ending “unnecessarily adversarial attitude” to initial offers that have depressed the value of payouts, and ensuring consistency across all four compensation schemes

• The creation of a standing body to administer financial redress to people wronged by public bodies

• Compensation to be extended to close family members of those affected who have suffered “serious negative consequences”

• The Post Office, Fujitsu and government agreeing a programme for “restorative justice”, a process that brings together those that have suffered harm with those that have caused it

Regarding the human impact of the Post Office’s pursuit of postmasters, including its use of unique powers of prosecution, Sir Wyn writes: “I do not think it is easy to exaggerate the trauma which persons are likely to suffer when they are the subject of criminal investigation, prosecution, conviction and sentence.”

He says that even the process of being interviewed under caution by Post Office investigators “will have been troubling at best and harrowing at worst”.

Read more:

Post Office inquiry lays bare heart-breaking legacy – analysis

‘Hostile and abusive behaviour’

The report finds that those wrongfully convicted were “subject to hostile and abusive behaviour” in their local communities, felt shame and embarrassment, with some feeling forced to move.

Detailing the impact on close family members of those prosecuted, Sir Wyn writes: “Wives, husbands, children and parents endured very significant suffering in the form of distress, worry and disruption to home life, in employment and education.

“In a number of cases, relationships with spouses broke down and ended in divorce or separation.

“In the most egregious cases, family members themselves suffered psychiatric illnesses or psychological problems and very significant financial losses… their suffering has been acute.”

The report includes 17 case studies of those affected by the scandal including some who have never spoken publicly before. They include Millie Castleton, daughter of Lee Castleton, one of the first postmasters prosecuted.

Three things you need to know about Post Office report

She told the inquiry how her family being “branded thieves and liars” affected her mental health, and contributed to a diagnosis of anorexia that forced her to drop out of university.

Her account concludes: “Even now as I go into my career, I still find it so incredibly hard to trust anyone, even subconsciously. I sabotage myself by not asking for help with anything.

“I’m trying hard to break this cycle but I’m 26 and am very conscious that I may never be able to fully commit to natural trust. But my family is still fighting. I’m still fighting, as are many hundreds involved in the Post Office trial.”

Business Secretary Jonathan Reynolds said the inquiry’s report “marks an important milestone for sub-postmasters and their families”.

He added that he was “committed to ensuring wronged sub-postmasters are given full, fair, and prompt redress”.

“The recommendations contained in Sir Wyn’s report require careful reflection, including on further action to complete the redress schemes,” Mr Reynolds said.

“Government will promptly respond to the recommendations in full in parliament.”

Post Office minister Gareth Thomas said, “Sir Wyn’s report highlights a series of failings by the Post Office and various governments. His recommendations are immensely helpful as a guide for what is needed to finish the job”.

The chairman of Marks & Spencer has told MPs the company is “still in the rebuild mode” and will be for “some time to come” following a cyber attack which led to empty shelves and limited online operations for months.

Speaking publicly for the first time since the attack, Archie Norman declined to answer whether the business had paid a ransom.

“It’s a business decision, it’s a principal decision,” he told members of the Business and Trade Committee (BTC).

“The question you have to ask is – and I think all businesses should ask – is, when they look at the demand, what are they getting for it?

“Because once your systems are compromised and you’re going to have to rebuild anyway, maybe they’ve got exfiltrated data that you don’t want to publish. Maybe there’s something there, but in our case, substantially the damage had been done.”

Money blog: 10 happiest and unhappiest professions for shift workers

When asked again later in the BTC evidence session, Mr Norman said, “We’re not discussing any of the details of our interaction with the threat actor, including this subject, but that subject is fully shared with the NCA [National Crime Agency].”

“We don’t think it’s in the public interest to go into that subject on it, because it is a matter of law enforcement”, he added.

What happened?

The initial entry into M&S’s systems took place on 17 April through “sophisticated impersonation” that involved a third party, Mr Norman said.

It was two days later, on Easter Saturday, before the company became aware of the attack, and approximately a week after the intrusion, before the retailer heard directly from the attacker.

Who is behind M&S cyberattack?

A day later, after learning of the attack, the authorities were notified, while customers were told on Tuesday, MPs heard.

As well as British authorities, the US FBI was contacted, who are “more muscled up in this zone” and were “very supportive”, Mr Norman said.

By the time the breach is clear, systems have already been compromised, the chairman said.

The group behind the attack may have been Scattered Spider, some of whom are believed to be English-speaking teenagers, but Mr Norman said M&S made an early decision that no one from the company would deal directly with the so-called “threat actor”.

“Anybody who’s suffered an event like ours, it would be foolish to say there’s not a thousand things you’d like to have done differently,” he added.

Advice for businesses

In a warning to other businesses, M&S’s general counsel and company secretary Nick Folland said firms should be prepared to operate without IT systems.

“One of the things that we would say to others is make sure you can run your business on pen and paper,” he said.

Awareness and planning for the threats of cybersecurity meant M&S had trebled the number of people working on cybersecurity to 80and doubled its expenditure.

“We curiously doubled our insurance cover last year”, Mr Norman added.

In a good position

The business was better positioned to deal with the strike than at the start of Mr Norman’s tenure, he said.

“The context of M&S is when I joined the business, it was a very broken business… our systems were in a pretty decrepit state.”

“So I have to say if this has happened then I think we would have been kippered.”

Read more:

UK to miss deadline to agree steel and aluminium tariffs

Flavour of what’s to come as first Post Office inquiry lays bare heart-breaking legacy

Recent profits meant the company was “muscled up”.

“Extensive” insurance cover means M&S expects to make an “unsurprisingly significant claim” and receive “substantial recovery”, though the process of finding out how much will take about 18 months.

The £300m sum M&S said it expected to lose as a result of the cyber attack does not include money it expects to claim via insurance. The financial hit was calculated at £300m as the chain department store was losing £10m a week by not operating online.

The incident has “not really” affected its future, Mr Norman said.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike