Army tankers to deliver fuel to petrol stations from Monday

Army tanker drivers are to start delivering fuel to petrol stations from Monday in an emergency government move prompted by the continuing crisis at the pumps.

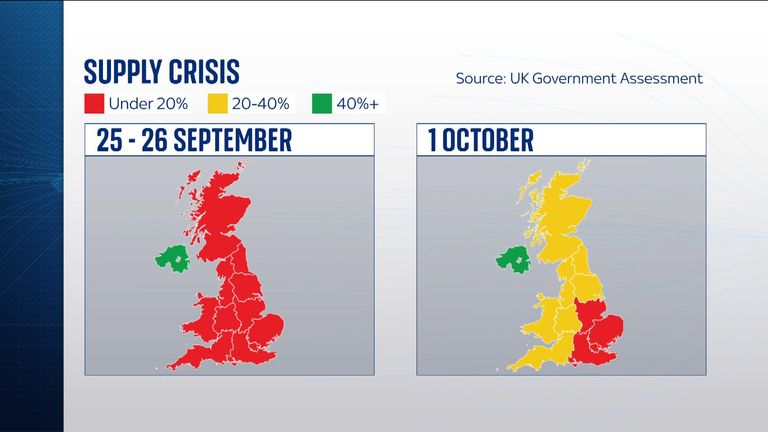

Senior ministers have been alarmed at how slowly the fuel supply disruption is improving, with motorists still forced to queue for hours for fuel after more than a week of forecourt chaos.

Almost 200 soldiers – including 100 drivers – have been training with haulage firms this week, learning how to fill up tankers and petrol pumps, and the first army deliveries will be made early on Monday morning.

Fuel shortages have improved for most areas but are still not back to normal

Announcing the move, Defence Secretary Ben Wallace said: “Across the weekend over 200 military personnel will have been mobilised as part of Operation Escalin.

“While the situation is stabilising, our Armed Forces are there to fill in any critical vacancies and help keep the country on the move by supporting the industry to deliver fuel to forecourts.”

At the same time, Cabinet Office minister Steve Barclay, who is in charge of the government’s response to the fuel crisis, appealed to motorists to stop panic buying at the pumps

“The government has taken decisive action to tackle the short-term disruption to our supply chains, and in particular the flow of fuel to forecourts,” he said.

“We are now seeing the impact of these interventions with more fuel being delivered to forecourts than sold and, if people continue to revert to their normal buying patterns, we will see smaller queues and prevent petrol stations closing.”

And despite no end to the long queues at garages in some parts of the UK, particularly southeast England and London, senior ministers still insist the demand for fuel has stabilised.

Gridlock in northwest London due to petrol queues

“Thanks to the immense efforts of industry over the past week, we are seeing continued signs that the situation at the pumps is slowly improving,” Business Secretary Kwasi Kwarteng claimed.

“UK forecourt stock levels are trending up, deliveries of fuel to forecourts are above normal levels, and fuel demand is stabilising.

“It’s important to stress there is no national shortage of fuel in the UK, and people should continue to buy fuel as normal. The sooner we return to our normal buying habits, the sooner we can return to normal.”

But the decision to send in the army came as Rishi Sunak, the chancellor, issued a gloomy warning that shortages of goods could last until Christmas.

“These shortages are very real,” Mr Sunak said in a Daily Mail interview. “We’re seeing real disruption in supply chains in different sectors, not just here but around the world.”

And admitting that families face a “challenging” winter, the chancellor added: “We’re determined to do what we can to try to mitigate as much of this as we can.”

The government’s announcement on sending in the army to tackle the fuel crisis came just hours after it was demanded by Labour leader Sir Keir Starmer.

There continues to be long queues at petrol stations in some parts of the country

It also followed a warning by the Petrol Retailers Association, which represents independent garages, that more than a quarter of its filling stations have no fuel.

Calling on Boris Johnson to “take emergency action to get a grip”, Sir Keir also called for extended opening hours for petrol stations to help NHS shift workers and other key workers.

And he urged the prime minister to recall parliament and hold an emergency summit of the road haulage industry, training providers, business groups, government ministers and transport unions to focus on the immediate crisis.

The government says it is already taking a range of measures to ease temporary supply chain pressures in food haulage industries, brought on by the pandemic and the global economy rebounding around the world.

In a further step to manage these pressures in the short term, the government is introducing a scheme allowing fuel tanker drivers and food haulage truckers to work in the UK immediately on a temporary basis.

Under these plans:

• 300 fuel drivers will be able to arrive immediately, subject to immigration checks, and stay to work until the end of March 2022

• 4,700 food haulage drivers who will arrive from late October and leave by 28 February 2022

• 5,500 poultry workers who will arrive from late October and be able stay up to 31 December 2021

The government says these temporary, time-limited visa measures, do not detract from a commitment to upskill and increase the wages of domestic labour, but are in recognition of the extraordinary set of circumstances affecting the stability of the UK supply chain.

Motorists are still forced to queue for hours for fuel after more than a week of forecourt chaos

Ministers say they want to see employers make long-term investments in the UK domestic workforce instead of relying on overseas labour to build a high-wage, high-skill economy.

In addition to short-term fixes, the government says it is also working with industry to find long-term solutions to the shortage of HGV drivers through improved testing and hiring, with better pay, working conditions and diversity.

To help with recruitment, the government also says it is collaborating with freight associations to drive up standards of lorry parking facilities, helping to make the HGV industry more attractive for prospective drivers and supporting the wellbeing of those currently working as lorry drivers.

Other moves include an immediate increase in HGV testing and new skills boot camps to train up to 4,000 more people to become HGV drivers.

A Chinese blockchain event was reportedly cut short on Tuesday due to overcrowding, but some attendees expressed concerns over the country’s recent crackdowns.

Rachel Reeves has said she is determined to “defy” forecasts that suggest she will face a multibillion-pound black hole in next month’s budget, but has indicated there are some tough choices on the way.

Writing in The Guardian, the chancellor argued the “foundations of Britain’s economy remain strong” – and rejected claims the country is in a permanent state of decline.

Reports have suggested the Office for Budget Responsibility is expected to downgrade its productivity growth forecast by about 0.3 percentage points.

Rachel Reeves. PA file pic

That means the Treasury will take in less tax than expected over the coming years – and this could leave a gap of up to £40bn in the country’s finances.

Ms Reeves wrote she would not “pre-empt” these forecasts, and her job “is not to relitigate the past or let past mistakes determine our future”.

“I am determined that we don’t simply accept the forecasts, but we defy them, as we already have this year. To do so means taking necessary choices today, including at the budget next month,” the chancellor added.

She also pointed to five interest rate cuts, three trade deals with major economies and wages outpacing inflation as evidence Labour has made progress since the election.

Speculation is growing that Ms Reeves may break a key manifesto pledge by raising income tax or national insurance during the budget on 26 November.

Read more from Sky News:

What tax rises could Reeves announce?

Start-ups warn chancellor over budget bombshell

Chancellor faces tough budget choices

Budget decisions ‘don’t come for free’

Although her article didn’t address this, she admitted “our country and our economy continue to face challenges”.

Her opinion piece said: “The decisions I will take at the budget don’t come for free, and they are not easy – but they are the right, fair and necessary choices.”

Yesterday, Sky’s deputy political editor Sam Coates reported that Ms Reeves is unlikely to raise the basic rates of income tax or national insurance, to avoid breaking a promise to protect “working people” in the budget.

Tax hikes possible, Reeves tells Sky News

Sky News has also obtained an internal definition of “working people” used by the Treasury, which relates to Britons who earn less than £45,000 a year.

This, in theory, means those on higher salaries could be the ones to face a squeeze in the budget – with the Treasury stating that it does not comment on tax measures.

In other developments, some top economists have warned Ms Reeves that increasing income tax or reducing public spending is her only option for balancing the books.

Experts from the Institute for Fiscal Studies have cautioned the chancellor against opting to hike alternative taxes instead, telling The Independent this would “cause unnecessary amounts of economic damage”.

Although such an approach would help the chancellor avoid breaking Labour’s manifesto pledge, it is feared a series of smaller changes would make the tax system “ever more complicated and less efficient”.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024