Petrol retailers warn of record prices at the pumps within days

Petrol retailers have been accused of “taking a bigger cut” by a motoring group after warning that record pump prices are expected within days.

The Petrol Retailers Association (PRA) – which shot to public prominence last month as the industry grappled delivery problems that sparked weeks of panic-buying in areas of England – blamed rising wholesale costs for the situation.

The body, which represents about two-thirds of forecourts across the UK, said pump prices of 142 pence per litre (ppl) for petrol and 148p for diesel set in April 2012 were “almost certain to be eclipsed before the end of October”.

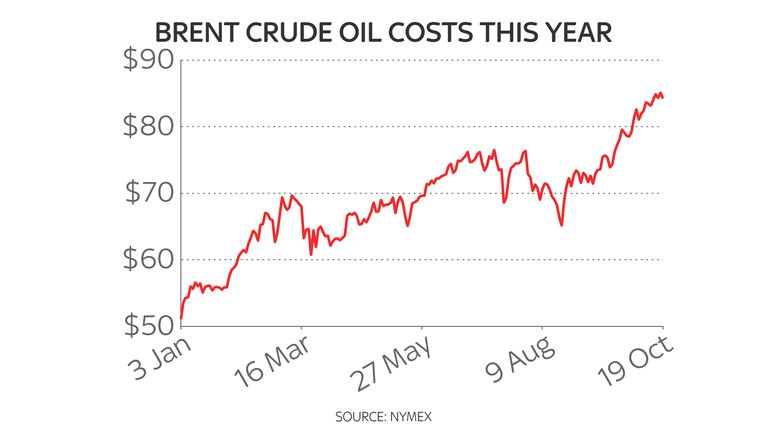

Its outgoing chairman, Brian Madderson, said: “The primary reason is the rise and rise of crude oil costs which recently hit $85/barrel for Brent crude.

“This involves more than a 50% increase since January 2021 and has been caused by a cutback in production from OPEC countries and Russia at the same time as the global economies are staging a rapid economic turnaround from the global pandemic.”

He pointed to the latest Experian Catalist data which showed average petrol costs of 141.35ppl and 144.84ppl on Tuesday and warned there was no end in sight to the pressure on pump costs amid market talk that Brent could hit $100/barrel by Christmas.

Mr Madderson, whose organisation represents independent fuel operators, added: “Current average pump prices across the UK are being softened by some of the largest retailers who typically benefit from a 3 or even 4-week lag to their delivered fuel prices.

“Only last week, two major grocery retailers in Belfast were vying for business by offering fuel at below standard wholesale cost with pump prices as low as 125.9ppl for petrol and 130.9ppl for diesel.”

HGV delivering fuel is driven by military

Motoring groups had, in recent weeks, suggested that rising prices were not only down to market forces but profiteering among retailers.

RAC fuel spokesman Simon Williams said of the PRA’s warning: “The bioethanol component of unleaded has increased from 5% to 10% with the introduction of E10 in September and unfortunately that costs even more than petrol on the wholesale market.

“Retailers are also taking a bigger cut on petrol than they normally do at around 8p a litre which is a further blow to drivers, particularly as VAT is charged at 20% on top of this and the other increases.”

He added: “We strongly urge retailers not to contribute further to the pump price rise”.

The price prediction adds to an already gloomy picture for household bills over the winter months – a consequence of global supply disruption as economies get back in gear including a shortage of workers as supply fails to meet demand.

The Office for National Statistics reported earlier in the day that fuel prices had provided the largest upwards pressure on inflation during September without the impact of the delivery problems even being included.

Economists say wider energy costs – particularly for home gas and electricity – will provide the largest squeeze on family finances in the months ahead.

Business

Farage and Tice right to scrutinise one of Bank of England’s most radical monetary experiments in history

There was some speculation, when it emerged that Nigel Farage was heading to Threadneedle Street to see the Bank of England governor, that he was about to “do a Trump”.

You might recall, if you follow American politics, how the US president has been, for want of a better word, trolling the chairman of the Federal Reserve, Jerome Powell, threatening to fire him if he didn’t cut interest rates. Might Mr Farage and Reform be about to do the same thing in the UK, raising deep (and, for economists, scary) questions about the independence of the central bank?

The short answer, as far as anyone can tell following today’s meeting, is: no. Instead, Mr Farage and his fellow Reform MP Richard Tice enjoyed a relatively cordial meeting with the governor, where they discussed the intricacies of quantitative easing, the Bank’s reserves policies and even cryptocurrency – a slightly unexpected addition to the agenda which might reflect the fact that Reform is hoping to raise lots of campaign funds from crypto dudes.

Money latest: HMRC can now take money direct from your account if you don’t pay

The main Bank-related issue Reform has been campaigning on – Mr Tice in particular – comes back to something seemingly arcane but certainly important. As you may be aware, in recent years, the Bank of England has, alongside its interest rate policy, been engaged in something called quantitative easing (QE). QE is complex, but it boils down to this: in an effort to boost the economy, the Bank bought up a lot of government bonds and they now sit awkwardly in its balance sheet. In recent months, the Bank has begun to reverse QE (quantitative tightening) – selling off billions of pounds of bonds.

Bank of England’s £134bn gamble

Anyway, reach deeper into the arcane mechanism of how QE works and something interesting leaps out. Two things, actually. First, as part of QE, in order to get hold of those government bonds, the Bank created “reserves” – sort of bank-account-at-the-Bank-of-England – for the high street banks from whom it bought them.

Tens of billions to high street banks

Those reserves earn interest at the Bank’s official interest rate. At the time of QE, the rate was near zero, so no one spent much time thinking about reserves. But since then, rates went up to 5.25%, and are now at 4%, and hence the Bank has recently been paying out a hefty amount – tens of billions of pounds – in interest to high street banks.

Reform UK leader Nigel Farage (left) and deputy leader Richard Tice speaking to the media outside the Bank Of England in central London. Pic: PA

This, says Richard Tice, is an abomination. In the last Reform manifesto, he said the Bank should stop paying out those reserves. Which, on the face of it, sounds perfectly sensible. However, there are a few catches.

A big bank tax

The first is that while in theory it might help recoup billions of pounds of public money, that money has to come from somewhere, and in this case, it would come from high street banks. In other words, this is, in all but name, a very big bank tax. The Bank of England’s point, when asked about all this, is that if anyone is going to do something like that, it should really be the government, since it’s rightly in charge of taxing and spending.

Read more:

Co-op reveals £80m profit hit from cyber attack disruption – with more to come

Jaguar Land Rover cyber attack: No easy options for taxpayer aid

The other catch is that Bank of England reserves systems are desperately complex. Changing the way they’re structured is a delicate operation. Running a coach and horses through it, as Mr Tice is suggesting, could have all sorts of unintended consequences, including undermining confidence in UK economic policy.

This, by the way, is not the only thing Reform is unhappy about: they also think the Bank should slow down its quantitative tightening programme.

But the point of all the above is that while there are some big question marks about the particular idea Reform is proposing, the worst thing of all would be not to discuss this as publicly as possible.

The worst outcome of all would be for the government and Bank to take certain decisions which affect billions of pounds of public money with only the merest of scrutiny, save at the Treasury Select Committee, whose sessions rarely get much attention beyond the financial pages. And that is more or less the situation we’ve had for the past decade and a half.

The Bank of England has introduced one of the most radical monetary experiments in history, which may or may not have been a success or a failure, but few outside of the City are even aware of it. Mr Tice’s policy platform may be flawed, but his overarching point – that this stuff desperately needs more scrutiny – is quite right.

Jaguar Land Rover (JLR) “failed to finalise” a cyber insurance deal before it was struck by hackers last month, forcing a halt to production and threatening the future of its supply chain, according to an industry journal.

The Insurer, citing three insurance sector sources, said Britain’s biggest carmaker was still in negotiations over cover before the cyber attack at the end of August.

It opens the prospect that the company faces footing the bill for the hacking by itself.

Losses will easily run into many hundreds of millions of pounds, with its global factory shutdown set to last for a month at least.

Money latest: Rich Britons reveal the taxes they hate most

JLR shutdown extended

Marks and Spencer, which was targeted back in April, said it expected that the estimated £300m bill it was facing from the disruption would be largely offset by the cyber insurance cover it had taken out.

As frantic efforts continue at JLR to recover its systems, the government is exploring ways to support JLR’s supply chain and the 200,000 jobs within it.

One idea under consideration, according to ITV News, was taxpayer money being used to purchase parts.

These components could then be sold back to JLR as its manufacturing operations got back up to speed, resulting in no direct losses for the public purse.

Inside factory affected by Jaguar Land Rover shutdown

The “just-in-time” nature of automotive production means that many suppliers had little choice but to shut down immediately after JLR announced its manufacturing freeze.

Industry sources estimate that around 25% of suppliers have already taken steps to pause production and lay off workers, many of them by “banking hours” they will have to work in future.

Union demands for a COVID-style furlough scheme have not been taken up by ministers, who have said that support to date has come only from JLR.

Industry minister Chris McDonald said on a visit to a West Midlands manufacturer on Tuesday he was “supremely confident” that JLR would get through the cyber attack.

He added: “What I really want this to be is a wake-up call to British industry. I’m affronted by this attack on British industry. This is a serious attack on a flagship of British industry.”

Jaguar Land Rover said it declined to comment on commercial matters.

The government has also been approached for comment.

A cyber attack in April delivered an £80m hit to half-year operating profits at the Co-operative Group, it has been revealed.

The results showed an underlying pre-tax loss of £75m over the six months to 5 July compared to a profit of £3m over the same period a year ago.

The £80m figure included a £20m hit from one-off costs. The impact of the attack on sales revenue was estimated at £206m.

Money latest: Rich Britons reveal the taxes they hate most

While the mutual had insurance cover for operational disruption, it did not have a policy to meet full losses arising from a cyber incident.

It further revealed that the total profit damage was expected to nudge £120m over its full financial year.

Co-op was among several retailers hit in April, including M&S, and iall its members had data stolen.

A Co-op Group store is shown in Manchester during the height of the cyber attack disruption. Pic: PA

In-store, customers faced problems making payments initially and latterly empty shelves as the group struggled to restore control of key systems.

It prioritised rural stores for limited deliveries until stocks recovered in late May.

July: Four arrested over M&S, Co-Op and Harrods cyber attacks

Co-op chair Debbie White said: “The first half of 2025 brought significant challenges, most notably from a malicious cyber attack.

“Our balance sheet strength and the magnificent response of our 53,000 colleagues enabled us to maintain vital services for our members and their communities.

“We must now build our Co-op back better and stronger to meet the challenges and opportunities that lie ahead.”

The attacks on the retailers, which have resulted in four arrests, have brought the insurance issue to the fore as Jaguar Land Rover battles the impact of a similar attack.

Its factories are currently on track to produce nothing for at least a month and the government is now actively considering some kind of taxpayer support for its vast supply chain.

It has been reported that it was in discussions over cyber cover when its systems came under attack at the end of August.

Like the Co-op, it leaves the company facing the prospect of meeting many of the costs itself.

M&S put a £300m cost on the ransomware attack on its own systems ahead of Easter but expects to claw much of that money back through insurance payouts.

The government has this week described the run of hacking attempts as a further wake up call to the business community and urged continued investment in cyber security.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment12 months ago

Environment12 months agoHere are the best electric bikes you can buy at every price level in October 2024