US inflation hits highest level since 1990 as food and fuel prices surge

The annual rate of inflation in the US has hit its highest level in more than three decades, fed by faster than expected rises in the cost of fuel and food.

The headline consumer prices measure rose to 6.2% in October – a level not seen since 1990 – after a 0.9% surge on the previous month.

It represented a sharp acceleration in the cost of living that is being experienced globally, including the UK, as economies reopen from COVID-19 disruption but are hampered by supply struggling to keep pace with demand.

The bottlenecks have been exacerbated by worker shortages – hampering both production and deliveries.

President Biden has pledged action to tackle high fuel costs. File pic

The price surge is a concern because it risks harming spending power in the recovery from the pandemic disruption, but central banks can only do so much to limit the pace because things like energy costs are outside their control.

The US Federal Reserve and the Bank of England both last week maintained their views that much of the factors behind rising inflation are “transitory” – that they are temporary factors and inflation will fall back in the medium term.

But while the Fed took some action to take some heat out of the economy and prices, its counterpart in London stopped short of a policy response through an interest rate rise, as financial markets had expected.

The UK’s inflation rate currently stands at 3.1%, but is tipped to rise sharply when the next set of figures is released next week.

The Bank expects the CPI measure to rise above 5% next year.

‘Interest rate rise wouldn’t tackle supply issues’

In the case of the US, economists also believe there is more inflation to come, as factory gate data suggests higher costs in the early supply chain.

Sam Bullard, a senior economist at Wells Fargo, told the Reuters news agency: “Supply disruptions and the recovery of services poses a substantial concern that higher-than-expected inflation could persist for longer than the Fed believes.

“We expect goods inflation to hand the baton to services over the course of the next year, but all signs indicate that supply chain bottlenecks will keep fanning the flames on inflation in the near term.”

The country’s latest employment figures showed wage growth at an eight-month high.

President Joe Biden, who reacted to the figures by saying they were a “top priority”, is under pressure to help ease fuel prices by relaxing curbs on the country’s domestic oil producers after major oil-pumping nations snubbed last week his call to increase supply.

US pump costs are currently at seven-year highs ahead of the Thanksgiving and Christmas holidays on the back of a 60% rise in wholesale costs in the year to date.

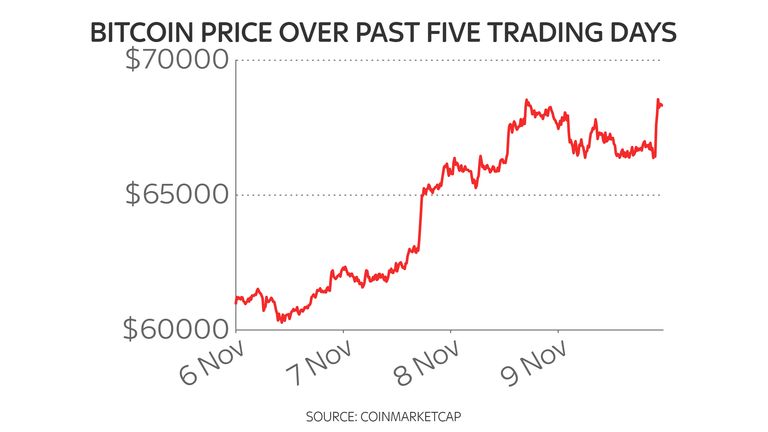

The dollar rallied and Bitcoin – increasingly seen as a new risk-off asset class – hit record highs in the wake of the inflation data, while stock markets fell back on Wall St as investors saw the prospect of a Fed U-turn ahead.

Craig Erlam, senior market analyst at ONADA, wrote: “It’s getting harder and harder for the Fed to describe inflation as transitory, and the response to today’s data suggests the narrative won’t work on investors anymore.

“The chances are, the central bank would have phased it out over the next couple of meetings anyway as it was losing credibility on that front, but today may have hastened that.”

Business

‘Knock-back for London’ as AstraZeneca sells shares directly on rival New York Stock Exchange

One of the UK’s most valuable listed companies is to sell its shares directly on the rival New York Stock Exchange, in a move described as a “knock back for London”.

While AstraZeneca will maintain its headquarters in the UK and its primary stock listing on the London Stock Exchange, the news can be seen as a move away from London.

“Although there has been no suggestion that AstraZeneca is imminently going to up sticks and move its primary listing from London, there may be some nervousness this morning around the risk that the UK market might lose one of its largest constituents,” said Russ Mould, the investment director of investment platform AJ Bell.

Read more:

AstraZeneca exit is a frightening prospect for the City and the government

The news “does at least hint at the possibility of a more dramatic shift at some point in the future”, Mr Mould said.

There may also be relief that AstraZeneca is not moving from the London Stock Exchange altogether.

“I think there is probably relief that it’s not pursuing a primary listing in New York, but the decision is hardly a ringing endorsement of London,” said Neil Wilson, the UK investor strategist at investment platform Saxo Markets.

“It reflects the fundamental, structural issues in the UK for the largest globally-oriented stocks – the depth and liquidity of its capital markets is falling short of what’s on offer across the pond.”

“It’s also a bit of a knock-back for London”, Mr Wilson said.

Why is the UK economy so volatile?

Why is this happening?

The Cambridge-based pharmaceutical company said the decision to sell shares directly on the New York Stock Exchange – rather than the previous less straightforward system of using American depository receipts – has been made to allow it “to reach a broader mix of global investors” and “make it even more attractive for all our shareholders”.

“The US has the world’s largest and most liquid public markets by capitalisation, and the largest pool of innovative biopharma companies and investors,” the company said in an announcement to investors.

AstraZeneca’s share price was up 0.7% on the news.

Jaguar Land Rover (JLR) has announced it will partially resume manufacturing “in the coming days” after nearly a month in the wake of a cyber attack.

The luxury car-making plants have paused production since 31 August. The cyber attack halted car-making across the supply chain, with staff off work as a result.

Money latest: Five parts of UK defying housing market

More than 33,000 people work directly for JLR in the UK, many of whom are on assembly lines in the West Midlands, with the largest facility located in Solihull, and a plant in Halewood on Merseyside.

Roughly 200,000 more are employed by several hundred companies in the supply chain, who rely on JLR orders as their biggest client.

“As the controlled, phased restart of our operations continues, we are taking further steps towards our recovery and the return to manufacture of our world-class vehicles,” a company spokesperson said.

The shutdown was said to last until at least 1 October.

Are we in a cyber attack ‘epidemic’?

“Today we are informing colleagues, retailers and suppliers that some sections of our manufacturing operations will resume in the coming days,” the company added, days on from the partial restart of its IT systems, which allowed supplier payments to recommence.

“We know there is much more to do, but the foundational work of our recovery is firmly underway, and we will continue to provide updates as we progress.”

Over the weekend, the government said it would underwrite a £1.5bn five-year loan guarantee to JLR.

The promise came as the head of the influential Business and Trade Committee of MPs wrote to Chancellor Rachel Reeves, warning small firms reliant on JLR, “may have at best a week of cashflow left to support themselves” with “urgent” action needed to support businesses.

JLR was just the latest business to be the subject of a cyberattack.

Harrods, the Co-Op, and Marks and Spencer, are among the companies that’ve struggled in the past year with such attacks.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment12 months ago

Environment12 months agoHere are the best electric bikes you can buy at every price level in October 2024