Why fear of growth setback has spooked investors

News of a potentially fast-spreading new coronavirus variant has already triggered a violent reaction on markets and in a number of different asset classes.

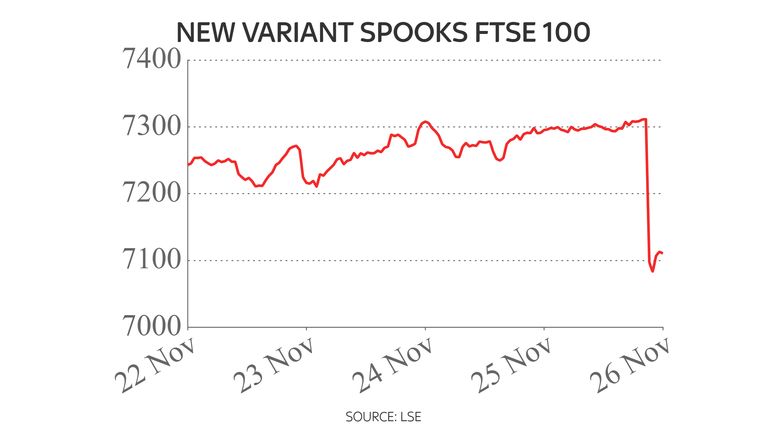

While much attention has naturally alighted on equity markets, with big falls in the FTSE-100 and continental European indices such as the DAX in Germany and the CAC-40 in France, probably the most significant move has been in the oil price.

At one point this morning, the price of a barrel of Brent crude fell to $77.28 – a level it has not seen since 24 September.

And, while a new coronavirus variant is undoubtedly unwelcome news, the fall in the price of oil may be one piece of good news emerging from the situation.

For a start, because oil prices move in close correlation to the price of other energy sources such as natural gas, a big decline will relieve inflationary pressures.

News of a fresh coronavirus variant has triggered a violent reaction on markets, including the FTSE 100

These, as was shown by this week’s co-ordinated release of crude reserves by the US, China and others, have been exercising governments in a number of countries.

It has also been exercising policy makers. The Bank of England has been dropping ever heavier hints of a looming increase in interest rates and, while it surprised the markets by not raising its main policy rate this month, at least one rise was being priced by the end of February next year.

But a sustained decline in the price of oil – and the threat to growth posed by the new variant – will relieve pressure on the Bank of England to act quickly and especially at a time when a number of members of the Bank’s Monetary Policy Committee are still extremely wary of the possible impact of even a modest increase in Bank Rate.

That is also the calculation markets have been making this morning about the US. Yields on US Treasuries (US government IOUs) have fallen this morning – the yield falls as the price rises – as investors started to reconsider the likely timing of the next rise in US interest rates.

The odds against an early rate hike from the US Federal Reserve had been shortening since, on Monday, President Joe Biden reappointed Jay Powell as chairman of the Fed rather than going for the more dovish Lael Brainard.

Those bets have now started to unwind as some investors calculate the spread of a new coronavirus variant could push back the timing of the Fed’s first hike.

Bank of England governor Andrew Bailey explains why it decided to hold interest rates at 0.1% – despite predicting inflation will hit 5% next year

A bigger concern, when it comes to the potential impact of another COVID variant, will be Europe. The main European economies have not rebounded from the pandemic as rapidly as the United States, as borne out on Thursday by confirmation of weaker-than-expected GDP growth in the third quarter of this year in Germany, the continent’s biggest economy.

Those concerns also apply to the UK, whose economy is further away from recapturing its pre-pandemic levels than any other country in the G7, other than Japan.

What is particularly striking about market reaction to this new variant is that it has been far more violent than the response, earlier this week, to new COVID lockdowns in Austria, Slovakia and other parts of continental Europe. On that occasion, investors calculated that spending prevented from taking place due to lockdowns would be merely deferred, not postponed altogether.

Markets around the world were down on Friday as news of a worrying new variant spooked investors

With the new variant, as so little information is currently available about the speed with which it can be transmitted and the impact it will have on sufferers, the same assumption cannot be made.

That explains the punishment meted out this morning to aviation stocks, such as International Airlines Group (IAG) and Lufthansa and tourism-related stocks, such as TUI, Intercontinental Hotels and Whitbread, the owner of the Premier Inn chain.

But it cannot be stressed how unknowable the situation is.

As Neil Shearing, group chief economist at the consultancy Capital Economics, put it in a note to clients this morning: “It goes without saying that it’s still too early to say exactly how big a threat the new B.1.1.529 strain poses to the global economy.”

Mr Shearing said there were three key points to make, though, the first of which is that – as Delta showed – it is very hard to stop the spread of virulent new variants. Secondly, it is the restrictions imposed in response to the virus, rather than the virus itself, that causes the bulk of the economic damage.

Thirdly, he said, the global economic backdrop is different than in previous waves, with supply chains already stretched, while labour shortages are widespread.

He added: “All of this will complicate the policy response. At the margin, the threat of a new, more serious, variant of the virus may be a reason for central banks to postpone plans to raise interest rates until the picture becomes clearer.

“The key dates are 15 December, when the Fed meets, and 16 December, when several central banks, including the Bank of England and European Central Bank, meet.

“But unless a new wave causes widespread and significant damage to economic activity, it may not prevent some central banks from lifting interest rates next year.”

Much will depend on what information comes from the World Health Organisation in coming days and how governments respond.

As Jim Reid, head of global fundamental credit strategy at Deutsche Bank, noted today: “At this stage very little is known. Mutations are often less severe so we shouldn’t jump to conclusions but there is clearly a lot of concern about this one.

Also South Africa is one of the world leaders in sequencing so we are more likely to see this sort of news originate from there than many countries.

“Suffice to say at this stage no one in markets will have any idea which way this will go.”

Exactly. At the moment, travel bans have only been imposed to and from six southern African countries. It may well be that, if the new variant has already taken hold elsewhere, there may be little point in imposing new travel restrictions.

But this is not a situation many investors either expected or wanted to return to. They have seen this story before. And they do not wish to be caught out in the way they were during earlier waves of the pandemic.

The world’s most valuable company, and first to be valued at $4trn (£2.9trn), beat market expectations in keenly anticipated financial results.

Microchip maker Nvidia recorded revenues of $46.7bn (£34.6bn) in just three months up to July, latest financial data from the company showed, slightly better than Wall Street observers had expected.

The company’s performance is seen as a bellwether for artificial intelligence (AI) demand, with investors paying close attention to see whether the hype is overblown or if significant investment will pay off.

Originally a creator of gaming graphics hardware, Nvidia’s chips help power AI capability – and the UK’s most powerful supercomputer.

Nvidia’s graphics processors underpin products such as ChatGPT from OpenAI and Gemini from Google.

Other tech giants – Microsoft, Meta and Amazon – make up Nvidia’s biggest customers and are paying large sums to embed AI into their products.

Why does it matter?

Nvidia has been central to the boom in AI development and the surge in tech stock valuations, which has seen stock markets reach record highs.

It represents about 8% of the value of the US S&P 500 stock market index of companies relied on to be stable and profitable.

Strong results will continue to fuel record highs in the market. Conversely, results that fail to live up to the hype could trigger a market tumble.

Read more business news:

Government costs to push up energy price cap

Wagamama owner among suitors for Costa

Is Trump’s AI plan a ‘tech bro’ manifesto?

Nvidia itself saw its share price rise more than 40% over the past year. Its value impacts anyone with cash in the US stock market, such as pension funds.

The S&P 500 rose 14% over the past year, and the tech-company-heavy NASDAQ gained 21%, largely thanks to Nvidia.

As such, its earnings can move markets as much as major economic or monetary policy announcements, like an interest rate decision.

Sir Keir Starmer with NVIDIA chief Huang at London Tech Week. Pic: AP

What next?

Revenue rises are forecast to continue to rise as Nvidia said it expected a rise to roughly $54bn (£40bn) in the next three months, more than the $53.14bn (£39.3bn) anticipated by analysts.

This excludes any potential shipments to China as export of Nvidia’s H20 chip, designed with the Biden administration’s export crackdown on advanced AI powering chips in mind, had been banned under US national security grounds.

But in recent weeks, Nvidia and another chipmaker, AMD, reached an unprecedented agreement to pay the Trump administration a 15% portion of China sales in return for export licences to send chips to China.

There were no H20 sales at all to China in the second quarter of the year, the period for which results were released on Wednesday evening.

Previously, 13% of Nvidia’s revenue came from China, with nearly 50% coming from the US.

Market reaction

Despite the expectation-beating results, Nvidia shares were down in after-hours trading, as the massive revenue rises previously booked by the company were not repeated in the latest quarter.

Compared to a year ago, revenues rose 56% and 6% compared to the three months up to April.

The absence of Chinese sales in forecasts appeared to disappoint.

A larger than expected hike in the energy price cap from October is largely down to higher costs being imposed by the government.

The typical sum households face paying for gas and electricity when using direct debit is to rise by 2% – or £2.93 per month – to £1,755, the energy watchdog Ofgem announced.

The current price cap is £1,720 a year. A 1% increase had been widely forecast.

The latest bill settlement, covering the final quarter of the year until the next price review takes effect from January, will affect around 20 million households.

Money latest: Should I fix? Reaction to energy price cap shift

There are 14 million others, such as those on pre-payment meters, who will also see bills rise by a similar level.

Those on fixed deals, which are immune from price cap shifts until such time as the term ends, currently stands at 20 million.

Wholesale prices – volatile since Russia’s invasion of Ukraine back in February 2022 – have been the main driver of rising bills.

But they are making little contribution to the looming increase.

Ofgem explained that government measures, such as the expansion of the warm home discount announced in June, were mainly responsible.

Bills must rise to pay for energy transition

The discount is set to add £15 to the average annual bill.

It will provide £150 in support to 2.7 million extra people this year, bringing the total number of beneficiaries to six million.

The balance is made up from money needed to upgrade the power network.

Tim Jarvis, director general of markets at Ofgem, said: “While there is still more to do, we are seeing signs of a healthier market. There are more people on fixed tariffs saving themselves money, switching is rising as options for consumers increase, and we’ve seen increases in customer satisfaction, alongside a reduction in complaints.

“While today’s change is below inflation, we know customers might not be feeling it in their pockets. There are things you can do though – consider a fixed tariff as this could save more than £200 against the new cap. Paying by direct debit or smart pay as you go could also save you money.

“In the longer term, we will continue to see fluctuations in our energy prices until we are insulated from volatile international gas markets. That’s why we continue to work with government and the sector to diversify our energy mix to reduce the reliance on markets we do not control.”

The looming price cap lift will leave bills around the same sort of level they were in October last year but it will take hold at a time when overall inflation is higher.

Inflation has gone up again – this explains why

Food price increases, also partly blamed on government measures such as the national insurance contributions hike imposed on employers, have led the main consumer prices index to a current level of 3.8%.

It is predicted to rise to at least 4% in the coming months, further squeezing household budgets.

Ministers argue that efforts to make the UK less reliant on natural gas, through investment in renewable power sources, will help bring down bills in future.

Energy minister Michael Shanks said: “We know that any price rise is a concern for families. Wholesale gas prices remain 75% above their levels before Russia invaded Ukraine. That is the fossil fuel penalty being paid by families, businesses and our economy.

“That is why the only answer for Britain is this government’s mission to get us off the rollercoaster of fossil fuel prices and onto clean, homegrown power we control, to bring down bills for good.

“At the same time, we are determined to take urgent action to support vulnerable families this winter. That includes expanding the £150 Warm Home Discount to 2.7 million more households and stepping up our overhaul of the energy system to increase protections for customers.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment11 months ago

Environment11 months agoHere are the best electric bikes you can buy at every price level in October 2024