Liz Truss’s ‘favourite’ economist says chancellor ‘took his eye off ball’ and ‘overstepped the mark’ with mini-budget

Prime Minister Liz Truss’s external adviser on the economy has told Sky News that the chancellor had “taken his eye off the ball” and “overstepped the mark” with his mini-budget.

Gerard Lyons, who is often referred to as Ms Truss’s favourite economist, said Chancellor Kwasi Kwarteng failed to adequately prepare the financial markets ahead of his announcement.

Speaking on The Take With Sophy Ridge, Mr Lyons said: “The chancellor, whilst he had focused on the general public and on British businesses, he had not really prepared the financial markets fully.

“And I think he had taken his eye off the ball slightly, shall we say, in having not prepared the markets for what he was doing in the budget and I felt that he overstepped the mark last week.

“So it was a combination of all three factors – the febrile markets because of the global backdrop, the actions of the Bank of England last Thursday, but let’s be in no doubt, it was primarily the mini-budget last Friday that triggered this latest series of events.”

Asked if he had had any conversations with Ms Truss or her team, Mr Lyons said he had “made my thoughts known”. He said he was “highlighting in my writing… about the febrile state of the markets and the need to keep the markets onside”.

Pushed on whether they had taken his advice, he said: “Well, sometimes people listen, sometimes they don’t, but there were positives that came out of it. But as we saw last Friday, there was just not enough in line with what the markets had been prepped for and were expecting.”

Despite his remarks, Mr Lyons said the budget was “very positive in many respects”.

He said it was “very much on a pro-growth agenda” which was needed to “break out of this low-growth phrase”.

‘Mini-budget not what the markets were expecting’

Mr Lyons’s remarks about the chancellor failing to prepare the financial markets were contrasted by a minister who told deputy political editor Sam Coates it was “bulls***t” to say market movement was related to the mini-budget announcement.

And on The Take with Sophy Ridge, chief secretary to the Treasury Chris Philp denied the government had any responsibility and said there would be no change of course.

Chief Sec bullish on tax cuts

Read more:

Ed Conway on the Bank’s extraordinary response

Liz Truss is a ‘danger to the economy’, Starmer says

Government departments asked for ‘efficiency savings’

“Getting Britain’s economy growing is so important. Important to raise wages and important to pay the tax bills of the future,” he said.

Mr Philp suggested benefits may not be hiked in line with spiralling inflation. He said a commitment by former chancellor Rishi Sunak to uprate benefits in line with inflation was under consideration amid reports different government departments have been asked to draw up plans for efficiency savings.

Mr Philp told ITV’s Peston: “We are going to look for efficiencies wherever we can find them.”

But he said the Treasury would not commit to an expected uprating of benefits in line with inflation.

Pressed about the decision, he said: “I am not going to make policy commitments on live TV, it is going to be considered in the normal way, we will make a decision and it will be announced I am sure in the first instance to the House of Commons.”

Subscribe to the Daily podcast on Apple Podcasts, Google Podcasts, Spotify, Spreaker

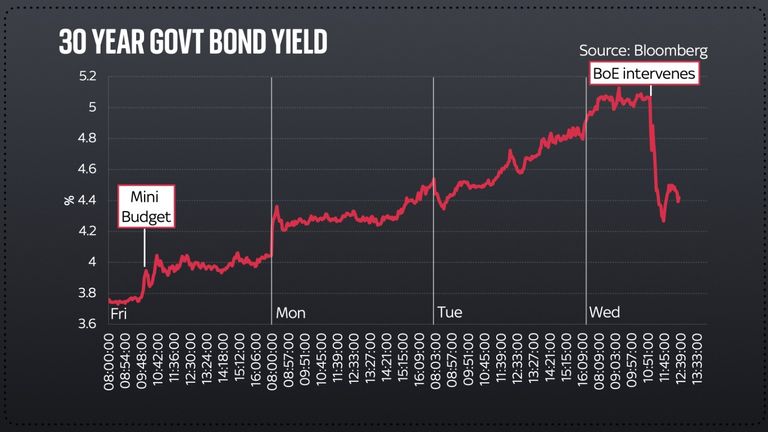

On Wednesday the Bank of England was forced to launch an emergency government bond-buying programme to prevent borrowing costs from spiralling out of control and stave off a “material risk to UK financial stability”.

The Bank will buy as many long-dated government bonds as needed between now and 14 October in a bid to stabilise financial markets.

The announcement had an immediate effect on the market, with data showing 30-year bond yields fell back to 4.3%, having risen to levels above 5% not seen since 2002, earlier on Wednesday. There were similar falls for 20-year yields.

Ms Truss is expected to face public questioning about her economic plans for the first time on Thursday as she tours regional BBC radio stations in a morning round of interviews. Neither the prime minister nor the chancellor were anywhere to be seen or heard on the economy on Wednesday.

Donald Trump has warned that all goods from Japan and South Korea will face tariffs of 25% from 1 August.

The announcement, via his Truth Social platform, marks the restart of the threatened “liberation day” escalation that was paused in April, for 90 days, to allow for negotiations to take place with all US trading partners.

The president showed off copies of letters to the leaders of both Japan and South Korea informing them of the tariff rates. Those duties will come on top of sector-specific tariffs – such as 50% rates covering steel – already in force.

Money latest: Retailers release images of ‘prolific shoplifters’

He warned the rates could be adjusted “upward or downward, depending on our relationship with your country”.

Country-specific tariffs had been due to take effect from Wednesday this week but Mr Trump had earlier revealed that nations would start to get letters instead, setting out the US position.

Duties would take effect from 1 August, without any subsequent deal being agreed, it was announced.

The letters sent to Japan and South Korea cited persistent trade imbalances for the rates and included the sentence: “We invite you to participate in the extraordinary Economy of the United States, the Number One Market in the World, by far.”

He ended both letters by saying, “Thank you for your attention to this matter!”

The European Union – the biggest single US trading partner – is among those set to get a letter in the coming days.

Mr Trump has also threatened an additional 10% tariff on any country aligning itself with the “anti-American policies” of BRICS nations – those are Brazil, Russia, India, China and South Africa and whose members also include Egypt, Ethiopia, Indonesia, Iran and the United Arab Emirates.

The UK, bar a massive shock U-turn, should be exempt.

What does the UK-US trade deal involve?

The country was the first to be granted a trade deal, of sorts, in May and the Trump administration has claimed many others had been offering concessions since the clock ticked down to 9 July.

The UK is not expected to face any changes to its current 10% rate due to the trade truce, which came into effect last week.

While UK-made cars aerospace products face no duties under a new quota arrangement, it still remains to be seen whether 25% tariffs on UK-produced steel and aluminium will be cancelled.

Can the UK avoid steel tariffs?

They could, conceivably, even be raised to 50%, as is currently the case for America’s other trading partners, because no agreement on eliminating the rate was reached when the government struck its deal in May.

It all amounts to more uncertainty for the UK steel sector.

A No 10 spokesman said on Monday: “Our work with the US continues to get this deal implemented as soon as possible.

“That will remove the 25% tariff on UK steel and aluminium, making us the only country in the world to have tariffs removed on these products.

“The US agreed to remove tariffs on these products as part of our agreement on 8 May. It reiterated that again at the G7 last month. The discussions continue, and will continue to do so.”

China and Vietnam have also secured some US concessions.

The dollar strengthened but US stock markets lost ground in the wake of the letters to Japan and South Korea being made public, with the broad-based S&P 500 down by 1%.

Stock markets in both Japan and South Korea were closed for the day but US-traded shares of SK Telecom and LG Display were down 7.5% and 5.8% respectively.

Shares in Elon Musk’s Tesla have reversed sharply over renewed concerns about his focus on the company’s recovery as he plots against Donald Trump.

Shares in the electric car firm plunged by more than 7% at the start of trading on Wall Street – taking about $71bn (£52bn) off its market value.

The stock has often come under pressure since Musk started his association with the president, latterly helping bring down federal government costs through a new department known as DOGE (Department of Government Efficiency).

Money latest: Call centre worker’s tips for getting discounts

But it is now suffering as their political relationship has soured.

Musk has publicly opposed the so-called “big, beautiful bill” – Mr Trump’s flagship tax cut and spending plans that received Congressional approval last week – since he left his DOGE role.

Musk wrote in a post on his X platform on 30 June: “It is obvious with the insane spending of this bill, which increases the debt ceiling by a record FIVE TRILLION DOLLARS that we live in a one-party country – the PORKY PIG PARTY!!”

Once the bill was passed, he created a poll on X, asking people if they would want him to launch the America Party.

Musk v Trump: ‘The Big, Beautiful Breakup’

He wrote on 4 July: “Independence Day is the perfect time to ask if you want independence from the two-party (some would say uniparty) system!”

The vote ended with 65.4% in favour of creating the party.

The formation of the America Party was announced the following day.

“By a factor of 2 to 1, you want a new political party and you shall have it! When it comes to bankrupting our country with

waste & graft, we live in a one-party system, not a democracy.”

“Today, the America Party is formed to give you back your freedom,” Musk posted.

Trump responded on his Truth Social account: “I am saddened to watch Elon Musk go completely ‘off the rails,’ essentially becoming a TRAIN WRECK over the past five weeks.

“He even wants to start a Third Political Party, despite the fact that they have never succeeded in the United States –

The System seems not designed for them.”

Trump threatens to ‘put DOGE’ on Musk

Trump has previously threatened to go after Tesla‘s government subsidies and contracts through the DOGE department to save “big” as their relationship deteriorated.

Such threats have also pressured the share price at Tesla.

It has suffered throughout Trump 2.0 and, in fact, has trended lower since last December – shortly after Mr Trump’s election win was confirmed.

Read more:

The Trump-Musk bust-up that everyone knew was coming

Musk hits out at Tesla succession claim

The possibility of tariff hits to the business, followed by actual tariff disruption, along with a consumer and investor backlash against Musk’s previous DOGE role have contributed to a 35% decline on the December peak.

The very absence of Tesla’s CEO dragged on the shares.

Tesla sales suffered globally as the trade war ramped up due to the imposition of tariffs by a government he supported, until the public row between him and the president began in early June.

Musk had only just renewed his 100% focus on Tesla and his other business interests by that time.

Tesla sales were down during the presidential election campaign last year and continued to decline, on a quarterly basis, during the first half of 2025.

Neil Wilson, UK investor strategist at Saxo Markets, said of the company’s share price woes: “Investors are worried about two things – one is more Trump ire affecting subsidies and the other more importantly is a distracted Musk.

“Investors had cheered Musk stepping back from frontline politics but are now worried he’s going to sucked back in and take his eye off Tesla.”

Business

Post Office scandal: Victims say government’s control of redress schemes should be taken away

Post Office scandal victims are calling for redress schemes to be taken away from the government completely, ahead of the public inquiry publishing its first findings.

Phase 1, which is due back on Tuesday, will report on the human impact of what happened as well as compensation schemes.

“Take (them) off the government completely,” says Jo Hamilton OBE, a high-profile campaigner and former sub-postmistress, who was convicted of stealing from her branch in 2008.

“It’s like the fox in charge of the hen house,” she adds, “because they were the only shareholders of Post Office“.

“So they’re in it up to their necks… So why should they be in charge of giving us financial redress?”

Nearly a third of Ms Hamilton’s life has been dominated by the scandal

Jo and others are hoping Sir Wyn Williams, chairman of the public statutory inquiry, will make recommendations for an independent body to take control of redress schemes.

The inquiry has been examining the Post Office scandal which saw more than 700 people wrongfully convicted between 1999 and 2015.

Sub-postmasters were forced to pay back false accounting shortfalls because of the faulty IT system, Horizon.

At the moment, the Department for Business and Trade administers most of the redress schemes including the Horizon Conviction Redress Scheme and the Group Litigation Order (GLO) Scheme.

The Post Office is still responsible for the Horizon Shortfall scheme.

Lee Castleton OBE

Lee Castleton OBE, another victim of the scandal, was bankrupted in 2007 when he lost his case in the civil courts representing himself against the Post Office.

The civil judgment against him, however, still stands.

“It’s the oddest thing in the world to be an OBE, fighting for justice, while still having the original case standing against me,” he tells Sky News.

While he has received an interim payment he has not applied to a redress scheme.

“The GLO scheme – that’s there on the table for me to do,” he says, “but I know that they would use my original case, still standing against me, in any form of redress.

“So they would still tell me repeatedly that the court found me to be liable and therefore they only acted on the court’s outcome.”

He agrees with other victims who want the inquiry this week to recommend “taking the bad piece out” of redress schemes.

“The bad piece is the company – Post Office Limited,” he continues, “and the government – they need to be outside.

“When somebody goes to court, even if it’s a case against the Department for Business and Trade (DBT), when they go to court DBT do not decide what the outcome is.

“A judge decides, a third party decides, a right-minded individual a fair individual, that’s what needs to happen.”

Pic: AP

Mr Castleton is also taking legal action against the Post Office and Fujitsu – the first individual victim to sue the organisations for compensation and “vindication” in court.

“I want to hear why it happened, to hear what I believe to be the truth, to hear what they believe to be the truth and let the judge decide.”

Neil Hudgell, a lawyer for victims, said he expects the first inquiry report this week may be “really rather damning” of the redress claim process describing “inconsistencies”, “bureaucracy” and “delays”.

“The over-lawyeringness of it,” he adds, “the minute analysis, micro-analysis of detail, the inability to give people fully the benefit of doubt.

“All those things I think are going to be part and parcel of what Sir Wynn says about compensation.

“And we would hope, not going to say expect because history’s not great, we would hope it’s a springboard to an acceleration, a meaningful acceleration of that process.”

June: Post Office knew about faulty IT system

A Department for Business and Trade spokesperson said they were “grateful” for the inquiry’s work describing “the immeasurable suffering” victims endured.

Their statement continued: “This government has quadrupled the total amount paid to affected postmasters to provide them with full and fair redress, with more than £1bn having now been paid to thousands of claimants.

“We will also continue to work with the Post Office, who have already written to over 24,000 postmasters, to ensure that everyone who may be eligible for redress is given the opportunity to apply for it.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike