Cost of living: Fuel prices could rise again as oil-producing states ponder output cut

There is a mounting risk that fuel prices could soon begin to rise again as major oil-producing countries ponder a big cut in output.

The Opec+ cartel, which includes Saudi Arabia and Russia among its main members, is expected by markets to reveal this week a collective target to reduce delivery by more than one million barrels per day.

The price of Brent Crude, which rose 4% on Monday in anticipation of such a cut, was up further during Tuesday’s trading – to just shy of $90 per barrel.

Follow live updates on the cost of living crisis

Opec+ is responding to weaker demand for oil globally as economies tackle high inflation though there is pressure from the West to maintain supply to help tame the pace of price rises.

While the current Brent price remains far below the early Russia-Ukraine war highs of above $120 per barrel, the recent weakness of the pound would be expected to contribute to pressure on UK pump prices, potentially adding to the cost of living crisis again according to motoring organisation the RAC.

That is because wholesale fuel, like oil, is traded in dollars.

‘Further pain at UK pumps’

RAC fuel spokesman Simon Williams told Sky News: “The extent of the (Opec+) cuts will be crucial, as will compliance from member countries throughout October.

“But one thing’s for sure, it’s likely to cause further pain for drivers at the pumps in the UK, particularly with the pound so weak against the dollar.

“If the cost of a barrel were to climb back up to $100, drivers at the current exchange rate would very soon see forecourts displaying prices around 175p a litre again, which is 12p more than the current UK average.”

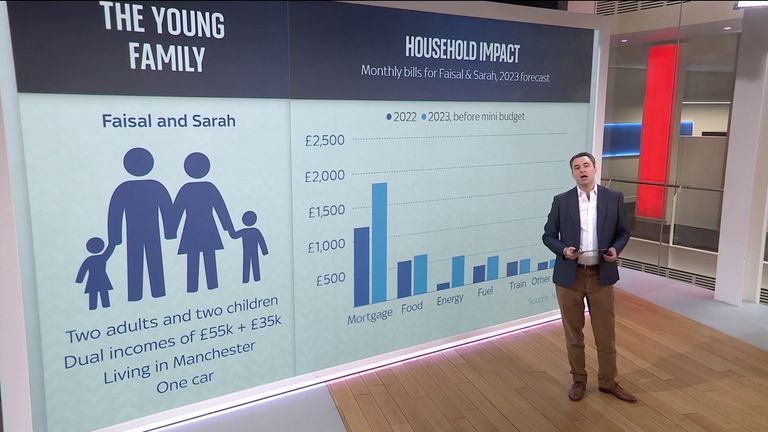

How rising costs will affect you

Average pump prices are currently 163p for unleaded and 180p for diesel – the latter remaining higher because of the loss of Russian supplies.

The pound was infinitely higher in value versus the US currency, around the $1.25 level, when petrol and diesel costs were hitting record levels daily in the spring following the Russian invasion.

It slumped to an all-time low of $1.03 last week in the wake of the government’s mini-budget when financial markets balked at the volume of giveaways and level of borrowing required to fund the growth programme.

How the markets are performing

It had recovered to just shy of $1.14 by Tuesday morning. That has been credited to government U-turns since Kwasi Kwarteng’s statement to the Commons and a weakening in the historic level of dollar strength.

The reason cited for the weakening was data suggesting the US economy was slowing faster than expected, raising the prospect of a pause to sharp US interest rate hikes.

Stock markets also recovered some poise as investors left the safety of the dollar, with the FTSE 100 putting on 1.5% in early dealing to take the index above the 7,000 points mark.

The more domestically-focused FTSE 250 was 2% higher.

Energy and commodity stocks were among those to enjoy the best gains as prices recovered from their recent recession -induced slump.

Opec sources told the Reuters news agency that voluntary output cuts by individual members could come on top of the group production reductions.

That being the case, it would amount to the largest output reduction since the start of the COVID pandemic in early 2020.

However, there were signs that the markets were yet to fully shrug off the fallout from the mini-budget that saw UK borrowing costs soar.

There were clear concerns around the UK’s credibility when the government raised £2.5bn on the bond markets.

The 0.5% of the 2061 (40-year) gilt on offer was sold at an average yield of 3.371%.

While that was the highest yield for any gilt sold at auction since 2014, it came in below that for a 30-year green bond syndicated last week.

It drew bids worth 1.97 times the volume on offer – the lowest bid-to-cover ratio since March.

Sir Alan Bates has reached a seven-figure deal to settle his claim over the Post Office Horizon scandal, more than 20 years after he began campaigning over what turned into one of Britain’s biggest miscarriages of justice.

Sky News has learnt that the government has agreed a deal with the former sub-postmaster after handing him what he described as a “take it or leave it” offer during the spring.

Sir Alan has previously said publicly that that proposal amounted to 49.2% of his original claim.

One source suggested that his final settlement may have been worth between £4m and £5m, implying that Sir Alan’s claim could have been in the region of £10m, although those figures could not be corroborated on Tuesday morning.

A government spokesperson said: “We pay tribute to Sir Alan Bates for his long record of campaigning on behalf of victims and have now paid out over £1.2bn to more than 9,000 victims.

“We can confirm that Sir Alan’s claim has reached the end of the scheme process and been settled.”

Sky News has attempted to reach Sir Alan for comment about the settlement of his claim.

Read more:

Victims say they’re treated like ‘second class citizens’

Who are the key figures in the scandal?

Victim died days before compensation letter arrived

Sir Alan led efforts over many years to prove that the Horizon software system supplied by Fujitsu, the Japanese technology company, was faulty.

Hundreds of sub-postmasters were wrongly prosecuted between 1999 and 2015, with scores of people either ending their own lives or making attempts to do so.

However, it was only after ITV turned their fight for justice into a drama, Mr Bates Vs The Post Office, that the government accelerated plans to deliver redress to victims.

Even so, the compensation scheme set up to administer redress has been mired in controversy.

Will Post Office victims be cleared?

Writing in The Sunday Times in May, Sir Alan described the process as “quasi-kangaroo courts in which the Department for Business and Trade sits in judgement of the claims and alters the goalposts as and when it chooses”.

“Claims are, and have been, knocked back on the basis that legally you would not be able to make them, or that the parameters of the scheme do not extend to certain items.”

Sir Alan had previously been made compensation offers worth just one-sixth of his claim – which he had labelled “derisory”, with a second offer amounting to a third of the sum he was seeking.

Sir Ross Cranston, a former High Court judge, adjudicates on cases where a claimant disputes a compensation offer from the government and then objects to the results of a review by an independent panel.

In 2017, Sir Alan and a group of 555 sub-postmasters sued the Post Office in the High Court, ultimately winning a £58m settlement.

However, swingeing legal fees left the group with just £12m of that sum, prompting ministers to establish a separate compensation scheme amid a growing outcry.

A significant number of other sub-postmasters have also complained publicly about the pace, and outcome, of the compensation process.

‘This waiting is just unbearable’

The first volume of Sir Wyn Williams’s public inquiry into the Horizon scandal was published in July, and concluded that at least 13 people may have taken their own lives after being accused of wrongdoing, even though the Post Office and Fujitsu knew the Horizon system was flawed.

The miscarriage of justice left the Post Office’s reputation, and that of former bosses including chief executive Paula Vennells, in tatters.

A subsequent corporate governance mess under the last government further dragged the Post Office’s name through the mud, with the then chief executive, Nick Read, accused of being absorbed by his own remuneration.

In recent months, the government has outlined a further redress scheme aimed at compensating victims of the Capture accounting software which was in use at Post Offices between 1992 and 2000.

Since then, a new management team has been appointed and has set the objective of boosting postmasters’ pay and overhauling technology systems to enable Post Office branches to offer a broader range of services.

Business

Money Problem: ‘My dad died and we didn’t cancel BT Sport for three years – now they won’t give our money back’

The US ambassador to the UK has said Britain should carry out “more drilling and more production” in the North Sea.

In his first broadcast interview in the job, Warren Stephens urged the UK to make the most of its own oil and gas reserves to cut energy costs and boost the economy.

“Electricity costs are four times ours in the UK, versus the US,” he told Mornings with Ridge and Frost.

“I want the UK economy to be as strong as it possibly can be, so the UK can be the best ally to the US that it possibly can be.

“Having a growing economy is essential to that – and the electricity costs make it very difficult.”

Mr Stephens told Wilfred Frost he hoped Britain would “examine the policies in the North Sea and frankly, make some changes to it that allows for more drilling and more production”.

“You’re using oil and gas, but you’re importing it. Why not use your own?” he asked.

Mr Stephens said Britain should make more of its own oil and gas

The ambassador said he had held meetings with Sir Keir Starmer on the energy issue while US President Donald Trump was in the room, and that the prime minister was “absolutely” listening to the US view.

“I think there are members of the government that are listening,” Mr Stephens told Sky News. “There is a little bit of movement to make changes on the policy and I’ll hope that will continue.”

Energy Secretary Ed Miliband has said the UK should be prioritising net zero by 2030 to limit climate change, rather than issuing new oil and gas drilling licences.

The Thistle Alpha platform, north of Shetland, stopped production in 2020 . Pic: Reuters/Petrofac

However, the ambassador said it would take “all energy for all countries to compete” in the future, given the huge power demands of data centres and AI.

“I don’t think Ed Miliband is necessarily wrong,” said Mr Stephens. “But I think it’s an incorrect policy to ignore your fossil fuel reserves, both in the North Sea and onshore.”

The ambassador hosted Mr Trump on the first night of his second UK state visit in September – a trip that was seen as a success by both sides.

Mr Stephens said Mr Trump and Sir Keir had a “great relationship” and pointed to the historic ties between Britain and the US as a major factor in June’s trade deal and the favourable tariff rate on the UK.

The ambassador said Sir Keir and President Trump have a ‘great relationship’

“The president really loves this country,” the ambassador told Sky News.

“I don’t think it’s coincidental that the tariff rates on the UK are generally a third, or at worst half, of what a lot of other countries are facing.

“I think the prime minister and his team did a great job of positioning the United Kingdom to be the first trade deal, but also the best one that’s been struck.”

Mr Stephens – who began his job in London in May – also touched on the Ukraine war and said Mr Trump’s patience with Russia was “wearing thin”.

The Alaska summit between Mr Trump and Vladimir Putin failed to produce a breakthrough, and the US leader has admitted the Russian president may be “playing” him so he can continue the fighting.

Read more from Sky News:

Trump accused of ‘new low point’ with refugee order

Trump’s opinion of Xi meeting brushes over thornier issues

The ambassador told Sky News he had always favoured a tough stance on Russia and was “delighted” when Mr Trump sanctioned Russia’s two biggest oil firms a few weeks ago.

However, he emphasised the president’s call that other countries must stop buying Russian energy to really tighten the screw.

“The president, has been, I would say, careful in ramping up pressure on Russia. But I think his patience is wearing out,” said Mr Stephens.

“One of the problems is a lot of European countries still depend on Russian gas,” he added.

“We’re mindful of that. We understand that, but until we can really cut off their ability to sell oil and gas around the world, they’re going to have money and Putin seems intent on continuing the war.”

The ambassador also struck a cautious but hopeful tone on future US and UK relations with China.

It comes after Mr Trump said his meeting this week with President Xi Jinping was a “12/10”, raising hopes the trade war between the superpowers could be simmering down.

China’s huge economy is too big to ignore – but it remains a major spy threat; the head of MI5 warned last month of an increase in “state threat activity” from Beijing (as well as Russia and Iran).

Mr Stephens praised the country’s economy and said it would be “terrific” if China could one day be considered a partner.

Trump-Xi meeting: Three key takeaways

But he warned “impatient” China is ruthlessly focused on itself only, and would like to see the US and the West weakened.

“There’s certainly things we want to be able to do with China,” added the ambassador.

“And I know the UK wants to do things with China. The United States does, too – and we should. But I think we always need to keep in the back of our mind that China does not have our interests at heart.”

:: Watch Mornings with Ridge and Frost on weekdays Monday to Thursday, from 7am to 10am on Sky News

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024