Lenders push Chancellor Kwasi Kwarteng to extend mortgage guarantee scheme

The UK’s biggest mortgage lenders will urge the chancellor to extend a government home loans initiative which helps first-time buyers get onto the property ladder.

Sky News understands that executives from major banks and Nationwide, Britain’s biggest building society, will ask Kwasi Kwarteng to commit to renewing the Mortgage Guarantee Scheme, which is scheduled to expire at the end of the year.

Launched in the spring of 2021, the scheme gives lenders an option to underwrite through the government the losses incurred on mortgages above 80% of the purchase price of a property.

The request to extend the scheme will form part of the banks’ agenda as they and the Treasury seek to address the disruption in the mortgage market following Mr Kwarteng’s ‘mini-Budget’ last month.

Lenders will also highlight the need for stability in financial markets in order to price home loans properly, and will flag potential risks under the City watchdog’s new ‘consumer duty’ from agreeing to unaffordable mortgage loans.

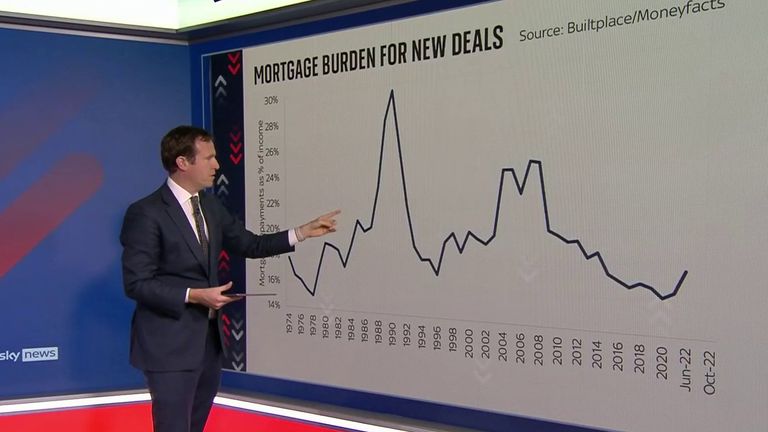

Hundreds of mortgage deals have been pulled or frozen by banks in the last fortnight as a result of volatility in how banks price such loans.

The chief executive of the City watchdog told The Sunday Times at the weekend that he wanted lenders to justify the withdrawal of fixed-rate mortgage products.

“If a product is withdrawn for a temporary period, we want to understand when they’re going to come back to market so that those people who may need to refinance are able to proceed with their plans,” Nikhil Rathi told the newspaper.

Executives from Barclays, Lloyds Banking Group and NatWest Group are among those expected to attend Thursday’s talks.

UK Finance, the banking trade association, will also be represented at the meeting, according to a Treasury source.

Sky’s Economics and Data Editor Ed Conway looks at the growing concerns over the state of the UK’s mortgage market.

After the meeting the Treasury confirmed the chancellor discussed his commitment to “fiscal discipline” and the importance of the financial sector in driving growth. He committed to working closely with the sector in the weeks and months ahead.

He is reported to have said the factors affecting rising mortgage costs are multifaceted and rates have been rising internationally, not just in the UK in response to his mini-budget announcement.

The cyber attack on Jaguar Land Rover (JLR), which halted production for nearly six weeks at its sites, cost the company roughly £200m, it has been revealed.

Latest accounts released on Friday showed “cyber-related costs” were £196m, which does not include the fall in sales.

Profits took a nose dive, falling from nearly £400m (£398m) a year ago to a loss of £485m in the three months to the end of September.

Money blog: Apple launches £220 iPhone ‘sock’ today – fans are divided

Revenues dropped nearly 25% and the effects may continue as the manufacturing halt could slow sales in the final three months of the year, executives said.

The impact of the shutdown also hit factories across the car-making supply chain.

Slowing the UK economy

The production pause was a large contributor to a contraction in UK economic growth in September, official figures showed.

Had car output not fallen 28.6%, the UK economy would have grown by 0.1% during the month. Instead, it fell by 0.1%.

How cyber attack ‘effectively hacked GDP’

Read more from Sky News:

Telegraph future in limbo again as RedBird abandons £500m deal

Reacting to JLR’s impact on the GDP contraction, its chief financial officer, Richard Molyneux, said it was “interesting to hear” and it “goes to reinforce” that JLR is really important in the UK economy.

The company, he said, is the “biggest exporter of goods in the entire country” and the effect on GDP “is a reflection of the success JLR has had in past years”.

Recovery

The company said operations were “pretty much back running as normal” and plants were “at or approaching capacity”.

Production of all luxury vehicles resumed.

Investigations are underway into the attack, with law enforcement in “many jurisdictions” involved, the company said.

When asked about the cause of the hack and the hackers, JLR said it was not in a position to answer questions due to the live investigation.

A run of attacks

The manufacturer was just one of a number of major companies to be seriously impacted by cyber criminals in recent months.

Are we in a cyber attack ‘epidemic’?

High street retailer Marks and Spencer estimated the cost of its IT outage was roughly £136m. The sum only covers the cost of immediate incident systems response and recovery, as well as specialist legal and professional services support.

The Co-Op and Harrods also suffered service disruption caused by cyber attacks.

Four people were arrested by police investigating the incidents.

Sir Keir Starmer and Rachel Reeves have scrapped plans to break their manifesto pledge and raise income tax rates in a massive U-turn less than two weeks from the budget.

The decision, first reported in the Financial Times, comes after a bruising few days which has brought about a change of heart in Downing Street.

Read more: How No 10 plunged itself into crisis

I understand Downing Street has backed down amid fears about the backlash from disgruntled MPs and voters.

The Treasury and Number 10 declined to comment.

The decision is a massive about-turn. In a news conference last week, the chancellor appeared to pave the way for manifesto-breaking tax rises in the budget on 26 November.

She spoke of difficult choices and insisted she could neither increase borrowing nor cut spending in order to stabilise the economy, telling the public “everyone has to play their part”.

‘Aren’t you making a mockery of voters?’

The decision to backtrack was communicated to the Office for Budget Responsibility on Wednesday in a submission of “major measures”, according to the Financial Times.

The chancellor will now have to fill an estimated £30bn black hole with a series of narrower tax-raising measures and is also expected to freeze income tax thresholds for another two years beyond 2028, which should raise about £8bn.

Tory shadow business secretary Andrew Griffith said: “We’ve had the longest ever run-up to a budget, damaging the economy with uncertainty, and yet – with just days to go – it is clear there is chaos in No 10 and No 11.”

How did we get here?

For weeks, the government has been working up options to break the manifesto pledge not to raise income tax, national insurance or VAT on working people.

I was told only this week the option being worked up was to do a combination of tax rises and action on the two-child benefit cap in order for the prime minister to be able to argue that in breaking his manifesto pledges, he is trying his hardest to protect the poorest in society and those “working people” he has spoken of so endlessly.

Ed Conway on the chancellor’s options

But days ago, officials and ministers were working on a proposal to lift the basic rate of income tax – perhaps by 2p – and then simultaneously cut national insurance contributions for those on the basic rate of income tax (those who earn up to £50,000 a year).

That way the chancellor can raise several billion in tax from those with the “broadest shoulders” – higher-rate taxpayers and pensioners or landlords, while also trying to protect “working people” earning salaries under £50,000 a year.

The chancellor was also going to take action on the two-child benefit cap in response to growing demand from the party to take action on child poverty. It is unclear whether those plans will now be shelved given the U-turn on income tax.

A rough week for the PM

The change of plan comes after the prime minister found himself engulfed in a leadership crisis after his allies warned rivals that he would fight any attempted post-budget coup.

It triggered a briefing war between Wes Streeting and anonymous Starmer allies attacking the health secretary as the chief traitor.

Wes Streeting: Faithful or traitor? Beth Rigby’s take

Read more: Is Starmer ‘in office but not in power’?

The prime minister has since apologised to Mr Streeting, who I am told does not want to press for sackings in No 10 in the wake of the briefings against him.

But the saga has further damaged Sir Keir and increased concerns among MPs about his suitability to lead Labour into the next general election.

Insiders clearly concluded that the ill mood in the party, coupled with the recent hits to the PM’s political capital, makes manifesto-breaking tax rises simply too risky right now.

But it also adds to a sense of chaos, given the chancellor publicly pitch-rolled tax rises in last week’s news conference.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024