Musk must complete Twitter deal by Oct. 28 to avoid trial, judge rules

A Delaware Chancery Court judge ruled Thursday that Elon Musk has until Oct. 28 to close his acquisition of Twitter if he wants to avoid a trial, granting Musk a slight delay.

Earlier in the day, the Telsa CEO said he wanted to return to his original agreement to buy Twitter for $54.20 a share, and asked the social media company to end all litigation in order to close the deal. Twitter refused to oblige.

In a filing with Delaware’s Court of Chancery on Thursday, Musk’s side said Twitter should drop the court date scheduled for Oct. 17, so that the necessary financing can be pulled together to wrap up the acquisition by Oct. 28.

“Twitter will not take yes for an answer,” the filing says. “Astonishingly, they have insisted on proceeding with this litigation, recklessly putting the deal at risk and gambling with their stockholders’ interests.” Musk argued that the trial would distract his team from securing the financing necessary to close the deal.

In this photo illustration, the image of Elon Musk is displayed on a computer screen and the logo of twitter on a mobile phone in Ankara, Turkiye on October 06, 2022.

Muhammed Selim Korkutata | Anadolu Agency | Getty Images

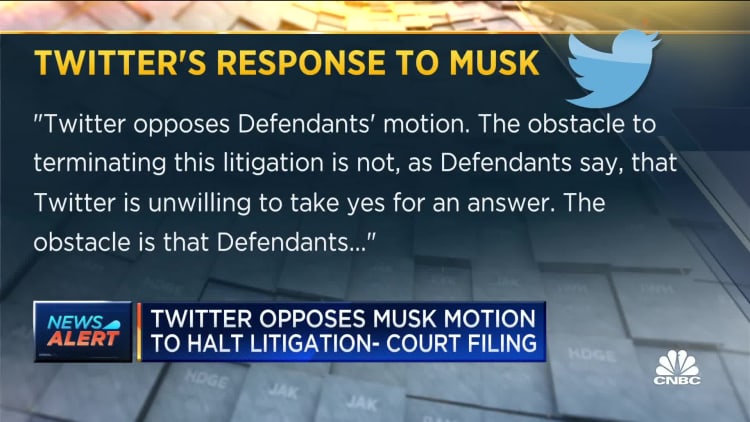

In a filing later on Thursday, Twitter responded by saying that Musk and his legal team are being disingenuous. Only days before a trial was to commence, Musk’s team suddenly declares “they intend to close after all,” the lawyers wrote.

“‘Trust us,’ they say, ‘we mean it this time,’ and so they ask to be relieved from a reckoning on the merits,” Twitter’s side said. “To justify that relief, they propose an order that allows them an indefinite time to close on the basis of a conditional withdrawal of their unlawful notices of termination coupled with an explicit reservation of all ‘claims and defenses in the event a closing does not occur.'”

The Twitter lawyers added that Musk’s “proposal is an invitation to further mischief and delay.”

Twitter sued Musk in July to try and force the world’s richest person to stick to his purchase agreement, which was signed in April. Musk appeared ready to take the case to court, as legions of his text messages were released in preliminary filings.

While Twitter shareholders, at the company’s recommendation, agreed to Musk’s purchase price in September, Twitter may now be reluctant to walk away from its lawsuit without certainty that all the financing is available to close the deal.

Morgan Stanley and Bank of America are among the banks that originally agreed to provide $12.5 billion in debt for Musk. Since then the markets have tanked, particularly for risky tech assets.

Musk’s attorneys said that “By far the most likely possibility is that the debt is funded in which case the deal will close on or around October 28.” The lawyers added that “counsel for the debt financing parties has advised that each of their clients is prepared to honor its obligations under the Bank Debt Commitment Letter on the terms and subject to satisfaction of the conditions set forth therein.”

Twitter said in the legal filing that the Musk parties “should be arranging to close on Monday, October 10,” but is instead refusing to “commit to any closing date.”

“They ask for an open-ended out, at the expense of Twitter’s stockholders (who are owed $44 billion plus interest), all the while remaining free to change their minds again or to invent new grounds to avoid the contract ‘[w]ithout any admission of liability and without waiver of or prejudice to [their] claims and defenses,'” the attorneys wrote.

The Twitter lawyers also alleged that earlier in the day, an unnamed corporate representative of one of the leading banks involved in the deal “testified that Mr. Musk has yet to send them a borrowing notice and has not otherwise communicated to them that he intends to close the transaction, let

alone on any particular timeline.”

“The bank further testified that the main task necessary to close the deal —memorializing the debt financing — could have happened in July but didn’t because Mr. Musk purported to terminate the deal,” the Twitter attorneys added.

Earlier this week, Twitter acknowledged that it had received the letter from Musk and his attorneys in which they expressed their wish to buy Twitter for the original agreed-upon price. Twitter said in a response to the letter that “The intention of the Company is to close the transaction at $54.20 per share.” However, this is the first time since then that Twitter has commented on the litigation.

Industrial and infrastructure stocks may soon share the spotlight with the artificial intelligence trade.

According to ETF Action’s Mike Atkins, there’s a bullish setup taking shape due to both policy and consumer trends. His prediction comes during a volatile month for Big Tech and AI stocks.

“You’re seeing kind of the old-school infrastructure, industrial products that have not done as well over the years,” the firm’s founding partner told CNBC’s “ETF Edge” this week. “But there’s a big drive… kind of away from globalization into this reshoring concept, and I think that has legs.”

Global X CEO Ryan O’Connor is also optimistic because the groups support the AI boom. His firm runs the Global X U.S. Infrastructure Development ETF (PAVE), which tracks companies involved in construction and industrial projects.

“Infrastructure is something that’s near and dear to our heart based off of PAVE, which is our largest ETF in the market,” said O’Connor in the same interview. “We think some of these reshoring efforts that you can get through some of these infrastructure places are an interesting one.”

The Global X’s infrastructure exchange-traded fund is up 16% so far this year, while the VanEck Semiconductor ETF (SMH), which includes AI bellwethers Nvidia, Taiwan Semiconductor and Broadcom, is up 42%, as of Friday’s close.

Both ETFs are lower so far this month — but Global X’s infrastructure ETF is performing better. Its top holdings, according to the firm’s website, are Howmet Aerospace, Quanta Services and Parker Hannifin.

Supporting the AI boom

He also sees electrification as a positive driver.

“All of the things that are going to be required for us to continue to support this AI boom, the electrification of the U.S. economy, is certainly one of them,” he said, noting the firm’s U.S. Electrification ETF (ZAP) gives investors exposure to them. The ETF is up almost 24% so far this year.

The Global X U.S. Electrification ETF is also performing a few percentage points better than the VanEck Semiconductor ETF for the month.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024