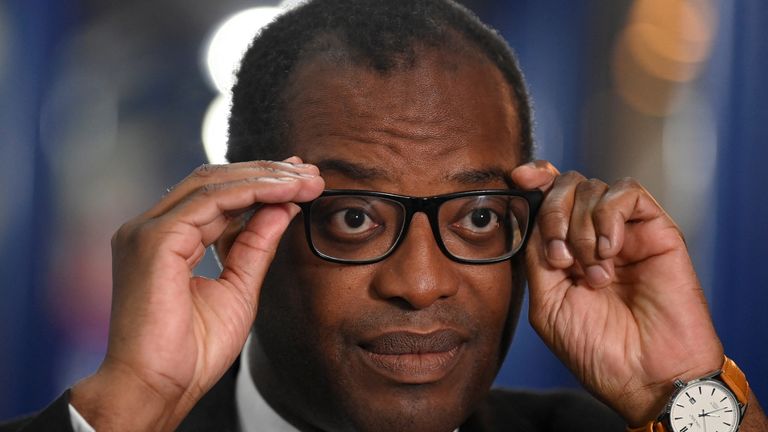

Chancellor Kwasi Kwarteng to return to London from Washington early as major mini-budget U-turn expected

Kwasi Kwarteng will return to the UK from Washington earlier than planned, as another major mini-budget U-turn is expected.

The chancellor was due to attend a final day of meetings at the International Monetary Fund’s annual gathering in Washington today.

Instead, after a hasty briefing with journalists late on Thursday, he announced he would fly home overnight.

Truss is out ‘and we have the numbers’, says Tory MP – politics latest

A source close to him dismissed suggestions that this represented a sign of panic and insisted that the chancellor’s focus was the medium-term fiscal plan.

Mr Kwarteng had been due to return to the UK from the annual IMF meeting later on Friday, but hasty changes were made.

Pressed on why there was a need for a last-minute schedule change, a Treasury source insisted that it was for talks on “the medium-term fiscal plan”.

The source said that the IMF trip had “put everything in a global context… a global set of challenges…”

On his return, the chancellor is likely to find a significant section of his mini-budget re-drawn following days of open revolt among Tory MPs and an expectation that another major U-turn is on the cards.

It comes amid speculation in Westminster about the fate of Mr Kwarteng, only a few weeks into the job, if his financial plans are scrapped in the coming days.

However, Mr Kwarteng has insisted that his position is safe, telling broadcasters: “I am not going anywhere.”

Pressure builds on Kwarteng

PM’s key pledge could be next casualty

Meanwhile, mounting pressure has been placed on Prime Minister Liz Truss to reassure the UK’s financial markets and rescue her administration, with her key pledge to scrap the planned increase in corporation tax from 19% to 25% widely seen as a likely casualty.

Former home secretary Priti Patel became the latest senior Tory to suggest the government could be forced into another U-turn, telling Sky News “market forces” could make a reversal on corporation tax cuts unavoidable.

Downing Street has not denied the policy could be reversed, despite it being one of Ms Truss’s landmark promises.

Former chancellor Rishi Sunak gave no comment when asked about the Truss government tax cuts

Several reports have also suggested that senior Conservatives are plotting the possibility of replacing Ms Truss with a joint ticket of Rishi Sunak and Penny Mordaunt.

The Times newspaper said party grandees are among those considering replacing her with a “unity candidate”.

Sky News understands Downing Street held talks on abandoning more elements of the £43bn tax-cutting mini-budget on Thursday, with proposed changes to corporation tax and dividend tax among the policies being considered.

Click to subscribe to the Sky News Daily wherever you get your podcasts

‘There are difficult choices’ to be made

Speculation surrounding the proposed changes have been fuelled by the chancellor following an interview he did with The Daily Telegraph.

Asked about the expectation that the government could ditch its corporation tax promise, Mr Kwarteng simply replied: “Let’s see”.

Read more:

What on earth is happening in UK markets?

What are bonds and where do they fit in the mini-budget crisis?

‘Don’t prolong the pain’

He also insisted there would be “no real cuts to public spending”, but added that “there are difficult choices” to be made.

“You have to make sure that you know the public is getting value for money. And I make no apologies for that, there has to be some sort of fiscal discipline,” he said.

Since his mini-budget announcement at the end of September, the UK’s financial markets have been reeling, with the Bank of England forced to intervene to restore some sense of stability.

Mini-budget caused ‘some turbulence’

‘Get on and do it – we all know it’s coming’

Not only did his policies spook markets, but they also caused anger among the Conservative Party, with some senior Tories calling for changes to be made.

Newly elected Foreign Affairs Committee Chair Alicia Kearns told LBC’s Tonight With Andrew Marr that she wanted the PM to succeed, but added her voice to calls for a change of course on the mini-budget.

She said: “The markets are not woke, the markets are not left. The fact they are not lefty, anti-government, the fact they have been spooked, is something that should be taken incredibly seriously.”

Former chancellor Ken Clarke told Sky News he has “never known a government to make such a catastrophic start”.

‘Catastrophic start’ – Ken Clarke slates Truss

Former veterans minister Johnny Mercer also tweeted that the situation “needs a course correction” from Number 10.

“Get on and do it – we all know it’s coming,” he wrote.

The government’s plans revolve around securing an increase in economic growth – with a target of an annual rise of around 2.5% in gross domestic product.

The crucial date will be 31 October, when the forecasts presented by the Office for Budget Responsibility alongside the chancellor’s statement will give an assessment on whether such a plan is realistic.

Business

Budget 2025: Hospitality pleads for ‘lifeline’ as Rachel Reeves accused of imposing ‘stealth tax’

Rachel Reeves has been accused of failing to “support the great British pub” as she promised in the budget, with owners facing skyrocketing business rates bills.

In her speech in the House of Commons on Wednesday, the chancellor said she was backing small businesses by introducing “permanently lower tax rates for over 750,000 retail, hospitality and leisure properties – the lowest tax rates since 1991”.

But while the government gave itself the powers to discount the business rates bills for high street businesses through legislation earlier this year, the chancellor only implemented a reduction of a quarter of what the government is able to, and she is being accused of imposing a “stealth tax”.

It has left small retail, hospitality, and leisure businesses questioning whether their businesses will be viable beyond April next year.

Sky’s Ed Conway looks at the aftermath of the budget and explains who the winners and losers are.

A Treasury spokesperson said: “We’re protecting pubs, restaurants and cafes with the budget’s £4.3bn support package – capping bill rises so a typical independent pub will pay around £4,800 less next year than they otherwise would have.

“This comes on top of cutting licensing costs to help more venues offer pavement drinks and al fresco dining, maintaining our cut to alcohol duty on draught pints, and capping corporation tax.”

Business rates, which are a tax on commercial properties in England and Wales, are calculated through a complex formula of the value of the property, assessed by a government agency every three years, combined with a national “multiplier” set by the Treasury, giving a final cash amount.

Chancellor Rachel Reeves has been accused of imposing a “stealth tax” on hospitality businesses. Pic: PA

Over the last few years, small businesses were given business rates relief of 75% to support them over the COVID pandemic, and Ms Reeves reduced that to 40% at last year’s budget.

The idea was that at the budget this year, the chancellor would remove that remaining relief in favour of reforming the business rates system to compensate for that drop, while shifting the tax burden on to much bigger businesses and companies like Amazon with lots of warehouse space.

However, the chancellor only announced a 5p in the pound discount for small retail, hospitality, and leisure businesses, rather than the assumed 20p drop which the government gave itself the powers to implement, and which trade bodies had been lobbying for.

How will your personal finances change following the budget announced by the chancellor?

On top of that, small businesses have seen the government-assessed value of their property increase dramatically, which wipes out the discount, and sees their business rates bill shoot far above what they had previously been paying.

One pub owner near Hull, Sam Caroll, has seen the assessed value of one of his two properties increase from £67,000 to £110,000 in just three years – a 64% increase.

He told Sky News that there is a “continual question” of business viability, and while he thinks they can “adapt” in the short term, “there will be a tipping point at some point”. Even at the moment, packing out their pubs seven nights a week, “it’s difficult for us to break even”, he said.

There will be a discount for small businesses to transition to the higher business rates level, but by year three, almost the full amount is expected to be payable, and Mr Carroll described it as “getting f***** slowly, instead of getting f***** overnight”.

👉 Listen to Sky News Daily on your podcast app 👈

Sean Hughes, who owns multiple hospitality venues in St Albans, has also seen vast increases in the assessed value of his properties, and was sharply critical of the transitional arrangements the government is implementing.

He told Sky News: “Fundamental business rate reform was promised and we have total chaos. If [the system] was fair, why would they need transitional relief periods?”

A spokesperson of the Valuation Office Agency (VOA), which assesses the value of commercial properties for business rates purposes, told Sky News: “At the last revaluation, some sectors including hospitality were significantly affected by the pandemic, which resulted in much lower rateable values than they would have seen otherwise. Businesses that have now seen a recovery in trade are also likely to see an increase in their rateable value.”

Read more:

Reeves accused of deliberately making UK finances look worse

Budget is a big risk for Labour’s election plans

However, Sky News has seen evidence of businesses whose assessed value did not decrease when assessed during the pandemic, but actually rose, and has risen dramatically this year.

Data compiled by the Pubs Advisory Service, shows that the number of pubs in the UK has decreased by nearly 5% in three years, but the average value of the properties has risen by an average of 36.82% per pub.

And analysis by UK Hospitality, the trade body that represents hospitality businesses, has found that over the next three years, the average pub will pay an extra £12,900 in business rates, even with the transitional arrangements, while an average hotel will see its bill soar by £205,200.

The prime minister has defended the budget after he and the chancellor were accused of breaking their promise to voters.

The body adds that by 2028/29, an average pub’s business rates will have increased by 76% and an average hotel’s by 115%, compared to 16% for a distribution warehouse like the ones the web giants use.

It’s not just the business rates rise that is worrying owners – it is the increase in employers’ national insurance implemented at the last budget, the increase in energy bills over the last few years, and the rise in the minimum wage, particularly for young people.

With the budget set to squeeze disposal income, there is little room for price increases to make up the shortfall either.

In a letter to the chancellor on Friday, Liberal Democrat deputy leader Daisy Cooper said small business owners “have been pushed to tears as they’re hit with the bombshell of higher business rates bills”, noting that “the government has chosen not to use the full powers it gave itself to throw high streets a lifeline”.

She added that businesses had been promised “permanently lower business rates”, but it appears the government has “broken yet another promise, by imposing a stealth tax not just on people, but on treasured high street businesses too”, and called on ministers to “throw our high streets and Britain’s hospitality sector a lifeline”.

Conservative shadow business secretary Andrew Griffith published his own analysis of the government’s budget measures on Friday morning, that found they will “hammer British pubs”.

Of the chancellor, he said: “She pretended in her budget speech to be supportive, whilst the true detail is that a combination of rate revaluations and scrapping reliefs will leave most pubs paying thousands of pounds more than they cannot afford.”

Kate Nicholls, Chair of UKHospitality, said in a statement: “The government promised in its manifesto that it would level the playing field between the high street and online giants. The plan in the budget to achieve this is quickly unravelling, and will deliver the exact opposite.”

She said they “repeatedly warned the Treasury” of the impending impacted of the value reassessment, but nonetheless, hospitality businesses are now facing “eye-watering increases”.

She added: “We agree with its reforms to deliver permanently lower business rates for hospitality and we appreciate the package of transitional relief, but its current proposal is not delivering lower bills. A 20p discount for hospitality would. We urge the chancellor to revisit.”

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024