Having sealed her chancellor’s fate, the markets could seal the prime minister’s fate

So farewell, then, Trussonomics.

The demise of the country’s second shortest-lived chancellor also brings with it the demise of the country’s shortest-lived economic movement.

Liz Truss came into office promising to boost the country’s growth rate through a forensic combination of tax cuts, reforms to the country’s supply side (for which read: things like planning reform) and spending restraint. This was, if you squint a little bit, not dissimilar to the kinds of policies espoused by Ronald Reagan and Margaret Thatcher.

Tory MPs turn on Truss as PM scrambles to save job after sacking chancellor – latest updates

It always looked risky – especially at such a fragile point for the global economy. We are coming to the end of a 12-year period of cheap money, something which is causing a near-nervous breakdown in financial markets. Central banks are in the process of raising interest rates and trying to feed the glut of bonds they bought during the financial crisis back in the market.

As if that weren’t enough, Europe is facing one of its bleakest economic winters in modern memory, with a war raging in Ukraine and energy prices touching historic highs. It is hard to think of many less auspicious periods to attempt an untested new economic manifesto.

Yet Ms Truss and her former chancellor Kwasi Kwarteng pushed on all the same. And unlike Thatcher, whose first few budgets were grisly austerity packages which no one much enjoyed, Ms Truss and Mr Kwarteng aimed to turn Thatcherism on its head. Instead of fixing the public finances first and then cutting taxes second, they opted to spend the fruits of economic growth before that growth had even been achieved.

The mini-budget of 23 September was a small document with extraordinarily large consequences. Ironically, the more expensive the measures were, the less controversial they turned out to be. The scheme to cap household energy unit costs will potentially cost hundreds of billions of pounds, yet (and we know this because it was pre-announced long before the mini-budget) investors barely batted an eyelid. They carried on lending to this country at more or less the same or equivalent rates.

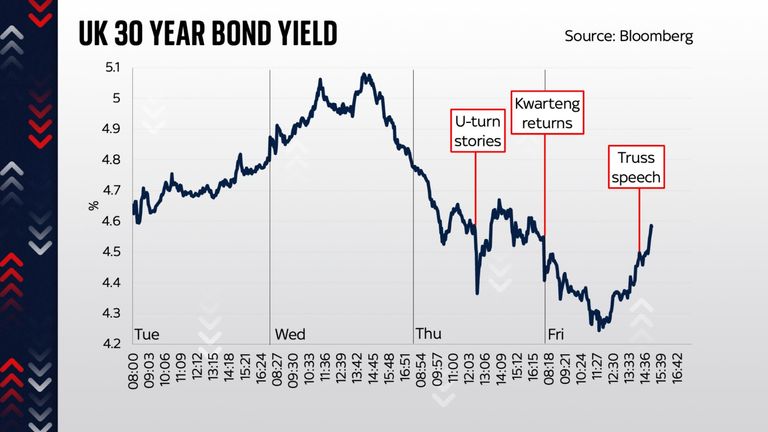

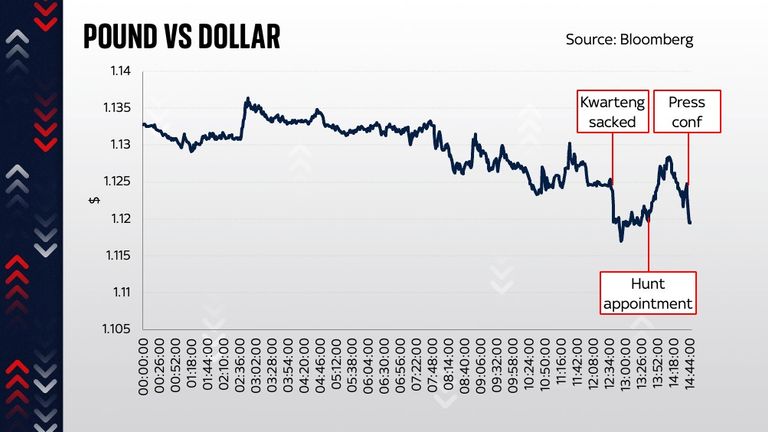

The same was not the case for the rest of the mini-budget’s policies. Shortly after they were announced – everything from the abolition of the 45p rate (actually quite cheap in fiscal terms) to the cancellation of Rishi Sunak’s corporation tax rise – markets began to lurch in what was, for Ms Truss, and most UK households, the wrong direction. The pound sank, the yields on government debt, which determine the interest rates across most of the economy, began to climb.

That was bad enough. When Mr Kwarteng announced gleefully a couple of days later on television that he had more tax cuts up his sleeve, the trot out of the country became a stampede. The pound fell, briefly, to the lowest level against the dollar in the history of, well, the dollar.

Even more worryingly, those interest rates on government bonds rose at an unprecedented rate, causing all sorts of malfunctions throughout the money markets.

The most obvious – and the one that perhaps will have the longest legacy – is the rise in mortgage rates. But the unexpected consequences were even more worrying, among them a crisis in funds used by pension schemes. That sparked a “run dynamic” which compelled the Bank of England to step in with an emergency support scheme.

Even at this point, we were into unprecedented territory. Never before had the Bank been forced to intervene quite like this. Never before had it had to do so as a result of a government’s Budget.

The intervention, however, had some success, bringing down the relevant interest rates and bringing markets back from the edge. But there was a sting in the tail: a deadline. Today, 14 October.

Analysis: PM’s new tax U-turn

In hindsight perhaps it’s obvious that this, then, would always have been the day when the government might face another existential crisis. Investors were always going to be nervous ahead of the Bank’s withdrawal from this neck of the bond market. And that is precisely what happened: after the governor reiterated, on a panel in Washington, that he was indeed serious, all eyes then turned to the chancellor. Could he say something to reassure markets?

In the event, the answer was: no. But something else changed matters: growing rumours of a U-turn. That brings us to this morning. The chancellor, pulled back from Washington early, was dismissed. The U-turn began. The corporation tax freeze is to be abandoned. The coming medium-term fiscal plan will involve austerity and a big dose of fiscal pain. The upshot is that Trussonomics, which was hinged clearly on tax cuts like these, is dead in the water.

However, the bigger question concerns what happens next. Those markets, which Ms Truss said explicitly were the reason for her U-turn, are still pretty frantic. No one knows how they’ll fare on Monday, but, whether right or wrong, another grisly day will almost certainly be seen as a sign of the government’s failure. And, having sealed the fate of her chancellor, the markets could well seal the fate of the prime minister.

But that’s a few days away – a long time in both politics and markets.

Liz Truss appoints Jeremy Hunt as chancellor. Pic: Andrew Parsons / No 10 Downing Street

In the meantime, here is something to dwell on: an alternative version of history. In a parallel universe, Ms Truss and Mr Kwarteng did things slightly less hastily. They decided their emergency Budget would simply deal with the energy price shock coming this winter. They promised an OBR statement and hatched plans for a growth-generating budget in a few months’ time.

In that parallel universe, interest rates probably wouldn’t have risen so high. The rises would, anyway, have been blamed on the Bank of England, not the government. The government would have enjoyed some kudos for having prevented energy-related penury this winter and made merry in their honeymoon. Things could have been oh-so different.

Click to subscribe to the Sky News Daily wherever you get your podcasts

Now, all of this is of course imponderable. But it does rather underline an important point: none of this was inevitable. This wasn’t a crisis like 1992 – where the UK faced monetary pressures suffered by nearly every other nation in Europe. It was simply a succession of very unfortunate decisions at precisely the wrong moment.

At a time of market turmoil and war in Europe, Ms Truss and Mr Kwarteng chose to take a gamble. It did not pay off.

:: The new chancellor, Jeremy Hunt, will talk to Sky News tomorrow morning. Tune in from 7am on Saturday.

The first-ever Capture case has been delayed at the Court of Appeal as the Post Office asks for an extension to respond, Sky News has learned.

Pat Owen, a former sub postmistress who has since passed away, was convicted of stealing in 1998 based on evidence from computer software.

The system, known as Capture, was used in up to 2,500 branches in the 1990s, before the infamous Horizon system was introduced.

Hundreds of sub-postmasters were wrongfully convicted between 1999 and 2015 as part of the Horizon scandal.

Earlier this year, Sky News unearthed a 1998 report showing the Capture software was also faulty.

That report, commissioned by the solicitors acting for Mrs Owen in 1998, was served on the Post Office and may never have been seen by the jury in her case.

‘All we want is her name cleared’

Ms Owen was given a suspended prison sentence and fought to clear her name subsequently – but died in 2003.

Her case was referred by the Criminal Cases Review Commission (CCRC) to the Court of Appeal in October.

The Post Office had until 5 December to respond to papers put forward by Mrs Owen’s defence team but they have now asked for an extension until 30 January.

Ms Owen’s daughter, Juliet Shardlow, described the family’s suffering at the lengthening wait.

“I need to emphasise the profound impact the ongoing delay is having on our family,” she said.

“The continuous uncertainty only compounds our heartache, stress, and anxiety.

Alan Bates: New redress scheme ‘half-baked’

“It has become the last thing I think about before I go to sleep and the first thing when I wake up.

“We have waited 27 years for justice, and this additional wait feels never-ending.”

Ms Owen’s case is the first time a conviction based on Capture has reached the Court of Appeal since the scandal was exposed.

Read more from Sky News:

Corporate manslaughter charges considered in Post Office scandal

21 ‘Capture’ cases investigated for miscarriages of justice

Lawyers have said that if Ms Owen is exonerated posthumously, it may “speed up” the handling of others.

CCRC chair Dame Vera Baird also told Sky News in the summer it could be a “touchstone case” for other victims.

The CCRC is also continuing to investigate around 30 other “pre-Horizon” convictions.

A Post Office spokesperson said: “We have sought an extension of time to fully consider and respond to the CCRC’s Statement of Reasons in Ms Owen’s case.

“We deeply regret the impact our request for further time will have on Ms Owen’s family.

“We have a duty to carefully consider the evidence presented in the Statement of Reasons submitted by the CCRC and do everything we can to fully assist the Court when it considers this conviction.”

Meanwhile, the first-ever redress scheme for victims of the Post Office Capture IT scandal was launched this autumn.

The Capture Redress Scheme will provide payments of up to £300,000, and more in “exceptional” cases, to former postmasters who suffered financial losses.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024