Markets react negatively to Truss speech despite positive response to government U-turn on mini-budget

The financial markets have responded positively to the government’s anticipated U-turn on parts of its massive mini-budget programme of unfunded tax cuts and energy price cap spending.

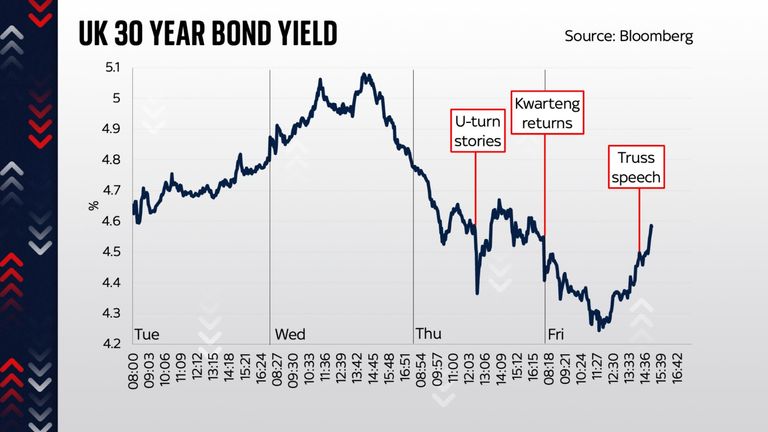

Despite initial positive moves in the market on Friday the response to Liz Truss’s U-turn speech on Friday afternoon has been negative.

UK government borrowing, necessary for planned large amounts of state spending, has become more expensive since Truss’s announcement.

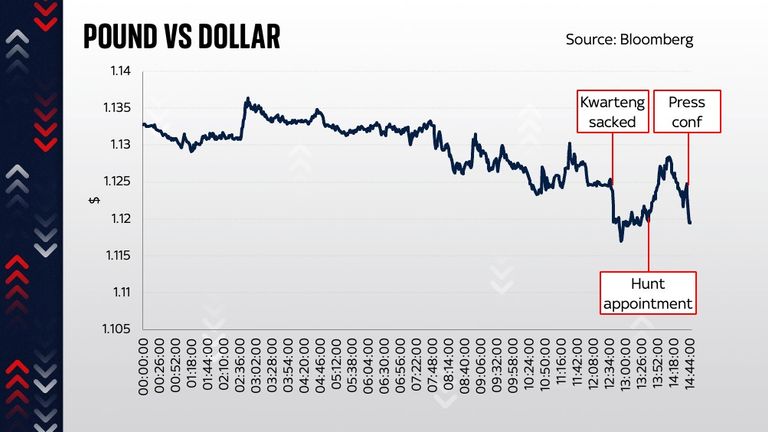

Paying for goods in US dollars, as importers do, has also become more expensive as the pound slid in value. Drops in the value of the pound signal a lack of confidence from investors in the UK market.

Markets had already priced in the government’s policy U-turn as the interest rate payments on long-dated government bonds, effectively state IOUs, sunk on Friday morning while the pound rose against the dollar and the euro.

As a result of the government’s rise in corporation tax, instead of the reduction it announced in the mini-budget, government bonds, known as gilts, fell. The measure is expected to add £18bn to state coffers.

These are the bonds that have had to be bought up as part of the Bank of England’s unprecedented intervention in the market to prevent a collapse in pensions as the market doubted the credibility of the UK’s economic plans.

The interest rate on long-dated gilts, which is the effective cost of government borrowing, fell steeply on Friday.

The interest rates had risen sharply following the mini-budget announcement, causing a massive sell-off, before the Bank announced its 13-day intervention on 28 September. That intervention is to end on Friday afternoon.

The 30-year gilts fell from near a high of 5% on Thursday following Sky News’s announcement of the U-turn, to 4.3% on Friday.

Similarly 20-year gilts fell from near a high of 5% to 4.42%.

The fall in the interest rate of the benchmark 10-year government gilt was also large, from 4.3% on Thursday to slightly above 4% on Friday.

The pound also saw a rise against the dollar, up from $1.11 on Thursday to $1.13 on Friday morning, before settling at around $1.12 on Friday afternoon, despite a dip in the wake of the sacking of Kwasi Kwarteng.

Markets are now also betting the Bank of England’s base interest rate, which determines the cost of borrowing in the UK, is going to be lower than had been expected earlier this week. A rate of 5.25% is now forecast, the lowest rate forecast since the money budget and a large drop from the 5.75% that was priced by UK money markets on Thursday.

That reduction is likely to reduce mortgage rates which had steadily risen since the mini-budget announcement as lenders pulled mortgage products from the market amid uncertainty over how much the Bank of England would raise rates.

On Friday morning there were 3,112 mortgage products on the market, still lower than before the mini-budget was announced, but an increase from the ten year low of 2,258 mortgages available on 1 October.

Mortgage rates had risen significantly since the mini-budget date on 23 September. On Friday the average interest rate on a two-year fixed term mortgage was 6.47%, and 6.29% on a five-year fixed term mortgage was. It’s nearly a 2% increase from the 4.74% and 4.75% average rates for two and five-year fixed term mortgages that existed prior to the mini-budget.

Sir Keir Starmer will deliver a speech today defending the decisions the government made in the budget, following criticisms of sweeping tax rises and accusations the chancellor lied to the country about the state of public finances.

The prime minister is expected to set out how the budget, which saw £26bn of tax rises imposed across the economy, “moves forward the government’s programme of national renewal”, and set “the right economic course” for Britain, Downing Street says.

He will also confirm that ministers will try again to reform the “broken” welfare system, after Labour MPs forced the government to U-turn on its plans to narrow the eligibility for Personal Independence Payments (PIP) earlier this year.

Sir Keir Starmer will give a speech later defending last week’s budget. Pic: Reuters

‘Of course I didn’t’ lie about public finances, says Reeves

“We have to confront the reality that our welfare state is trapping people, not just in poverty, but out of work – young people especially. And that is a poverty of ambition,” Sir Keir will say.

“And so while we will invest in apprenticeships and make sure every young person without a job has a guaranteed offer of training or work, we must also reform the welfare state itself – that is what renewal demands.”

Sky’s Ed Conway looks at the aftermath of the budget and explains who the winners and losers are

The prime minister will add: “This is not about propping up a broken status quo. Nor is it because we want to look somehow politically ‘tough’. The Tories played that game and the welfare bill went up by £88bn. They left children too poor to eat and young people too ill to work. A total failure.”

Instead, he will argue it is about “potential”, saying: “If you are ignored that early in your career, if you’re not given the support you need to overcome your mental health issues, or if you are simply written off because you’re neurodivergent or disabled, then it can trap you in a cycle of worklessness and dependency for decades, which costs the country money, is bad for our productivity, but most importantly of all – costs the country opportunity and potential.

“And any Labour Party worthy of the name cannot ignore that. That is why we have asked Alan Milburn on the whole issue of young people, inactivity and work. We need to remove the incentives which hold back the potential of our young people.”

The announcement will come after the Conservative opposition described the budget as one for “benefits street”, following the chancellor’s decision to lift the two-child benefit cap from April, at a cost of £3bn.

Prime Minister defends the budget

‘Government must go further and faster on growth’

The prime minister is also expected to launch a staunch defence of the budget overall, saying it will bear down on the cost of living through measures like money off energy bills and frozen rail fares; increase economic stability; and protect investment in public services and infrastructure that will drive economic growth.

He will argue that “economic growth is beating the forecasts”, but that the government must go “further and faster” to encourage it.

He will also reiterate his vow to scrap regulation across the economy, which he will argue is not only pro-business, but also a way to deal with the cost of living.

How will your personal finances change following the budget announced by the chancellor?

“Rooting out excessive costs in every corner of the economy is an essential step to lower the cost of living for good, as well as promoting more dynamic markets for business,” the prime minister will say.

He will confirm reforms to the building of nuclear power plants, after the government’s nuclear regulatory taskforce found that “pointless gold-plating, unnecessary red-tape and well-intentioned, but fundamentally misguided environmental regulation had made Britain the most expensive place to build nuclear power”.

“We urgently need to correct this,” the prime minister will say.

Business secretary Peter Kyle will be tasked with applying the same deregulatory approach to major infrastructure schemes and to accelerate the implementation of Labour’s industrial strategy.

In response, Tory shadow chancellor Sir Mel Stride said: “It is frankly laughable to hear the prime minister say Rachel Reeves’s Benefits Street budget has put the country on the right course and that he wants to fix the welfare system.

“His chancellor has just hiked taxes by £26bn to pay for a welfare splurge, penalising people who work hard and making them pay for those who don’t work at all. And she misrepresented why she was doing it, claiming there was a fiscal black hole to fill that she knew didn’t exist.

“Labour’s leadership have repeatedly shown they lack the backbone to tackle welfare and instead are just acting to placate their left-wing backbenchers.”

Rachel Reeves tells Sky News she did not lie about the state of the public finances

Chancellor accused of ‘lying’

Sir Mel is referring to the chancellor’s speech on 4 November in which she laid the ground for tax rises due to the decision by the independent Office for Budget Responsibility (OBR) to review and downgrade productivity over recent years, at a cost of £16bn, which led to a black hole in the public finances.

But the OBR revealed on Friday that it had told the Treasury days earlier that there was actually a budget surplus of £4.2bn, leading to outrage and claims that she misled the country about the state of the public finances.

Rachel Reeves was asked directly by Sky’s Trevor Phillips if she lied, and she replied: “Of course I didn’t.”

Why did Reeves make the situation sound ‘so bleak’?

She said: “I said in that speech that I wanted to achieve three things in the budget – tackling the cost of living, which is why I took £150 off of energy bills and froze prescription charges and rail fares.

“I wanted to continue to cut NHS waiting lists, which is why I protected NHS spending. And I wanted to bring the debt and the borrowing down, which is one of the reasons why I increased the headroom.

“£4bn of headroom would not have been enough, and it would not give the Bank of England space to continue to cut interest rates.”

Ms Reeves also said: “In the context of a downgrade in our productivity, which cost £16bn, I needed to increase taxes, and I was honest and frank about that in the speech that I gave at the beginning of November.”

Badenoch says Rachel Reeves should resign

But Tory leader Kemi Badenoch said: “I think the chancellor has been doing a terrible job. She’s made a mess of the economy, and […] she has told lies. This is a woman who, in my view, should be resigning.”

Report due on OBR breach

The tumultuous run-up to the 26 November budget culminated in the OBR accidentally publishing its assessment of the chancellor’s measures 45 minutes before the speech began, in what was an unprecedented breach of budget security.

👉 Listen to Sky News Daily on your podcast app 👈

The chair of the OBR, Richard Hughes, apologised for the “error”, and announced an investigation into how it happened.

The chancellor has said that she retains confidence in him, despite the “serious breach of protocol”, and confirmed to Trevor that the investigation report will be delivered to her on Monday, although it is not clear when it will be published.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024