Having sealed her chancellor’s fate, the markets could seal the prime minister’s fate

So farewell, then, Trussonomics.

The demise of the country’s second shortest-lived chancellor also brings with it the demise of the country’s shortest-lived economic movement.

Liz Truss came into office promising to boost the country’s growth rate through a forensic combination of tax cuts, reforms to the country’s supply side (for which read: things like planning reform) and spending restraint. This was, if you squint a little bit, not dissimilar to the kinds of policies espoused by Ronald Reagan and Margaret Thatcher.

Tory MPs turn on Truss as PM scrambles to save job after sacking chancellor – latest updates

It always looked risky – especially at such a fragile point for the global economy. We are coming to the end of a 12-year period of cheap money, something which is causing a near-nervous breakdown in financial markets. Central banks are in the process of raising interest rates and trying to feed the glut of bonds they bought during the financial crisis back in the market.

As if that weren’t enough, Europe is facing one of its bleakest economic winters in modern memory, with a war raging in Ukraine and energy prices touching historic highs. It is hard to think of many less auspicious periods to attempt an untested new economic manifesto.

Yet Ms Truss and her former chancellor Kwasi Kwarteng pushed on all the same. And unlike Thatcher, whose first few budgets were grisly austerity packages which no one much enjoyed, Ms Truss and Mr Kwarteng aimed to turn Thatcherism on its head. Instead of fixing the public finances first and then cutting taxes second, they opted to spend the fruits of economic growth before that growth had even been achieved.

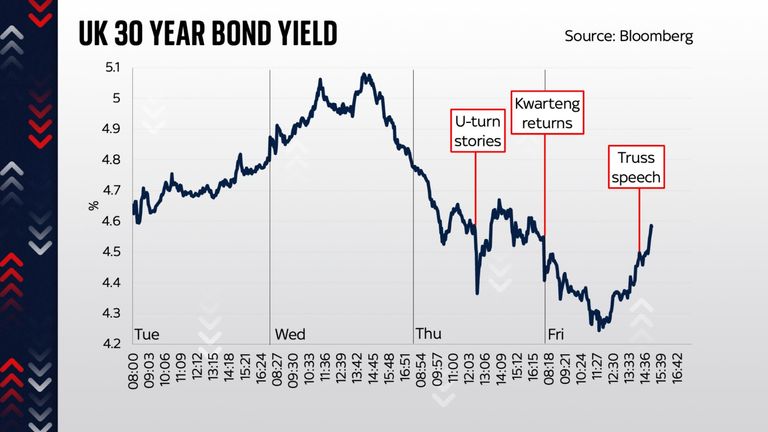

The mini-budget of 23 September was a small document with extraordinarily large consequences. Ironically, the more expensive the measures were, the less controversial they turned out to be. The scheme to cap household energy unit costs will potentially cost hundreds of billions of pounds, yet (and we know this because it was pre-announced long before the mini-budget) investors barely batted an eyelid. They carried on lending to this country at more or less the same or equivalent rates.

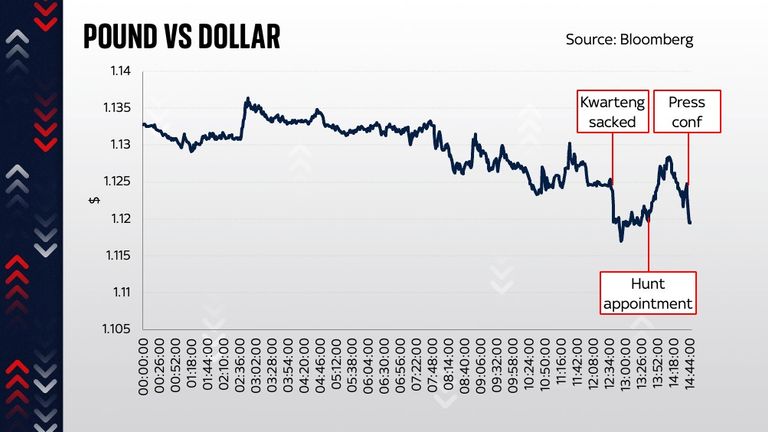

The same was not the case for the rest of the mini-budget’s policies. Shortly after they were announced – everything from the abolition of the 45p rate (actually quite cheap in fiscal terms) to the cancellation of Rishi Sunak’s corporation tax rise – markets began to lurch in what was, for Ms Truss, and most UK households, the wrong direction. The pound sank, the yields on government debt, which determine the interest rates across most of the economy, began to climb.

That was bad enough. When Mr Kwarteng announced gleefully a couple of days later on television that he had more tax cuts up his sleeve, the trot out of the country became a stampede. The pound fell, briefly, to the lowest level against the dollar in the history of, well, the dollar.

Even more worryingly, those interest rates on government bonds rose at an unprecedented rate, causing all sorts of malfunctions throughout the money markets.

The most obvious – and the one that perhaps will have the longest legacy – is the rise in mortgage rates. But the unexpected consequences were even more worrying, among them a crisis in funds used by pension schemes. That sparked a “run dynamic” which compelled the Bank of England to step in with an emergency support scheme.

Even at this point, we were into unprecedented territory. Never before had the Bank been forced to intervene quite like this. Never before had it had to do so as a result of a government’s Budget.

The intervention, however, had some success, bringing down the relevant interest rates and bringing markets back from the edge. But there was a sting in the tail: a deadline. Today, 14 October.

Analysis: PM’s new tax U-turn

In hindsight perhaps it’s obvious that this, then, would always have been the day when the government might face another existential crisis. Investors were always going to be nervous ahead of the Bank’s withdrawal from this neck of the bond market. And that is precisely what happened: after the governor reiterated, on a panel in Washington, that he was indeed serious, all eyes then turned to the chancellor. Could he say something to reassure markets?

In the event, the answer was: no. But something else changed matters: growing rumours of a U-turn. That brings us to this morning. The chancellor, pulled back from Washington early, was dismissed. The U-turn began. The corporation tax freeze is to be abandoned. The coming medium-term fiscal plan will involve austerity and a big dose of fiscal pain. The upshot is that Trussonomics, which was hinged clearly on tax cuts like these, is dead in the water.

However, the bigger question concerns what happens next. Those markets, which Ms Truss said explicitly were the reason for her U-turn, are still pretty frantic. No one knows how they’ll fare on Monday, but, whether right or wrong, another grisly day will almost certainly be seen as a sign of the government’s failure. And, having sealed the fate of her chancellor, the markets could well seal the fate of the prime minister.

But that’s a few days away – a long time in both politics and markets.

Liz Truss appoints Jeremy Hunt as chancellor. Pic: Andrew Parsons / No 10 Downing Street

In the meantime, here is something to dwell on: an alternative version of history. In a parallel universe, Ms Truss and Mr Kwarteng did things slightly less hastily. They decided their emergency Budget would simply deal with the energy price shock coming this winter. They promised an OBR statement and hatched plans for a growth-generating budget in a few months’ time.

In that parallel universe, interest rates probably wouldn’t have risen so high. The rises would, anyway, have been blamed on the Bank of England, not the government. The government would have enjoyed some kudos for having prevented energy-related penury this winter and made merry in their honeymoon. Things could have been oh-so different.

Click to subscribe to the Sky News Daily wherever you get your podcasts

Now, all of this is of course imponderable. But it does rather underline an important point: none of this was inevitable. This wasn’t a crisis like 1992 – where the UK faced monetary pressures suffered by nearly every other nation in Europe. It was simply a succession of very unfortunate decisions at precisely the wrong moment.

At a time of market turmoil and war in Europe, Ms Truss and Mr Kwarteng chose to take a gamble. It did not pay off.

To register your interest and share your story, please email TheGreatDebate@sky.uk

World

Colombia is high on Trump’s troublemaker list – but coca farmers will keep producing to match US demand

“Listen man, we’re a narco state, it’s just how it is, if you want to see drug deals, I’ll show you drug deals – it’s Colombia.”

I’d only asked one of our Colombian producers in passing if it was possible to see drugs being traded on the streets of Medellin. I didn’t realise it was that simple.

Medellin is synonymous with drugs and cartels. The home of perhaps the most famous of all the drug lords, Pablo Escobar, it seems to revel in its notoriety.

There are pictures of Escobar everywhere, on posters, on caps, and on t-shirts. There are even guided tours to his grave, and a museum in his honour.

Stuart Ramsay speaks with a coca farmer, who earn very little from growing the crop

This is where the big business drug cartels were born, invented by Escobar himself, the original Latin American “Godfather”.

In an infamous district in Medellin, we were instantly confronted with the sounds of dealers on the streets shouting out their products for sale as we drove through.

“Cocaine! Pills! Ecstasy! Tusi!” they shouted. All available to a traffic jam of cars waiting to buy.

Motorcycle delivery drivers queued to make the pick-up for their clients waiting in high-end apartments and nightclubs elsewhere in the city, while buyers on foot discreetly scored their drugs, before moving on.

Medellin was the home of Pablo Escobar and drugs are widely traded on its streets

‘Narco’ culture

It was chaotic and noisy, a place where lookouts use whistles to send signals to the dealers.

Two toots mean it’s all clear, a single toot is a warning – it means the police are nearby.

In the middle of this big open-air market for drugs, dimly lit restaurants and cafes served dinner. We passed one café where we saw a family sat at a table outside, celebrating a woman’s 70th birthday.

This neighbourhood runs a 24-hour drug selling market alongside the usual shops and cafes that spill over on to the pavement.

It is not illegal to grow coca, only to use it to produce cocaine

Although Colombia has a long history and fascination with “narco” culture and drug-taking, its immediate problem is that President Donald Trump has launched a war on Latin American drug cartels, manufacturers, and the nations the drugs come from – and through.

Venezuela is at the top of his hit list; he has launched strikes on boats off the Venezuelan coast that he says were carrying drugs. He has boosted American military presence in the Caribbean – sending ships, marines, helicopters, drones and jets into the region.

There is speculation he may be looking for regime change in Venezuela, and that the war on drugs is a front to remove President Nicolas Maduro from power, claiming the Venezuelan government is basically a drug cartel. Something they of course deny.

This coca plantation was hacked into the rainforest on the border of Colombia and Peru

None of this bodes well for Venezuela’s neighbour Colombia, indeed President Trump has made it clear Colombia is high on his list of troublesome nations.

Read more:

Trump’s declared war on drug cartels – Ecuador is taking action

Greta Thunberg removed from Gaza aid flotilla after ‘attack’ by Israel

There are other countries on his list, like Mexico, that he says has demonstrated willingness to clean up their act and take the war to Mexico’s deadly cartels.

Mr Trump’s gripe with Colombia isn’t necessarily that its society has a relaxed attitude to drug use – it is widespread across all classes – no, his problem is that Colombia is one of the biggest producers of cocaine in the world, and it feeds the biggest market, which is the United States of America.

Coca plantations are hidden miles away from other people in the Amazon

Hidden away, miles from people

It seems that the president’s view is that the supplier is the problem, not necessarily the user.

Cocaine is extracted from the coca leaf, which is grown in abundance in Colombia, Peru, and Bolivia.

Growing the coca plant in these countries is not illegal, and the leaf itself is often used for other purposes. The plant only becomes illegal when it’s used for cocaine production.

I wanted to meet the farmers who grow coca to find out if they are the masterminds of a multi-billion-pound international drugs business, or just farmers meeting international demand.

My journey began just after dawn in pouring rain on the Amazon River in Colombia.

Perhaps unsurprisingly the plantations are hidden away in remote areas, miles away from people.

Stuart Ramsay in the rainforest

We travelled for hours in the rain, on a small boat with a guide, passing indigenous communities who have nothing to do with the business hiding in their forest.

The river narrowed as we got closer to our destination, and five hours later, after navigating through broken tree trunks and low hanging branches, we arrived at an eight hectare coca plantation hacked into the rainforest bordering Colombia and Peru.

The crop, which is two-and-a-half years old, is hidden by the trees and the river.

They are about to start harvesting it, but it’s incredible just how many leaves they need.

The farmer says that for every 70 grams of cocaine produced, the cartel producers need 30 kilograms of leaves.

Colombia is one of the biggest producers of cocaine

Only way to provide for his family

That’s a lot of picking – and the farmer will earn just $7 for those 30 kilograms of leaves.

The cocaine business might be incredibly lucrative for the cartels that control it, but at the very bottom the farmers hardly get paid a thing.

And though he is worried about getting caught, the farmer I meet sees it as the only way to provide for his family.

“For me it’s very valuable, it’s my sustenance, the way for sustaining life,” he told me.

“We are aware that illegal processing isn’t good for anybody, not exactly, you can’t say I am doing this, and this is good for people, no, this harms the entire community, everyone,” he explained when I asked him if he was at all conflicted about his crop.

“But we all make sacrifices, and we struggle to make our way in life.”

It’s hard to believe that the global business of manufacturing and shipping cocaine around the world all starts with these fairly innocuous looking coca leaves.

And whatever Donald Trump says, they will keep producing as long as users in America, Europe, and indeed the world, demand it.

Several boats from a large aid flotilla trying to reach Gaza have been boarded by Israeli authorities – with campaigner Greta Thunberg among those removed.

The Global Sumud Flotilla is made up of more than 40 civilian boats with an estimated 500 people onboard, and is trying to break Israel’s sea blockade.

But the attempt appears to have been thwarted – at least for now – by about 20 Israeli ships.

Israel’s foreign ministry said “several vessels” had been “safely stopped” with passengers being taken to an Israeli port.

“Greta and her friends are safe and healthy,” a spokesperson added.

A livestream showed some of the boats in the flotilla as the incident unfolded

A video showed Thunberg sitting on deck while being handed a water bottle and raincoat.

It’s so far unclear how many boats have been intercepted.

The flotilla ignored requests to turn back and organisers said the interception was illegal as it happened in “international waters” around 80 miles off the coast.

Greg Stoker, a US veteran who’s involved, said water cannon had been used on some of the boats.

Gaza-bound flotilla ‘aggressively circled’ by warship

The flotilla, which set off from Barcelona and scheduled to arrive this morning, was flanked by NATO warships for some of the journey.

The attempt has received a lot of attention, with Nelson Mandela’s grandson, a former Barcelona mayor and several European legislators taking part.

Israel said the mission was violating a lawful blockade and is only intended to provoke. It also said it had offered a way to deliver any aid peacefully through safe channels.

Organisers said the night-time interception was the second time the flotilla had been approached on Wednesday, after “warships” earlier encircled two of its boats.

The flotilla set off from Barcelona on 31 August and later stopped in Sicily

Last week, drones also reportedly dropped stun grenades and itching powder on some vessels.

Israel didn’t comment, but has said it will use any means to stop the boats getting to Gaza.

Protests have broken out in Italy and Turkey over the treatment of the flotilla.

Italy’s largest union has called a general strike tomorrow, saying the “attack on civilian vessels carrying Italian citizens represents an extremely serious matter”.

Turkey’s foreign ministry called Israel’s interception an “attack” and “an act of terror” that endangered lives of those on board.

Gaza has been dealing with severe food shortages due to the ongoing war.

Thunberg and activist Saif Abukeshek. Pic: Reuters/Nacho Doce

Agencies such as the UN accused Israel of deliberately slowing the delivery of supplies – something it denies.

However, the aid being carried by the flotilla is said to only be a symbolic amount of food and medicine.

An aid boat carrying Thunberg was also intercepted near Gaza in June, with the Swede deported alongside others.

Israel put in it sea blockade when Hamas took control of the territory in 2007 and there have been several attempts to break it since then.

Some of those involved in the latest campaign have said they will start a hunger strike if they’re detained.

Read more:

Hamas’s first reaction to peace plan is telling

What Sky correspondents make of Trump plan

Will Trump’s Gaza plan bring peace?

Meanwhile, all eyes remain on Hamas and whether it will accept Donald Trump’s peace plan to end the two-year war, sparked by the group’s terror attack on Israel.

The 20-point proposal was unveiled alongside Israeli Prime Minister Benjamin Netanyahu in the White House this week.

Hamas said it would study the plan and consult with other factions, but didn’t give an indication of when it would deliver its verdict.

Mr Trump said on Tuesday he would give the group “three or four days”.

World

Taliban internet blackout has created an extreme scenario in Afghanistan with far-reaching consequences

At Kabul International Airport, there are dozens of confused looking families.

Many are holding flowers, waiting and hoping their loved ones will touch down.

Others came here hoping to take-off but are now sitting bewildered in the hot sun.

After the Taliban imposed a nationwide shutdown of the internet, no one knows if any flights are still operating and no one can use their phones to find out.

The Taliban caught many in the country off-guard with their shutdown. File pic: West Asia News Agency via Reuters

“I am waiting for my brother from Australia,” one man tells me, “but I don’t know if he’s coming”.

Beyond the gates, the runway is full of grounded planes.

After hours of waiting on Tuesday, no international flights took off or arrived at Kabul Airport, despite some airlines scheduling departures.

The Taliban caught many in the country off-guard with their shutdown – reportedly even some of their own ministers.

Initially, there appeared to be no official indication of how long the shutdown might last or an explanation for why it was imposed.

A man tries to use Google on his smartphone in the Afghan capital. Pic: Reuters

On Wednesday, the Taliban government rejected reports of a nationwide internet ban, saying old fibre optic cables are worn out and are being replaced.

But, at the airport, people worry it could be indefinite. Others speculate about rumours it’s to do with security protocols and the movement of officials in the country.

No one knows, and the TV and radio stations they get their news from have not been providing the latest information.

Men try to connect their smart TV to the internet. Pic: Reuters

The banks are open but no one can get out money. An employee at the bank in our hotel in Kabul told us they haven’t been able to open their operating systems since Tuesday morning and that Western Union isn’t accessible either.

That’s hugely significant in a country where many are reliant on money sent back by relatives abroad and banks are already struggling with sanctions.

No one can call the police, no one can call an ambulance, and hospitals and medical services are wrestling with how to adjust too.

It follows more than a week of temporary connectivity issues in some parts of the country, with the northern region of Balkh among the first to be affected by a ban on fibre optic internet.

Read more: Internet ban ‘extinguishing the only light that still reaches us’

Taliban fighters ride on a pickup truck during celebrations marking the fourth anniversary of the US withdrawal. Pic: AP

In the last 10 days, we have been travelling across Afghanistan. People in Nangarhar, Kunar, Mazar-i-Sharif and Herat all expressed concern about possible impending blackouts, and we personally experienced a slowdown in connectivity in these places. But nothing as widespread or sustained as this shutdown which is nationwide.

Two weeks ago, the Taliban’s provincial government spokesman Haji Attaullah Zaid said leader Hibatullah Akhundzada had imposed a “complete ban” on cable internet access in Balkh.

“This measure was taken to prevent immorality, and an alternative will be built within the country for necessities,” Mr Zaid said.

It was said to be connected to concerns around pornography – but this was never officially stated by the Taliban.

We have tried to reach the government for comment via satellite phone but with no success.

No one knows how long the shutdown will last. Pic: Reuters

The blackout has disrupted phone services. In countries with limited telecom infrastructure, phone networks are often routed through fibre-optic systems which have now been disabled.

The lack of connectivity has raised immediate concern in the aid community. Amnesty International called it “reckless” and said the shutdown would have “far-reaching consequences for the delivery of aid, access to healthcare and girls’ education”.

After the Taliban banned school for girls over the age of 12, many in the country have been secretly studying online.

Read more from Sky News:

US government shuts down

Eurovision rebellion emergency vote

Listen to The World with Richard Engel and Yalda Hakim every Wednesday

Everyone we’ve spoken to seems dumbfounded.

During the previous temporary blackouts, the Taliban did warn more was to come. But no one appears to have anticipated this – not ordinary citizens, not foreign officials here in Kabul, not big business, not the airlines or the hospitals.

It is an indication of how quickly this country can turn and the power the Taliban has to disrupt and reshape its future.

Internationally, many are raising concerns that this is an attempt by the Taliban at widespread censorship and further restriction of girls’ education.

Whatever the intention of their move, it has created an extreme scenario: no one in this country can currently contact anyone – for an emergency, for a family member, or for guidance – creating a major information vacuum.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment12 months ago

Environment12 months agoHere are the best electric bikes you can buy at every price level in October 2024