Why is Rishi Sunak casting such a sombre mood? It’s more about politics than economics

Rishi Sunak says we are facing a “profound economic crisis”. Big words, not to mention depressing. But do they really stack up?

Is the UK really facing something unique? Can he really blame much of it (as was implicit in his speech) on his predecessor? Or is something else going on?

Let’s start at the start.

There is no doubt that the UK is facing tough economic times right now. We are quite plausibly in the teeth of a recession. Look at measures like the purchasing manager’s index from S&P Global – a measure of how businesses are faring right now – and it is contraction territory. This is a recession warning, and no mistake.

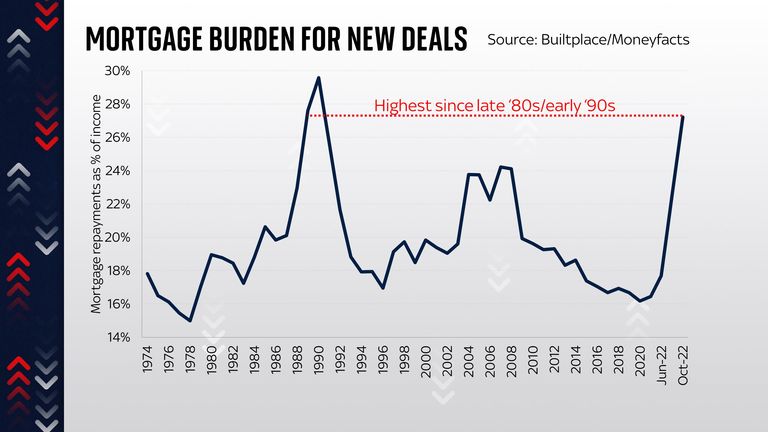

And there are certainly some factors which will make this a grim year or two for households. For one thing, mortgage costs are rising, and rising fast. The average two-year fixed rate mortgage is currently up above 6%, a level which implies the highest repayments as a percentage of household incomes since the late 1980s or early 1990s. This is clearly not good news.

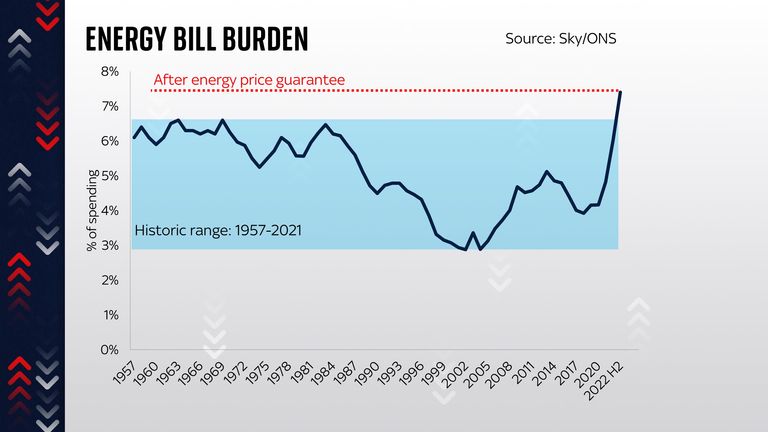

And it’s a similar story for energy bills. Even after you account for the energy price guarantee introduced by Liz Truss, the amount the average household spends on energy this winter will still be the highest we’ve seen since at least the 1950s. Again, not good news – and note that since the scheme has been shortened from two years to six months, it’s quite plausible the costs are even greater next year.

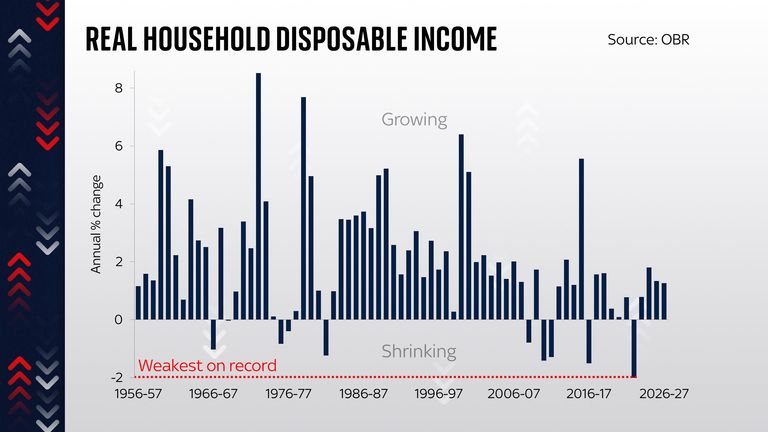

Put it all together and any measure of our collective standard of living suggests an astonishing fall this year. We are all going to be much poorer, relative to what we typically want to spend our money on. And that, in large part, is down to the impact of higher energy prices, which creep into every part of our lives.

But these are not the only issues facing the government.

The UK is not the only major economy facing a potential recession

One problem which no previous prime minister has been able to address successfully is Britain’s productivity malaise. Output per hour is perhaps the single most important yardstick of our economic wellbeing and it has essentially flatlined since the financial crisis, making (and this is not an exaggeration) everything worse: our incomes, our quality of life, the level of taxes and national debt.

And this is before you consider the deeper issues facing the global economy right now. Most glaringly we seem to be in the early stages of a new Cold War, which could result in the creation of trading blocs rather than a fully globalised world. And this prognosis is, frankly, more optimistic than many. This will have enormous economic implications.

But here’s the thing. None of these challenges are necessarily Britain’s alone. The UK is not the only major economy facing a potential recession: others in Europe will probably have even deeper contractions this winter. Disappointing productivity is something many developed economies struggle with. Interest rates are rising everywhere (even if the UK’s recent increase in borrowing costs outpaced other nations).

Many of the current problems pre-date Liz Truss

Nor is it especially fair to blame all these problems on Liz Truss: they pretty much all pre-date her. And here’s the really interesting thing: the spike in government bond yields which followed her and Kwasi Kwarteng’s mini-budget has now been almost completely erased.

Those gilt yields are now nearly back to where they were before. So too are expectations for Bank of England interest rates next year. This is an extraordinary turnaround – a consequence of the fact that the Truss government is no more.

But it means that actually much of the damage has now been erased. It’s worth pondering this for a moment. Remember: that rise in gilt yields as international investors looked askance at the UK pushed up the potential cost of borrowing both for households and for governments. It meant that if the government carried on having to issue debt at those kinds of interest rates then its debt interest bill would have been a lot higher. The IFS calculated the ongoing cost at about £10 billion a year. That’s a big deal.

‘Credibility premium’ on government debt is shrinking

But now that the “credibility premium” on government debt is shrinking, that problem is no longer, well, a problem. It may soon have disappeared altogether.

Which raises a question: why did Rishi Sunak try to cast such a sombre mood on the steps of Downing Street? My suspicion is that it’s about 60% politics and about 40% economics.

The politics first: if he can convince the public (and his MPs) that things are grim, it means less resistance for the inevitable cuts. Much as Covid united the party, perhaps, he thinks, the threat of economic contagion could do something similar.

If he can persuade the public that the bad news he’s meting out is down to Liz Truss rather than his own policies as chancellor (most of these problems were problems when he was in Downing Street and had responsibility for doing something about them) then, well, that would obviously suit him. Even if it’s not entirely accurate.

Sunak’s warnings are only 40% economics

The 40% economics is intriguing, because there’s a virtuous circle here. If he can deploy phrases like “profound economic crisis” and “difficult decisions” he can persuade markets that he’s really serious about cutting debt, which in turn should push down gilt yields even lower. Which means the hole in the public finances suddenly gets smaller too.

Talking tough could actually mean he doesn’t have to act quite so tough in the coming austerity mini-budget or whatever we’ll call it.

Not that much of this will be detectable when the fiscal statement lands. We are clearly in for some tough cuts for the economy. But most of the challenges they are intended to address were baked in long before Liz Truss ever reached Downing Street.

Baroness Michelle Mone has broadened her attack on her political critics, accusing Conservative leader Kemi Badenoch of using “inflammatory” and “reckless” language that could prejudice a police investigation into her role in the awarding of PPE contracts.

A day after she wrote to Sir Keir Starmer, accusing the government of pursuing a vendetta against her, the former Conservative peer responded to comments by Ms Badenoch following a High Court ruling that a company linked to Baroness Mone’s husband must repay £122m received for surgical gowns.

The court found that PPE Medpro, founded by her husband Doug Barrowman, was in breach of contract with the Department of Health and gave it two weeks to repay the sum.

While not a director of the company, Baroness Mone used her political contacts to introduce PPE Medpro to the government’s “VIP fast-lane” at the start of the pandemic, and a family trust of which her children are beneficiaries received £29m of the profits.

A separate criminal investigation by the National Crime Agency (NCA) is ongoing, and assets linked to the couple worth £75m have been frozen while it continues.

In a series of radio interviews, Ms Badenoch criticised Baroness Mone, accusing her of bringing shame on the Conservative Party and calling for her to step down from the House of Lords.

“Where people do wrong, they should be punished,” she said. “They should face the full force of the law and this is something that I very strongly believe in,” she said.

“And as the prosecution against her continues, they should throw the book at her for every single bit of wrongdoing that has taken place.”

Baroness Mone ‘should resign’

In a letter from her private office, Baroness Mone accuses the Tory leader of being ignorant of the facts and calls out a series of other Conservative politicians who introduced companies to the VIP lane.

“I was shocked to the core to read about your inflammatory language on BBC Radio yesterday calling for me to resign from the House of Lords,” she writes.

“You are commenting on a live criminal investigation that could prejudice the outcome of any trial, and in so doing, you are reportable to the attorney general for breach of and contempt of court. Does no one ever tell you these things before you and your colleagues make reckless statements in the public domain?”

Read more from Sky News:

Customer details stolen in Renault cyber attack

Japan could run out of Asahi

Tinned tuna-owner to unveil £1.5bn float

Baroness Mone goes on to say the NCA investigation has “nothing to do with PPE Medpro and the contracts”.

“The case theory of the NCA investigation is that I somehow misled the Conservative government about my alleged concealed involvement and ended up pocketing a lot of money,” she writes. “Well I’m sorry to disappoint you, but it isn’t true.”

She also says the Conservative government knew of her involvement and names former health secretary Matt Hancock, Lord Agnew, Lord Feldman and Lord Chadlington as being among 51 “mostly Conservative peers and MPs” who introduced providers to the VIP lane.

“So Kemi, my role was exactly the same as all other Conservative MPs and peers who were trying to help provide PPE… if I have done wrong, then so have all the others in the VIP lane. In which case, you should be calling out for them to resign as well. That’s if you manage to work out what it is they are supposed to have done wrong.”

The High Court says a company linked to Mone breached a government contract of nearly £122m

She concludes by saying she has no wish to rejoin the Lords as a Conservative peer when her leave of absence ends, “that’s assuming there still is a Conservative Party before the next General Election”.

The letter comes as an online petition calling for Baroness Mone to step down from the Lords, launched by the Covid-19 Bereaved Families for Justice, attracted 60,000 signatures in 24 hours.

The Conservative Party has been approached for comment.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment12 months ago

Environment12 months agoHere are the best electric bikes you can buy at every price level in October 2024