Coterra Energy’s earnings beat, dividend raise reinforce the Club’s investment case

OpenAI and Advanced Micro Devices have reached a deal that could see Sam Altman‘s company take a 10% stake in the chipmaker.

AMD stock skyrocketed more than 25% on Monday during premarket trading following the news.

OpenAI will deploy 6 gigawatts of AMD’s Instinct graphics processing units over multiple years and across multiple generations of hardware, the companies said Monday. It will kick off with an initial 1-gigawatt rollout of chips in the second half of 2026.

Tune in at 9:30 a.m. ET as OpenAI President Greg Brockman and AMD CEO Lisa Su join CNBC TV to discuss the chip deal. Watch in real time on CNBC+ or the CNBC Pro stream.

As part of the tie-up, AMD has issued OpenAI a warrant for up to 160 million shares of AMD common stock, with vesting milestones tied to both deployment volume and AMD’s share price.

The first tranche vests with the first full gigawatt deployment, with additional tranches unlocking as OpenAI scales to 6 gigawatts and meets key technical and commercial milestones required for large-scale rollout.

If OpenAI exercises the full warrant, it could acquire approximately 10% ownership in AMD, based on the current number of shares outstanding.

The ChatGPT maker said the deal was worth billions, but declined to disclose a specific dollar amount.

AMD one-day stock chart.

“AMD’s leadership in high-performance chips will enable us to accelerate progress and bring the benefits of advanced AI to everyone faster,” Altman said in a release announcing the partnership.

The deal positions AMD as a core strategic partner to OpenAI, marking one of the largest GPU deployment agreements in the artificial intelligence industry to date.

The partnership could help ease industrywide pressure on supply chains and reduce OpenAI’s reliance on a single vendor.

OpenAI unveiled a landmark $100 billion equity-and-supply agreement with Nvidia nearly two weeks ago, cementing the chip giant’s role in powering the next generation of OpenAI models. That arrangement combined capital investment with long-term hardware supply — though in Nvidia’s case, it was the chipmaker taking an ownership stake in OpenAI.

Shares of Nvidia fell 1% on Monday in premarket trading following news of the OpenAI-AMD deal.

That deal accounts for a dedicated 10-gigawatt portion of OpenAI’s broader 23-gigawatt infrastructure road map. At an estimated $50 billion in construction costs per gigawatt — together with the AMD deal — OpenAI has committed roughly $1 trillion in new buildout spending in just the past two weeks.

OpenAI is also in talks with Broadcom to build custom chips for its next generation of models.

The arrangement between OpenAI and AMD adds a new layer to the increasingly circular nature of AI’s corporate economy, where capital, equity and compute are traded among the same handful of companies building and powering the technology.

Nvidia is supplying the capital to buy its chips. Oracle is helping build the sites. AMD and Broadcom are stepping in as suppliers. OpenAI is anchoring the demand.

It’s a tightly wound circular economy, and one that analysts fear could face real strain if any link in the chain starts to weaken.

For AMD, the partnership is both a commercial milestone and a validation of its next-generation Instinct road map.

After years of trailing Nvidia in the AI accelerator market, AMD now has a flagship customer at the forefront of the generative AI boom.

AMD CEO Lisa Su said it creates “a true win-win enabling the world’s most ambitious AI buildout and advancing the entire AI ecosystem.”

It also reinforces OpenAI’s broader infrastructure ambitions.

Through its Stargate project, Altman’s startup is rapidly transforming into one of the most aggressive infrastructure builders in the AI sector. Its first site in Abilene, Texas, is already operational and running Nvidia chips, with construction continuing to expand capacity.

Upcoming builds in New Mexico, Ohio and the Midwest are expected to feature a mix of suppliers, including AMD.

WATCH: OpenAI’s Sarah Friar says ‘full ecosystem’ needs to come together to address compute crunch

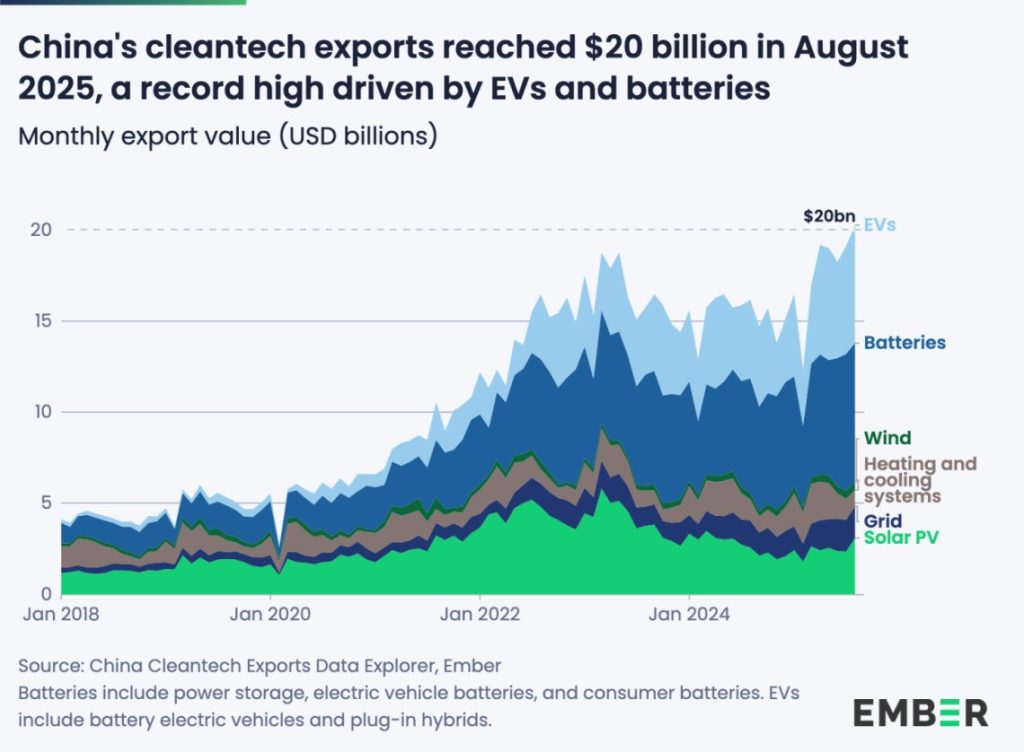

China set a new record for clean tech exports in August 2025, hitting $20 billion, according to new data analyzed using Ember’s China Cleantech Exports Data Explorer. The country remains the world’s largest exporter of electrotech, with surging demand for EVs and batteries leading the charge.

EV exports jumped 26% from January through August compared to the same period in 2024, while battery exports rose 23%. Other sectors saw more modest growth – grid technology up 22%, wind up 16%, and heating and cooling systems up 4% – but those gains were offset by a 19% drop in solar PV export value. EVs and batteries are now worth more than double the value of China’s solar PV exports.

This milestone is remarkable because it comes even as technology prices have fallen sharply. Solar panel prices, for example, have plunged more than 80% over the past decade, making them more affordable and driving up global demand. In August alone, China exported 46 gigawatts (GW) of solar PV – more than Australia’s entire installed solar capacity – setting a record in capacity terms. However, their dollar value remains 47% below their March 2023 peak.

Falling prices have fueled growth in new regions. Over half of the increase in China’s EV exports this year came from outside the OECD, with the ASEAN region emerging as a major growth engine. EV exports to ASEAN surged 75% in the first eight months of 2025, mainly driven by Indonesia. The country saw the biggest rise in Chinese EV imports globally this year, becoming the world’s ninth-largest EV market. Battery electric vehicles made up 14% of new car sales in Indonesia in August 2025, up from 9% a year earlier.

Africa is also rapidly adopting Chinese clean tech. From January to August, EV exports to the continent nearly tripled year-over-year (+287%), albeit from a very low base, with Morocco leading growth and Nigeria’s imports soaring sixfold. Latin America and the Caribbean saw an 11% rise, while the Middle East climbed 72%.

Domestically, China’s own adoption of clean tech is accelerating even faster. EVs accounted for 52% of new car sales in August, and in the first half of 2025, China installed more than twice as many solar panels as the rest of the world combined. Ember’s recent China Energy Transition Review attributes this momentum to consistent policy support that’s reshaping the country’s economy and energy system around electrified technologies.

“Demand for clean technologies continues to skyrocket as more and more countries seek their benefits, from low-cost power to cheaper vehicles,” said Ember analyst Euan Graham. “China’s electrotech is becoming the basis of the new energy system, with continued cost reductions driving faster growth than ever, especially in emerging economies.”

Read more: The era of cheap Chinese solar + storage is ending – here’s why

The 30% federal solar tax credit is ending this year. If you’ve ever considered going solar, now’s the time to act. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

Environment

This Meta alum has spent 10 months leading OpenAI’s nationwide hunt for its Stargate data centers

Keith Heyde stands on site in Abilene, Texas, where OpenAI’s Stargate infrastructure buildout is underway. Heyde, a former head of AI compute at Meta, is now leading OpenAI’s physical expansion push.

OpenAI

It wasn’t how Keith Heyde envisioned celebrating the holidays. Rather than hanging out with his wife back home in Oregon, Heyde spent late December visiting potential data center sites across the U.S.

Two months earlier, Heyde left Meta to join OpenAI as the head of infrastructure. His job was to turn CEO Sam Altman’s ambitious compute dreams into reality, seeking out vast swaths of land suitable for expansive facilities that will eventually be packed with powerful graphics processing units for building large language models.

“My in-between Christmas and New Year’s last year was actually mostly spent looking at sites,” Heyde, 36, told CNBC in an interview. “So my family loved that, trust me.”

His life in 2025 has only gotten more intense.

Since January, OpenAI has been quietly soliciting and reviewing proposals from around 800 applicants hoping to host the next wave of its Stargate data centers, AI supercomputing hubs designed to train increasingly powerful models.

Roughly 20 sites are now in advanced stages of diligence, with massive tracts of land under review across the Southwest, Midwest and Southeast. Heyde said tax incentives are “a relatively small part of the decision matrix.”

The most important factors are access to power, ability to scale, and buy-in from local communities.

“Can we build quickly, is the power ramp there fast, and is this something where it makes sense from a community perspective?” he said.

Heyde leads site development within OpenAI’s industrial compute team, a division that’s swiftly become one of the most important groups inside the company. Infrastructure, once a supporting function, has now been elevated to a strategic pillar on par with product and model development.

With traditional data centers nearly at max capacity, OpenAI is betting that owning the next generation of physical infrastructure is central to controlling the future of AI.

The energy needs are hard to fathom. A gigawatt data center requires the amount of power needed for some entire cities. Late last month, OpenAI announced plans for a 17-gigawatt buildout in partnership with Oracle, Nvidia, and SoftBank.

New sites will have to include all sorts of energy options, including battery-backed solar installations, legacy gas turbine refurbishments and even small modular nuclear reactors, Heyde said. Each site looks different, but together they form the industrial backbone OpenAI needs to scale.

“We’ve done this wonderful piece of bottleneck analysis to see what types of energy sources actually allow us to unlock the journey that we want to be on,” Heyde said.

A good chunk of the capital is coming from Nvidia. The chipmaker agreed to invest up to $100 billion to fuel OpenAI’s expansion, which will involve purchasing millions of Nvidia’s GPUs.

‘Perfect wasn’t the goal’

Heyde, a former head of AI compute at Meta, helped oversee the buildout of Meta’s first 100,000 GPU cluster.

In addition to power, OpenAI is assessing how quickly it can build on a site, the availability of labor and proximity to supportive local governments, according to Stargate’s request for proposal.

Heyde said the team has made around 100 site visits and has a short list of sites in late-stage review. Some will be brand new builds, and others will require conversions and refurbishments of existing facilities. Flexibility will be key.

“The perfect parcels are largely taken,” Heyde said. “But we knew that perfect wasn’t the goal — the goal for us was, number one, a compelling power ramp.”

Competition is fierce.

Meta is building what may be the largest data center in the Western Hemisphere — a $10 billion project in Northeast Louisiana, fueled by billions in state incentives. CEO Mark Zuckerberg raised the top end of the company’s annual capital expenditure spending range to $72 billion in July.

The steel frame of data centers under construction during a tour of the OpenAI data center in Abilene, Texas, U.S., Sept. 23, 2025.

Shelby Tauber | Reuters

Amazon and Anthropic are teaming up on a 1,200-acre AI campus in Indiana. And across the country, states are rolling out tax breaks, power guarantees, and expedited zoning approvals to attract the next big AI cluster.

OpenAI is a relative upstart, having been around for just a decade and only known to the mainstream since launching ChatGPT less than three years ago. But it’s raised mounds of cash from the likes of Microsoft and SoftBank, in addition to Nvidia, on its way to a $500 billion valuation.

And OpenAI is showing it’s not afraid to lead the way in AI. A self-built solar campus in Abiliene, Texas, is already live.

While OpenAI still leans on partners like Oracle, OpenAI Chief Financial Officer Sarah Friar told CNBC last week in Abilene that owning first-party infrastructure provides a differentiated approach. It curbs vendor markups, safeguards key intellectual property, and follows the same strategic logic that once drove Amazon to build Amazon Web Services rather than rely on existing infrastructure.

However, Heyde indicated that there’s no real playbook when it comes to AI, particularly as companies pursue artificial general intelligence (AGI), or AI that can potentially meet or exceed human capabilities.

“It’s a very different order of magnitude when we think about the type of delivery that has to happen at those locations,” he said.

Some applicants, including former bitcoin mining operators, offered existing power infrastructure, like substations and modular buildouts, but Heyde said those don’t always fit.

“Sometimes we found that it’s almost nice to be the first interaction in a community,” he said. “It’s a very nice narrative that we’re bringing the data center and the infrastructure there on behalf of OpenAI.”

The 20 finalist sites represent phase one of a much larger buildout. OpenAI ultimately plans to scale from single-gigawatt projects to massive campuses.

“Any place or any site we’re moving forward with, we’ve really considered the viability and our own belief that we can deliver the power story and the infrastructure story associated with those sites,” Heyde said.

He understands why many people are skeptical.

“It’s hard. There’s no doubt about it,” Heyde said. “The numbers we’re talking about are very challenging, but it’s certainly possible.”

WATCH: OpenAI’s $850 billion buildout contends with grid limits

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024