Coterra Energy’s earnings beat, dividend raise reinforce the Club’s investment case

On today’s budget-conscious episode of Quick Charge, we’re building up to the reveal of a new, more affordable Tesla Model Y tomorrow that will almost definitely not be a cheap pile of misaligned plastic body parts with inconsistent panel gaps that’s utterly incapable of turning the tide on Tesla’s global decline.

Plus, we’ve got news that Tesla is in hot water with California over its alleged mishandling of its insurance business, revisit the lies told about Cybertrucks drag racing Teslas, and look at the incredible 110% increase in EV sales over at GM that’s driving Cadillac’s renaissance.

Today’s episode is brought to you by Climate XChange, a nonpartisan nonprofit working to help states pass effective, equitable climate policies. The nonprofit just kicked off its 10th annual EV raffle, where participants have multiple opportunities to win their dream model. Visit the site at CarbonRaffle.org/Electrek to learn more.

Source Links

Prefer listening to your podcasts? Audio-only versions of Quick Charge are now available on Apple Podcasts, Spotify, TuneIn, and our RSS feed for Overcast and other podcast players.

New episodes of Quick Charge are recorded, usually, Monday through Thursday (most weeks, anyway). We’ll be posting bonus audio content from time to time as well, so be sure to follow and subscribe so you don’t miss a minute of Electrek’s high-voltage daily news.

Got news? Let us know!

Drop us a line at tips@electrek.co. You can also rate us on Apple Podcasts and Spotify, or recommend us in Overcast to help more people discover the show.

If you’re considering going solar, it’s always a good idea to get quotes from a few installers. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

Waev Inc. has just unveiled the GEM eX, a new electric utility vehicle designed to bridge the gap between street-legal low-speed vehicles (LSVs) and true off-road work machines. The company calls it the most versatile electric work UTV yet.

Unlike most golf cart–based UTVs or high-speed recreational rigs, the GEM eX is purpose-built for commercial, industrial, and government fleets that need to move between city streets, job sites, and rough terrain, all while staying emissions-free.

The vehicle features a top speed of 25 mph (40 km/h) and is said to be DOT street-legal as an LSV on roads up to 35 mph (56 km/h), giving it a clear advantage over most off-road-only competitors.

Power is provided by a 6.5 kW motor in a rear-wheel drive setup with a limited-slip rear differential. An 8 kWh battery provides enough juice for a claimed maximum range of 85 miles (137 km).

The eX comes with several fleet-focused safety and utility upgrades, including 3-point seat belts, roof crush protection, backup camera, mirrors, pedestrian noise emitter, and a robust bumper system. It rolls on street, winter, or all-terrain tires, and the chassis features 9.5 inches (24 cm) of ground clearance, 6.5 inches (16.5 cm) of suspension travel, and a 50-degree approach angle for climbing curbs or crossing uneven work terrain.

Hill-hold assist and single-pedal descent control make it easy to handle on slopes, while a limited-slip differential helps maintain traction without chewing up turf.

In the back, a 1,250 lb (567 kg) composite dump box can fit a full-sized pallet and comes with gas-assist or electric lift options, while towing capacity matches that at 1,250 lb (567 kg). Optional hard doors, roll-down windows, and HVAC with heat and A/C turn it into a true all-weather workhorse.

The lithium iron phosphate battery pack is said to provide a long lifespan for extra durability in extreme climates from –20°F to 140°F (–29°C to 60°C). Charging is flexible via 120V, 240V, or J1772 public stations, and Waev backs the battery with a 7-year warranty – on par with many passenger EVs.

“We field-tested the GEM eX everywhere from Arizona deserts to Minnesota winters,” said Sven Etzelsberger, Waev’s Director of Engineering. “Every piece of customer feedback went back into this vehicle. The result is a work UTV that’s refined, reliable, and ready to go.”

The GEM platform has expanded significantly over the years, from its humble beginnings as a simple people mover to more recent adaptations into everything from ambulances and emergency vehicles to the new GEM eX electric UTV.

Priced at $24,955, the higher purchase price may be one of the few downsides to the quieter, cleaner, and easier to maintain alternative to traditional gasoline-powered UTVs.

Electrek’s Take

Waev’s new GEM eX seems to hit a sweet spot that’s been missing – a street-legal, electric work UTV tough enough for real jobs yet affordable and easy to maintain. For fleet managers juggling both paved and off-road environments, this could be a serious game-changer.

While the price is high, it comes in at significantly less than other well-known models like Polaris’ Zero-powered electric RANGER UTV.

At the same time, there are still more affordable options like those from KANDI that offer more power for a lower price. However, without GEM’s storied brand legacy and increased national support, cheaper options may not have the staying power to compete.

So sure, it’s expensive, but at least I’m glad to see more options coming to the market, especially from brands that have been around for years. Here’s to hoping for more affordable options in the future.

FTC: We use income earning auto affiliate links. More.

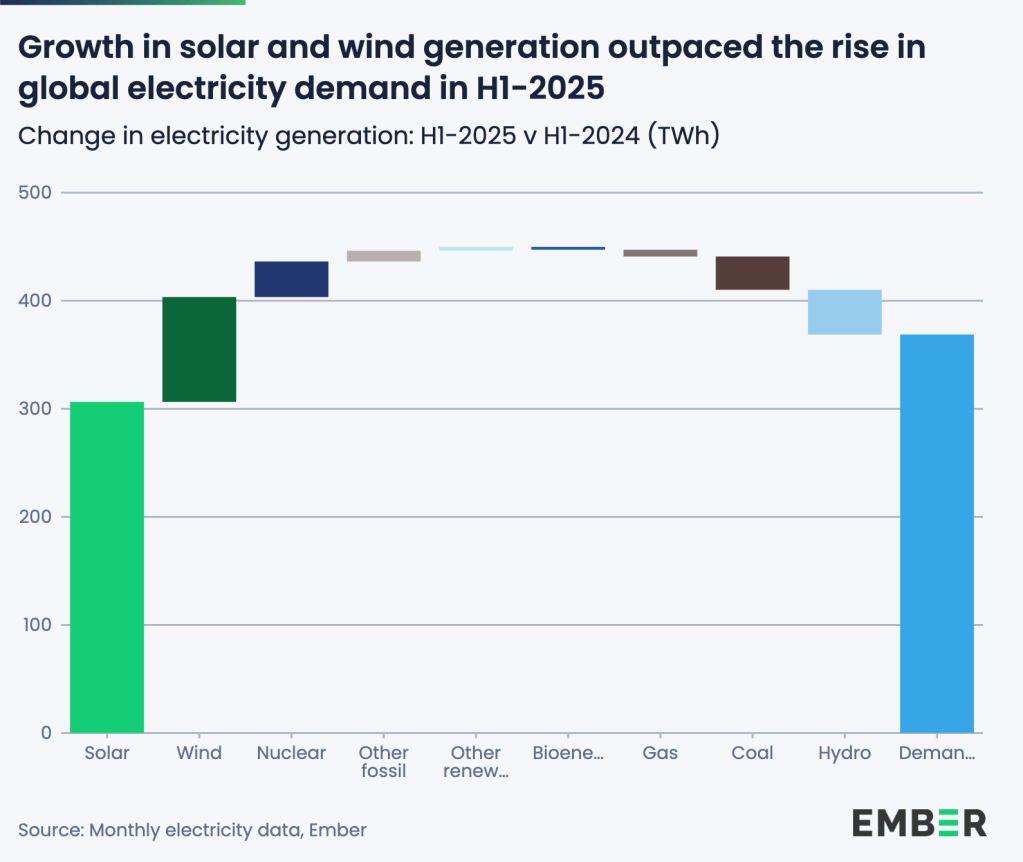

Solar and wind power aren’t just keeping up with global electricity demand anymore – they’re pulling ahead. According to a new analysis from energy think tank Ember, solar and wind combined outpaced global electricity demand growth in the first half of 2025. That shift led to a drop in both coal and gas generation compared to the same period last year. For the first time ever, renewables generated more power than coal globally.

“We’re seeing the first signs of a crucial turning point,” said Małgorzata Wiatros-Motyka, senior electricity analyst at Ember. “Solar and wind are now growing fast enough to meet the world’s growing appetite for electricity. This marks the beginning of a shift where clean power is keeping pace with demand growth.”

Solar leads the charge

Global electricity demand rose 2.6% in the first half of 2025 – an additional 369 terawatt-hours (TWh) year-over-year. Solar met a stunning 83% of that increase, growing by 306 TWh, or 31% year-over-year. Combined with steady wind expansion, renewables were able to meet rising demand and start displacing fossil fuels.

Coal generation fell 0.6% (-31 TWh), gas dropped 0.2% (-6 TWh), and overall fossil generation declined 0.3% (-27 TWh). As a result, global power sector emissions fell by 0.2%.

Renewables supplied 5,072 TWh of electricity in the first half of 2025 – up from 4,709 TWh a year earlier. Coal, by comparison, generated 4,896 TWh, down 31 TWh year-over-year. It’s the first time on record that clean energy has overtaken coal.

A global turning point

Ember’s analysis shows this is more than a blip. Solar and wind are now growing fast enough to meet new demand and begin cutting into fossil generation. As deployment accelerates, Ember expects clean power to outstrip demand growth for longer stretches, pushing fossil fuels into permanent decline.

But progress isn’t uniform across the globe. Among the world’s four biggest power markets – China, India, the US, and the EU – two saw fossil generation fall, while two saw it rise.

China remains the global clean energy powerhouse, adding more solar and wind capacity than the rest of the world combined. Its fossil generation fell 2% (-58.7 TWh) in the first half of 2025.

In India, clean power growth outpaced demand threefold. With electricity demand rising just 1.3% (+12 TWh) – far below the 9% surge seen last year – fossil generation dropped sharply: coal fell 3.1% (-22 TWh) and gas plunged 34% (-7.1 TWh).

In contrast, fossil generation rose in the US and EU. In the US, demand grew faster than renewables could keep up, leading to higher fossil fuel output. In the EU, weaker wind and hydro performance meant more gas and coal were needed to fill the gap.

What comes next

With half the world already past the peak of fossil fuel generation, Ember says the trend is clear: Clean power can keep up with rising electricity demand. But to lock in progress, deployment of solar, wind, and batteries needs to accelerate.

“Solar and wind are no longer marginal technologies – they’re driving the global power system forward,” said Sonia Dunlop, CEO of the Global Solar Council. “The fact that renewables have overtaken coal for the first time marks a historic shift. But to secure it, governments and industry must step up investment in clean energy and storage so affordable, reliable power reaches everyone.”

Ember’s Wiatros-Motyka added, “With technology costs continuing to fall, now is the perfect moment to embrace the economic, social, and health benefits that come with increased solar, wind, and batteries.”

Read more: FERC: Solar + wind made up 90% of new US power generating capacity to July 2025

The 30% federal solar tax credit is ending this year. If you’ve ever considered going solar, now’s the time to act. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024