Business Secretary Grant Shapps hints at autumn budget windfall tax expansion on energy firms due to ‘unexpected profits’

Business Secretary Grant Shapps has hinted that the government may extend the windfall tax on oil and gas companies in this month’s autumn budget as it tries to stabilise the UK’s public finances.

Speaking to Sky News with just 10 days to go before the government’s fiscal plans are unveiled, Mr Shapps said: “I mean, it is the case that because fuel prices have been so high, there have been unexpected profits, of course.

“But I think it’s important that we do carry on investing in making sure not on fossil fuels, but on the renewable energy as well, that we’ve we’ve got the capacity, we’ve got the ability to get that market moving as well.”

Sunak to raise migrant crossings with Macron – Politics latest

He added that the general public will “have to wait until the 17th” to know exactly which measures the government is going to pursue to tackle what the Resolution Foundation thinktank has said is a £40bn financial black hole.

Last week, an initial report in The Times suggested that Prime Minister Rishi Sunak and Chancellor Jeremy Hunt were planning to extend windfall taxes on oil and gas companies to raise an estimated £40bn over five years.

Mr Sunak and Mr Hunt want to maximise revenues from the windfall tax by increasing the rate from 25% to 30%, extending the policy until 2028, and expanding it to cover electricity generators – according to the paper.

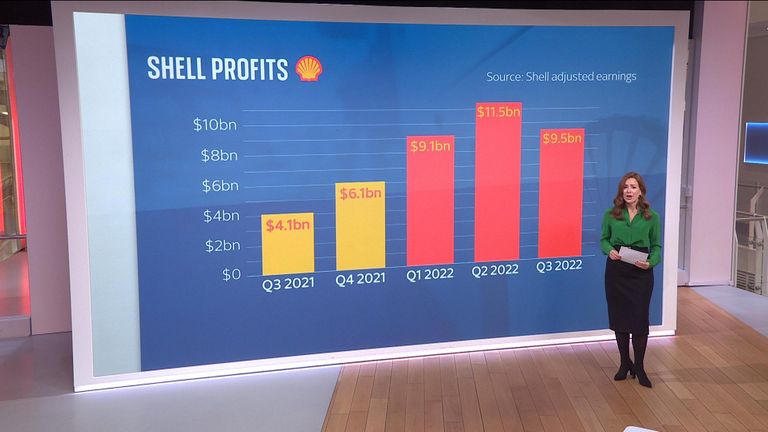

With BP unveiling profits that doubled to more than £7.1bn in the three months to September, pressure is continuing to mount for an enhanced windfall tax on oil and gas giants to help fill the Treasury coffers.

COP26 president Alok Sharma, who was demoted from the cabinet by Mr Sunak, has backed the move, saying: “We need to raise more money from a windfall tax on oil and gas companies and actively encourage them to invest in renewables.”

The Resolution Foundation said in a report last week that tax raises are “likely” to come soon as the government faces an “unpalatable menu” to find ways to re-balance the nation’s finances after former chancellor Kwasi Kwarteng’s ill-fated economic plans.

A combination of tax rises and spending cuts is likely to find the £40bn needed, it said.

Mr Sunak and Mr Hunt are currently figuring out how to tackle the abysmal economic forecast ahead of the autumn statement on 17 November, which was pushed back soon after Mr Sunak reappointed Mr Hunt.

Why do Shell’s profits matter?

The Resolution Foundation’s report added that a recession next year could be predicted by the government’s independent forecaster, the Office for Budget Responsibility.

Last week, the Bank of England raised its official interest rates by 0.75 percentage points to 3% and said the UK was already in recession.

It was the single biggest increase in more than three decades.

While GDP forecasts could be cut by up to 4% by the end of 2024.

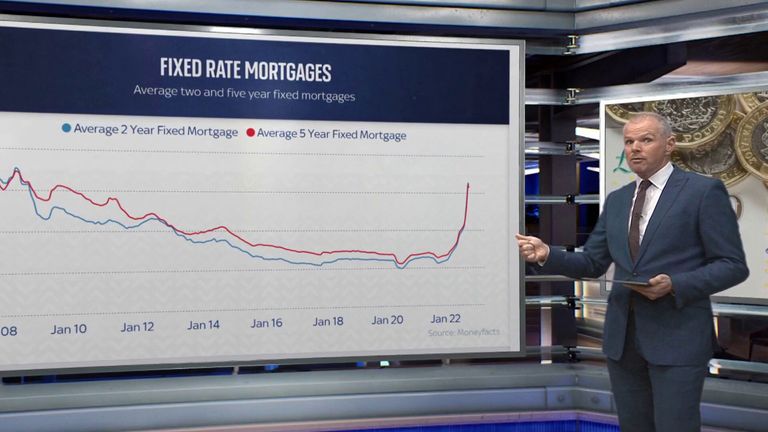

BoE interest rate hike explained

The autumn statement this month will likely encompass “rough” tax rises, Sky News has been told by a source in the Treasury.

The tax rises are likely to be across the board, although Mr Sunak and Mr Hunt are said to have agreed those with the “broadest shoulders” should bear the greatest burden, it is understood.

Read more: Demand for mortgages falls as customers grapple with high interest rates

Few concrete details have emerged but, according to The Times, public sector workers could face deep real-terms cuts to wages, with the Treasury reportedly looking at an increase of 2% across the board for 2023-24, at a time when inflation is expected to be well above that threshold.

The Resolution Foundation has said £9bn could be saved by the government choosing not to raise benefits and pensions in line with rising prices next year, but any such move would have a “huge” impact on those already struggling to make ends meet.

Another option would be to re-instate the health and social care levy to raise £15bn by 2026-2027, while around £2bn could be raised by extending the “stealth” freezes in income tax threshold by a further year to 2026-2027.

You’ve planned out your finances for the next 25 years, lost weekend after weekend to viewings and finally found your dream home.

And then, on your first night after getting the keys, you hear it: the muffled boom of drum and bass through paper-thin walls. At 11.23pm. On a Tuesday.

Turns out, you’ve spent an obscene amount of money buying a house next to a public nuisance.

It’s probably little comfort, but you’re not alone. In a survey of 1,000 homeowners by Good Move, 64% said they’d had “problems” with neighbours and one in 10 said it had got so bad they’d complained to the council.

Buyers beware

Sellers are legally obliged to disclose details of previous or ongoing disputes with neighbours in a Property Information Form (TA6) – failure to do so could lead to legal action.

The questions are limited, though, and how are you going to prove your seller knew about the drum and bass?

Read all the latest Money news here

“In reality, you have very few rights,” one estate agent insider told Money.

“You will never know if an agent has neglected to tell you about nuisance neighbours or if the seller did not tell the agent. A seller is hardly likely to volunteer the info if there have been any disputes.”

So maybe it’s the case that of all the roles you’ve had to master in the buying process – arranging surveys, scouring legal documents, packing everything you own – there’s one role you should have dedicated a bit more time to: detective.

We’ve spoken to top buying agents to get their advice on how to sniff out problem neighbours – and rounded up some of the lesser known tools that could save you a literal and figurative headache…

External clues

Henry Sherwood from The Buying Agents says most disputes arise from either noise or money issues.

“If the neighbouring property or building looks neglected, it probably means the neighbour does not have the funds to maintain it, or does not want to,” he said.

“If [it’s] an apartment, check out the communal parts on the floors above and below. Look for prams and excessive bikes that may indicate screaming babies or student flat shares.”

Flats with a porter/concierge are better protected, Sherwood says, as they are controlled by a management company and have someone onsite. Most flat leases also have sections relating to the type of renting allowed.

List of noise complaints

Some local councils keep a public register of noise complaints by postcode.

Here’s an example of Leeds City Council’s noise complaints register.

Next Door app (and local groups)

This is an app where local residents post about events, lost cats, bin collection dates and, inevitably, noise issues.

A simple search of “noise” in one area of north London found all of these complaints within the last month – and in each case the exact street was named:

• A second loud party on a weeknight on a small, residential street;

• A resident renovating his house in a loud and disruptive fashion. Alongside a photo of a huge pile of discarded bricks, the complainant says: “It has now been over six weeks of disruption through the summer holidays with no clear end date and neighbours being ignored”;

• Another resident living in an end terrace wrote that his walls were paper thin and he could hear his neighbour slamming doors and running up and down stairs;

• A photo of building work, with a resident complaining it was going on until midnight on a Sunday.

Away from the app, search out local groups on social media and see if you can join. Chances are, any serious issues will have been raised on there.

Speak to the neighbours

Not everyone is confident enough to knock on doors – but our survey on social media suggests most people think it’s perfectly acceptable.

91% of around 5,000 respondents said they’d make up an excuse to talk to a neighbour to suss out what they’re like.

“Just say you are thinking of buying the property next door and wondered what the parking was like at 4pm etc,” said Sherwood.

He says Sundays are a good day to bump into neighbours.

The internet is full of woeful tales of people who didn’t do their research.

In a thread on this topic on Mumsnet, Mommabear20 wrote: “Definitely knock on doors! We didn’t and regret it so much! Have a neighbour (over the road, terraced street, that has threatened to blow their house up at least six times in the last three years causing an evacuation of the entire area every time!”

If you do knock, be polite.

Sam Edington, director at Edingtons buying agent, said: “We recommend doing so casually and respectfully, simply introducing yourself, asking friendly, open questions about the area, and observing day-to-day life.”

Can you spot the clues? Pic: iStock

Airbnb

Henry Sherwood advises to look out for combination locks at the entrance to apartments – this is a giveaway that someone inside has listed on Airbnb.

Having a rolling cast of overnight guests might not bring problems, but you should consider if it’s a risk you want to take.

You could also search on Airbnb for the area you’re looking to buy – you may get lucky and find one of your immediate neighbours, in which case you can have a virtual snoop around their house for clues about their lifestyle.

Crime stats

While it won’t provide information on your specific neighbours, sites such as Police.uk allow you to check and map crime stats in a local area.

Find out if your neighbour is a landlord

Many councils keep a public register of licenced landlords or houses of multiple occupancy.

For example, Enfield Council allows you to type in your postcode – any landlords on your street will appear. Buckinghamshire Council lets you download an excel spreadsheet of HMOs.

Sam Edington deals in a higher end of the market and recalls only one nightmare neighbour scenario in his 23 years in the industry – it involved a tenant.

“We acted for a charming client buying a beautiful flat just off Hampstead Heath, and shortly after they moved in, a belligerent tenant with substance abuse issues arrived in the building, causing several months of distress.

“Fortunately, with our guidance, complaints to the managing agents and the council helped resolve the situation and restore calm.”

Ask questions of the seller

Henry Sherwood says it is essential to ask if a seller knows their neighbours and whether they’re owner-occupiers or renters.

If you meet the owner, ask them questions – chances are they’re not going to reveal negative details, but the more questions you ask, the harder a lie is to maintain.

Read more:

The supercommuters taking 24-hour journeys to the office

‘My £1.2k TV broke… but they won’t give me money back’

Ask them questions like: are you friends with your neighbours, have you ever had any issues with noise, are there any resident WhatsApp groups.

“If you don’t meet the owner, don’t be afraid to prepare a list of questions for the seller about the neighbours and be specific,” said Sherwood.

Get your solicitor to ask questions

An experienced property solicitor is vital to ask the right questions as the purchase progresses.

Sherwood said: “During the enquiries phase of the conveyancing you can ask your solicitor to ask if there have been any disputes or altercations. The seller is less likely to lie if it goes through legal channels and there is a record of it.”

How many times has the house sold recently?

“Stability is a good sign,” says Sam Edington, so it’s worth asking, or trying to find out, how long neighbours have been around.

Sites such as Zoopla and Rightmove have some historical sale and listing data that could help establish if the property you’re buying has struggled to sell or been sold multiple times in recent years.

The latter could be a red flag that’s worth further investigation.

Planning permission

The planning section of local council websites will inform you of any proposals or active plans in the area where you’re buying.

This will cover things like extensions that could alter your view or result in a period of building work.

Google Earth/Street View

You can use this tool to find out how the area has changed over the years…

This is unlikely to provide you with that crucial bit of information, but you’re trying to build a picture.

Golden rules

Henry Sherwood has a golden rule he shares with clients: “Never buy without viewing a minimum of twice, once during the week and once at the weekend.

“If possible, also take a look from the outside late night after agents have shut at 9pm or 10pm. Check out the times that are important to you.

You may just get unlucky

Ultimately, there’s no way to guarantee a peaceful and quiet co-existence.

Sherwood said: “There are no guarantees who your neighbours will be long term as the current owners could sell, rent it, turn into an HMO or Airbnb.”

Back on the Mumsnet thread we mentioned earlier, a poster called Thirtytimesround illustrated the point: “We popped back a few times at different times of day to just sit in car near house and listen to see if anyone noisy. It helped. But honestly so much luck is involved.

“Like, we bought in a quiet road in a smart area and my neighbours are a lovely, kind, generous couple in their forties. And their bedroom is the other side of the wall from ours and they have very noisy sex 😐 Plus shortly after we moved in they bought a dog that barks all the frickin’ time and then their son took up the drums. Nothing we could have done to discover that before we moved in – it’s just luck.

“We are probably gonna move because of them!!”

A healthcare AI company which claims to be used by more than 60% of NHS GPs will this week announce a funding injection led by one of Wall Street’s most prominent investors.

Sky News has learnt that Heidi, which promises to reduce doctors’ workloads by removing layers of bureaucracy from their daily tasks, will unveil a $65m (£48m) Series B fundraising which will value the company at $465m (£346m).

The round has been led by Point72 Private Investments, part of the investment empire of Steven Cohen, the billionaire asset management tycoon.

Existing investors including Blackbird, Headline and Latitude – which is part of the London-based venture capital group LocalGlobe – are also participating in the funding boost.

The raise brings the total sum of funding injected into Heidi since it was founded by a trio of Australian healthcare professionals to nearly $100m.

Heidi says its technology is now used to support more than 340,000 patient consultations each week in the UK.

It adds that organisations utilising it include One Care and Modality Partnership, the NHS’s largest GP “super-partnership”.

Heidi Health CEO, Dr Thomas Kelly. Pic: Heidi Health

Heidi is also running pilot programmes with NHS Trusts across the North West London Acute Provider Collaborative – a group of hospitals serving a local population of approximately 2.2 million people – as well as One LSC, a collective of five NHS Trusts in Lancashire and South Cumbria which serves nearly 1.8 million people.

The company says its administrative aids have already saved British doctors 3 million hours annually by cutting paperwork and other bureaucracy.

It automates tasks such as clinical documentation, evidence search, and follow-up communications with patients.

More widely, Heidi claims to have supported more than 70 million patient consultations globally over the last 18 months, returning more than 18 million hours to frontline clinicians by streamlining administrative functions.

“It is untenable that healthcare demand continues to rise while clinical time continues to shrink,” Dr Thomas Kelly, the CEO and co-founder of Heidi, said.

“Building a sustainable healthcare system requires expanding clinical capacity without compromising clinician wellbeing or patient safety.”

The new funding will be used to accelerate Heidi’s expansion in the US, UK and Canada, including doubling its workforce in Britain to meet growing NHS demand.

Read more from Sky News:

WSL Football bosses hire Goldman to kick off financing review

French air traffic controllers call off strike

“What we’re witnessing with Heidi in the UK’s NHS isn’t just fast growth, it’s a clinician-led movement,” said Ferdi Sigona, a partner at Latitude.

“When doctors themselves are championing a tool so passionately – from individual practices to major NHS Trusts serving millions of patients – we know we’re backing a company with universal appeal across healthcare.”

Alongside the funding round, Heidi is also expected to announce the appointment of Paul Williamson, a former executive at the fintech Plaid, as chief revenue officer, and former Microsoft chief medical officer Dr Simon Kos to the same role.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment12 months ago

Environment12 months agoHere are the best electric bikes you can buy at every price level in October 2024