US inflation figures are lower than Wall Street forecast – but there’s pain ahead for UK

Today’s dramatic US inflation figures raise hopes that the Federal Reserve is winning the fight against the monster.

Consumer price inflation in October came in at 7.7% on a year-on-year basis – lower than the 7.9% Wall Street had expected – and at 0.4% on a month-on-month basis which, again, was lower than the 0.6% that had been forecast.

This was a landmark in itself, since it is the first time since February this year that the headline rate of annual inflation has gone below 8%.

More important still are the so-called ‘core’ inflation numbers. This is the number that strips out volatile elements such as energy, food and tobacco and is relied on by the Fed as an accurate barometer of underlying inflationary pressures in the economy.

Here, too, the numbers were heading in the right direction.

On a year-on-year basis, core inflation came in at 6.3%, which was lower than the 6.5% expected. And, on a month-on-month basis, core inflation came in at 0.3% against the 0.5% that had been forecast on Wall Street.

The figures will raise hopes that the Fed will not have to raise US interest rates as aggressively in future as it has been.

The Fed chair, Jerome Powell, indicated last month that the Fed was even prepared to risk a US recession in order to bring inflation under control and the central bank has raised its main policy, Fed Funds, by 0.75% in each of its last four policy meetings.

The market reaction was instant. US stock futures rose, as did US Treasuries (US government IOUs), sending Treasury yields (which move in the opposite direction to the price) lower.

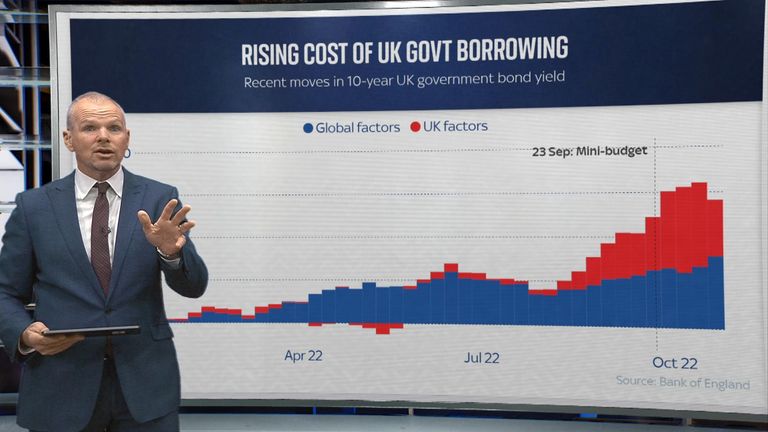

There was a similar reaction in Europe. The FTSE-100, which had been languishing in negative territory all morning, immediately reversed those losses to post a 1.5% gain. Yields on gilts – UK government bonds and the focus of so much attention lately – also fell.

Why are interest rates rising?

On the currency markets, the prospect of the Fed going easier on interest rate rises from now on sent the dollar lower. Sterling is currently ahead by some 2% against the greenback and heading back up towards $1.16. The euro has also posted a gain of more than 1% against the greenback on the session.

Seema Shah, chief global strategist at Principal Asset Management, said: “The first downside surprise in inflation in several months will inevitably be received by an equity market ovation.

“Not only is headline CPI back below its pre-Russia-Ukraine conflict level, but some details of the report suggest the long-awaited decline in inflation could now be underway.

“For now, however, despite both core and headline inflation easing, the best we can expect from the Fed is a downshift in the pace of tightening. A 0.5% hike, rather than 0.75%, in December is clearly on the cards but, until we have had a run of these types of CPI reports, a pause is still some way out.

“Let the market enjoy today, it still has another 100bps [1%] or so of tightening to commiserate.”

Stuart Clark, portfolio manager at wealth manager Quilter, added: “Inflation in the US has once again fallen, giving some momentum to the idea that the worst is now behind us.

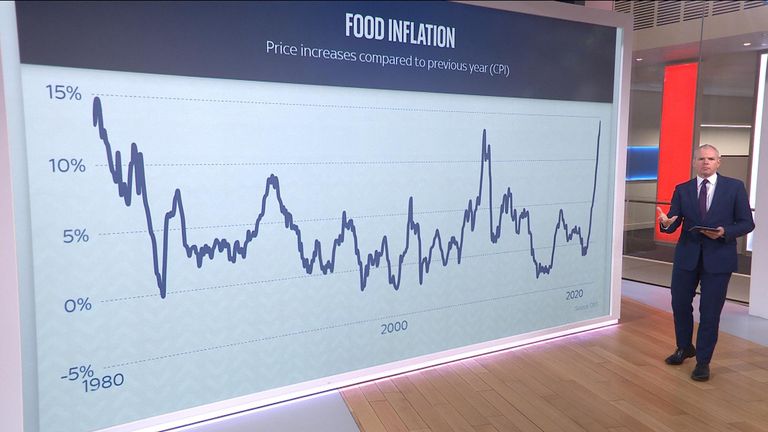

“The rate is lower than expectations and this will provide some relief to consumers and the wider market, however it is worth noting food and shelter is still increasing, so we’re not completely out of the woods yet.”

As inflation rises above 10%, Paul Kelso looks at what’s causing the surge

Those are points worth bearing in mind. At 7.7%, the headline rate of inflation remains significantly higher than anything most American households or businesses have experienced during the last four decades. The Fed is still going to have to carry on raising the cost of borrowing and not least because, as was shown by other figures published today, the US jobs market still remains immensely strong.

And on this side of the Atlantic, it is by no means clear that inflation has even peaked, as it appears to have in the US.

The headline CPI figure for September was 10.1% and it is unlikely to be any lower when the October figure is published nine days from now. The same can be said for the eurozone where, in October, headline CPI hit 10.7%.

Read more:

Autumn budget: How could PM and Hunt reduce ‘£60bn financial black hole’?

So there is still a lot of pain to come for UK households and businesses.

That said, it is unalloyed good news that inflation in the US is starting to moderate, albeit remaining at a historically high rate.

So far as the fight against inflation goes, the US economy is not out of the tunnel yet, but the light at the end of it is moving into view.

Tech giants Apple and Amazon have defied industry predictions with better-than-expected financial results.

Apple’s success is largely thanks to record-breaking iPhone sales, while Amazon’s is down to cloud computing arm Amazon Web Services (AWS), in spite of last week’s outage which knocked out thousands of websites.

AWS revenue accelerated 20.2% to $33bn (almost £25bn), which CEO Andy Jassy said was a pace it hadn’t seen since 2022. AWS accounts for 60% of Amazon’s total operating income.

Cloud growth has been a key focus for the company in the face of ever-growing pressure from rivals Google and Microsoft, which also reported revenue leaps this week.

While welcoming its latest results, Amazon has also issued a cautious sales outlook. File pic: Reuters

iPhone on the charge

With Donald Trump introducing punishing tariffs on India and China – the main manufacturing hubs for the iPhone – Apple’s record revenue has been even more welcome for boss Tim Cook.

The tariffs cost Apple $1.1bn (£824m) during the past quarter and are expected to cost another $1.4bn (just over £1bn) during the final three months of the year, but the new iPhone 17 range is a hit.

Consumers have been won over by a price point that didn’t stray above last year’s model, particularly in the US and Europe, leading to sales totalling $49bn (£36.1bn) during the July-September period – 6% up on last year.

Global market analyst IDC says almost 59 million iPhones were sold worldwide in the July-September quarter, putting Apple second behind Samsung at 61.4 million of their Android-powered phones.

Buoyed by the iPhone results, Apple earned $27.5bn (£21.4bn), or $1.85 per share (£1.44), nearly doubling its profit from a year ago. Revenue climbed 8% from a year ago to $102.5bn (£80bn).

Read more from Sky News:

Andrew to lose ‘prince’ title and move out of Royal Lodge

PM says chancellor will face no further action over rental issue

Tim Cook was famously once referred to by Donald Trump as ‘Tim Apple’. Pic: Reuters

Wall Street analysts had been cautious about both companies, and their tech rivals, because of uncertainty caused by tariffs and whether investment in AI has been overplayed.

While welcoming its latest results, Amazon has issued a cautious sales outlook for the fiscal fourth quarter, citing continued Trump tariffs as a possible bump in the revenue road.

Companies, including Amazon, are introducing AI into nearly every facet of their operations in hopes of reducing costs and boosting productivity. There have been tens of thousands of job losses at US tech firms this year.

On Wednesday, Federal Reserve Chair Jerome Powell said he did not believe the AI boom was a speculative bubble like the dot-com era, when many companies were “ideas rather than businesses”.

Today’s AI leaders “actually have earnings,” he said.

For all the brinkmanship, for all the high stakes and attempts to wield maximum leverage, in the end, there was clear recognition from both the US and China that a degree of stabilisation was necessary.

The fact that some progress has been made on a relatively wide range of issues speaks to that.

But there are real questions about how deep that progress runs and how easily, in the hands of two leaders who staked both their reputations on being strong and unyielding, it could all come crashing down.

Follow the latest: Trump teases ‘large-scale’ energy deal

From the very outset, the differences in style could not have been more stark.

As the two posed for the introductory handshake, Donald Trump moved quickly to dominate the space – leaning in, doing all the talking, even quipping to the gathered reporters that Xi Jinping is “a very strong negotiator, and that isn’t good”.

That didn’t raise as much as an eyebrow from the Chinese leader.

Xi doesn’t like or respond well to unscripted moments; Trump, on the other hand, lives for them.

It might seem like a relatively inconsequential detail, but it speaks to how difficult it has been for two such opposing systems to see eye to eye, and how many stumbling blocks remained.

But it seems today, at least some of that was overcome.

Donald Trump and Xi Jinping held talks in Busan, South Korea. Pic: Reuters

Indeed, there appears to have been an agreement on key issues such as the movement of rare earth minerals, the purchase of soybeans, the reduction of tariffs and the crackdown on the trade of fentanyl and the chemicals used to make it.

There was further consensus to keep talking about the sale of high-end US chips and to work together to try to end the war in Ukraine.

None of this is insignificant, but Trump’s assessment of it all as a “12 out of 10” likely brushes over many much thornier issues.

Trump scores meeting with Xi a ’12 out of 10′

The reality is that there is still a great gulf between them; there are many more barriers to trade than there were at the start of the year, there are still a raft of deep political and structural issues that divide them and the levels of distrust the trade war has left will take more than just one meeting to fix.

Disagreements, such as the future status of Taiwan, for example, weren’t even mentioned today.

There is still a gulf between the two leaders, despite the pair agreeing on key issues at the summit. Pic: Reuters

There also doesn’t appear to be any guarantees baked in, and thus, there is nothing to prevent either party from reneging on what has been agreed and ramping pressure back up as soon as another issue arises.

And, given the characters involved, that feels all too likely.

Indeed, both sides, for different reasons, have found political advantage in the “maximum pressure” style brinkmanship we’ve seen in recent months.

Read more:

Donald Trump says tariffs will be cut

Everything you need to know about the meeting

Xi in particular cannot now be seen to cave in to Trump’s pressure and, economically at least, China doesn’t need to.

There was an agreement today that the two would meet again in the early part of next year; Trump plans to visit China in April.

This at least offers more diplomatic opportunity, but it would perhaps be naive to assume it will all be plain sailing until then.

Donald Trump has described crucial trade talks with Chinese President Xi Jinping as “amazing” – and says he will visit Beijing in April.

The leaders of the world’s two biggest economies met in South Korea as they tried to defuse growing tensions – with both countries imposing aggressive tariffs on exports since the president’s second term began.

Aboard Air Force One, Mr Trump confirmed tariffs on Chinese goods exported to the US will be reduced, which could prove much-needed relief to consumers.

It was also agreed that Beijing will work “hard” to stop fentanyl flowing into the US.

Semiconductor chips were another issue raised during their 100-minute meeting, but the president admitted certain issues weren’t discussed.

“On a scale of one to 10, the meeting with Xi was 12,” he told reporters en route back to the US.

‘Their handshake was almost a bit awkward’

Xi a ‘tough negotiator’, says Trump

The talks conclude a whirlwind visit across Asia – with Mr Trump saying he was “too busy” to see Kim Jong Un.

However, the president said he would be willing to fly back to see the North Korean leader, with a view to discussing denuclearisation.

Mr Trump had predicted negotiations with his Chinese counterpart would last for three or four hours – but their meeting ended in less than two.

The pair shook hands before the summit, with the US president quipping: “He’s a tough negotiator – and that’s not good!”

It marks the first face-to-face meeting between both men since 2019 – back in Mr Trump’s first term.

Donald Trump and Xi Jinping. Pic: AP

There were signs that Beijing had extended an olive branch to Washington ahead of the talks, with confirmation China will start buying US soybeans again.

American farmers have been feeling the pinch since China stopped making purchases earlier this year – not least because the country was their biggest overseas market.

Chinese stocks reached a 10-year high early on Thursday as investors digested their meeting, with the yuan rallying to a one-year high against the US dollar.

Analysis: A fascinating power play

Sky News Asia correspondent Helen-Ann Smith – who is in Busan where the talks took place – said it was fascinating to see the power play between both world leaders.

She said: “Trump moved quickly to dominate the space – leaning in, doing all the talking, even responding very briefly to a few thrown questions.

“That didn’t draw so much as an eyebrow raise from his counterpart, who was totally inscrutable. Xi does not like or respond well to unscripted moments, Trump lives for them.”

Read more from Sky News:

US cuts interest rates as inflation fears ease

Is Trump preparing for war with Venezuela?

Will Trump really run for a third term?

On Truth Social, Mr Trump had described the summit as a gathering of the “G2” – a nod to America and China’s status as the world’s two biggest economies.

While en route to see President Xi, he also revealed that the US “Department of War” has now been ordered to start testing nuclear weapons for the first time since 1992.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024