Jeremy Hunt to defend autumn statement amid warning of record fall in living standards

Jeremy Hunt will continue to defend his autumn statement today as experts warn of a record fall in living standards across the country.

The chancellor presented his economic plan to parliament on Thursday, littered with stealth taxes and curbs on government spending amounting to £55bn in an attempt to plug the black hole in public finances.

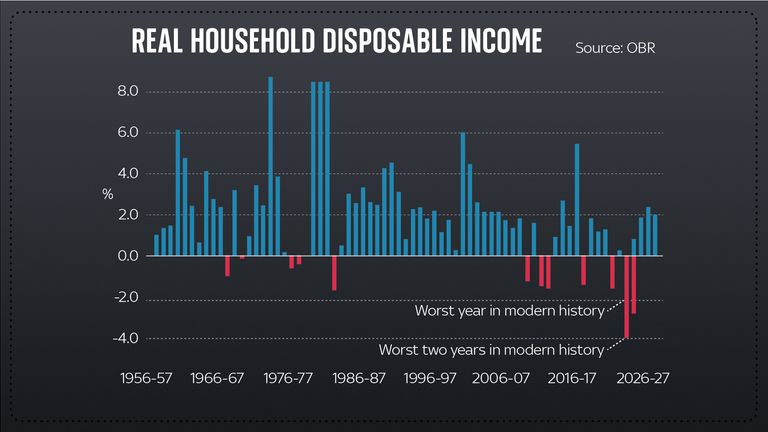

But the independent Office for Budget Responsibility warned the disposable incomes of UK households would fall by 7.1% over the next two years – the lowest level since records began in 1956/7, and taking incomes down to 2013 levels.

Politics live: Top Tory warns ‘jury is out’ on chancellor’s plans

As a result of the Mr Hunt’s announcements, the tax burden in the UK will also now be at its highest since the Second World War, and there are stark warnings about increased bills and higher unemployment as the recession takes hold – as well as predictions the economy will still shrink 1.4% in 2023.

But most of the difficult decisions on spending have been postponed until after the next general, due in 2024.

Both the Resolution Foundation and the Institute for Fiscal Studies will lay out their own analysis of the plans later this morning, but Treasury analysis already suggests around 55% of households will be worse off as a result of the measures.

Meanwhile, Labour has blamed “12 weeks of Conservative chaos” and “12 years of Conservative economic failure” for the bleak outlook.

Shadow chancellor Rachel Reeves accused the government of forcing the UK economy into a “doom loop where low growth leads to higher taxes, lower investments and squeezed wages, with the running down of public services”.

Click to subscribe to the Sky News Daily wherever you get your podcasts

During his statement, Mr Hunt distanced himself from the philosophy of Liz Truss’s short-lived government – which promised billions of unfunded tax cuts and sent the markets into turmoil.

Yet, while the chancellor froze tax thresholds, lowered the point the higher rate of income tax kicks in and extended the windfall tax on energy firms (the latter, a Labour policy) amid other measures, he also promised more spending on the NHS, social care and education, as well as re-committing to uprating pensions and benefits in line with inflation.

Hunt questioned over autumn statement

Mr Hunt also pledged to continue support for energy bills from April next year – though raising the cap to £3,000 for the average household.

Speaking to reporters after the announcement, he said the government was “helping every bit as much as we can” to reduce the impact of the recession on households and businesses, as well as protecting public services.

But he pointed to those spending decisions, adding: “As soon as the recession is behind us, then, yes, we will consolidate to make sure that we’re balancing our books – and I think that’s what people would want.”

’12 weeks of Conservative chaos’ – Rachel Reeves

While many in his party were supportive of the “difficult decisions”, the chancellor made in light of the energy crisis, the war in Ukraine and the fallout from the pandemic – as well as Ms Truss’s tenure in office – other Tories warned against hiking taxes while the country is in a recession.

Former party leader Sir Iain Duncan Smith told Sky News: “My worry is they’ve estimated that they will get certain revenues from their tax rises [but] those tax rises could end up damaging the economy and they won’t get the revenues thereafter, which means they’ll be back again looking for more.

“[There] is every chance that tax increases don’t yield what you think they will, so this could lead to a deeper recession. We need to watch that very carefully and see where it goes.”

Read more:

Key announcements from the autumn statement

Electric car owners to pay road tax from 2025

Jaw-dropping change of tack by Jeremy Hunt – analysis

And former Wales Secretary David Jones told the Telegraph that the if high taxes continue, “the prospects of Tories winning the next election… are going to become more remote”.

Opposition parties were also quick to condemn the plan, with Liberal Democrat MP Sarah Olney saying it will “cause untold pain for everyone”, and the SNP’s Kirsty Blackman saying it “ushered in a new era of damaging austerity cuts”.

MPs will debate the measures in the Commons on Monday and Tuesday next week.

Chancellor Jeremy Hunt will be talking to Sky News at around 7am this morning about his autumn statement announcement

Shares in UK banks have fallen sharply on the back of a report which urges the chancellor to place their profits in her sights at the coming budget.

As Rachel Reeves stares down a growing deficit – estimated at between £20bn-£40bn heading into the autumn – the Institute for Public Policy Research (IPPR) said there was an opportunity for a windfall by closing a loophole.

It recommended a new levy on the interest UK lenders receive from the Bank of England, amounting to £22bn a year, on reserves held as a result of the Bank’s historic quantitative easing, or bond-buying, programme.

Money latest: Ryanair changes cabin bag sizing

It was first introduced at the height of the financial crisis, in 2009.

The left-leaning think-tank said the money received by banks amounted to a subsidy and suggested £8bn could be taken from them annually to pay for public services.

It argued that the loss-making scheme – a consequence of rising interest rates since 2021 – had left taxpayers footing the bill unfairly as the Treasury has to cover any loss.

Why taxes might go up

The Bank recently estimated the total hit would amount to £115bn over the course of its lifetime.

The publication of the report coincided with a story in the Financial Times which spoke of growing fears within the banking sector that it was firmly in the chancellor’s sights.

Her first budget, in late October last year, put businesses on the hook for the bulk of its tax-raising measures.

Ms Reeves is under pressure to find more money from somewhere as she has ruled out breaking her own fiscal rules to help secure the cash she needs through heightened borrowing.

Is Labour plotting a ‘wealth tax’?

Other measures understood to be under consideration include a wealth tax, new property tax and a shake-up that could lead to a replacement for council tax.

Analysts at Exane told clients in a note: “In the last couple of years, the chancellor has been protective of the banks and has avoided raising taxes.

“However, public finances may require additional cash and pressures for a bank tax from within the Labour party seem to be rising,” it concluded.

The investor flight saw shares in Lloyds and NatWest plunge by more than 5%. Those for Barclays were more than 4% lower at one stage.

A spokesperson for the Treasury said the best way to strengthen public finances was to speed up economic growth.

“Changes to tax and spend policy are not the only ways of doing this, as seen with our planning reforms,” they added.

The man dubbed “Britain’s most hated boss” for his controversial policy of sacking hundreds of seafarers and replacing them with cheaper agency staff is to quit.

Sky News can exclusively reveal that Peter Hebblethwaite, the chief executive of P&O Ferries, is leaving the company.

Sources said he had decided to resign for personal reasons.

Money latest: The exact time to book train ticket at bargain price

Mr Hebblethwaite joined the ranks of Britain’s most notorious corporate figures in 2022 when P&O Ferries – a subsidiary of the giant Dubai-based ports operator DP World – said it was sacking 800 staff with immediate effect – some of whom learned their fate via a video message.

The policy, which Mr Hebblethwaite defended to MPs during subsequent select committee hearings, erupted into a national scandal, prompting changes in the law to give workers greater protection.

Under the new legislation, the government plans to tighten collective redundancy requirements for operators of foreign vessels.

In a statement issued in response to a request from Sky News, a P&O Ferries spokesperson said: “Peter Hebblethwaite has communicated his intention to resign from his position as chief executive officer to dedicate more time to family matters.

Peter Hebblethwaite gives evidence to a committee of MPs in 2022. Pic: PA

“P&O Ferries extends its gratitude to Peter Hebblethwaite for his contributions as CEO over the past four years.

“During his tenure the company navigated the challenges of the COVID-19 pandemic, initiated a path towards financial stability, and introduced the world’s first large double-ended hybrid ferries on the Dover-Calais route, thereby enhancing sustainability.

“We extend our best wishes to him for his future endeavours.”

A source close to the company said it anticipated making an announcement on Mr Hebblethwaite’s successor in the near term.

A former executive at J Sainsbury, Greene King and Alliance Unichem, Mr Hebblethwaite joined P&O Ferries in 2019, before taking over as chief executive in November 2021.

Insiders claimed on Friday that he had “transformed” the business following the bitter blows dealt to its finances by the COVID-19 pandemic and – to some degree – by the impact of Britain’s exit from the European Union.

A union protest is shown at the height of the mass sackings row in 2022

P&O Ferries carries 4.5 million passengers annually on routes between the UK and continental European ports including Calais and Rotterdam.

It also operates a route between Northern Ireland and Scotland, and is a major freight carrier.

The company’s losses soared during the pandemic, with DP World – its sole shareholder – supporting it through hundreds of millions of pounds in loans.

Its most recent accounts, which were significantly delayed, showed a significant reduction in losses in 2023 to just over £90m.

The reduction from the previous year’s figure of almost £250m was partly attributed to cost reduction exercises.

The accounts also showed that Mr Hebblethwaite received a pay package of £683,000, including a bonus of £183,000.

“I reflected on accepting that payment, but ultimately I did decide to accept it,” he told MPs.

“I do recognise it is not a decision that everybody would have made.”

The row over his pay was especially acute because of his admission that P&O Ferries’ lowest-paid seafarers received hourly pay of just £4.87.

Mr Hebblethwaite had argued since the mass sackings of 2022 that the company would have gone bust without the drastic cost-cutting that it entailed.

The company insisted at the time that those affected by the redundancies had been offered “enhanced” packages to leave.

Last October, the then transport secretary, Louise Haigh, said: “The mass sacking by P&O Ferries was a national scandal which can never be allowed to happen again,” adding that measures to protect seafarers from “rogue employers” would prevent a repetition.

“This issue has been ignored for over 2 years, but this new government is moving fast and bringing forward measures within 100 days,” Ms Haigh added.

“We are closing the legal loophole that P&O Ferries exploited when they sacked almost 800 dedicated seafarers and replaced them with low-paid agency workers and we are requiring operators to pay the equivalent of National Minimum Wage in UK waters.

“Make no mistake – this is good for workers and good for business.”

The minister’s description of P&O Ferries as “rogue”, and suggestion that consumers should boycott the company, sparked a row which threatened to overshadow the government’s International Investment Summit last October.

Sky News’s business and economics correspondent, Paul Kelso, revealed that DP World had withdrawn from participating in the event, and paused a £1bn investment announcement.

The company relented after Sir Keir Starmer publicly distanced the government from Ms Haigh’s characterisation of DP World.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment11 months ago

Environment11 months agoHere are the best electric bikes you can buy at every price level in October 2024