Google has avoided mass layoffs so far, but employees worry their time may be coming

Google CEO Sundar Pichai speaks on stage during the annual Google I/O developers conference in Mountain View, California, May 8, 2018.

Stephen Lam | Reuters

As industry-wide layoffs hit bigger tech names, some Google workers worry they’re next.

While Google has so far avoided the widespread job cuts that have hit tech companies, particularly those supported by a slumping ad market, internal anxiety is on the rise, according to documents viewed by CNBC and employees who spoke on the condition of anonymity.

Alphabet executives have stressed the need to sharpen “focus,” bring down costs of projects and make the company 20% more efficient. There’s also been a recent change in performance reviews, and some employees point to declining travel budgets and less swag as signs that something bigger may be on the horizon.

In July, Alphabet CEO Sundar Pichai launched the “Simplicity Sprint” in an effort to bolster efficiency during an uncertain economic environment. Just a few miles up the road, Meta told employees this month that it’s laying off 13% of its staff, or more than 11,000 employees, as the company reckons with declining ad revenue. Snap announced a 20% cut in August, and Twitter just slashed about half its workforce under the leadership of new owner Elon Musk. Elsewhere in Silicon Valley, HP said on Tuesday it plans to lay off 4,000 to 6,000 employees over the next three years.

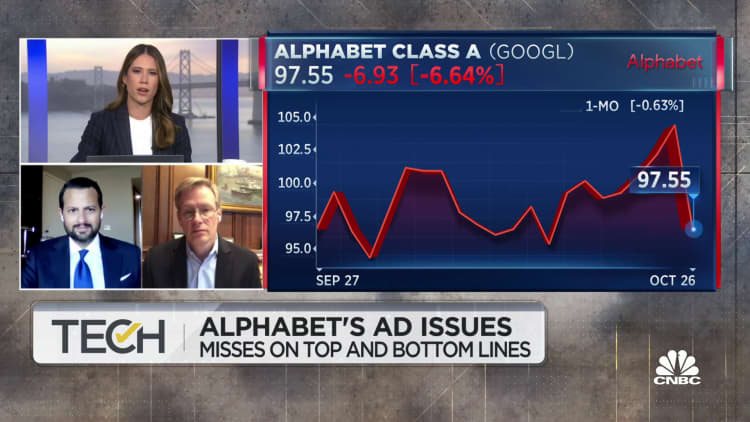

Google’s business hasn’t been hit as hard as many of its peers, but the combination of a potential recession, soaring inflation and rising interest rates is having a clear impact. Last month, the company said YouTube’s ad revenue shrank from a year earlier as Google generated its weakest period of growth since 2013, other than one quarter during the pandemic. Google said at the time that it would significantly reduce headcount growth in the fourth quarter.

The crypto market, which put a dent in Google’s latest results, has fallen even further with the collapse of crypto exchange FTX, leading to increased concerns about industry contagion.

‘Don’t fire us please’

Cuts at Google have already taken place around the edges.

The company canceled the next generation of its Pixelbook laptop, slashed funding to its Area 120 in-house incubator and said it would be shuttering its digital gaming service Stadia.

Concerns about terminations are mounting, at least in certain corners. And some employees are turning to memes to express their anxieties through humor.

One internal meme shared with CNBC shows a before-and-after animated character. On the before side, the figure has his hands raised with the caption “inflation pay rise!” On the after side, a frightened character sits alongside the caption, “don’t fire us please.”

Another meme has names of tech companies — “Meta, Twitter, Amazon, Microsoft” — that recently conducted layoffs next to an image of a worried anime character. There were also memes created in reference to a statement last week from activist investor TCI Fund Management, which called on Pichai to cut salaries and headcount through “aggressive action.”

Among the workforce, Pichai found himself on the defensive in September, as he was forced to explain the company’s changing position after years of supercharged growth. Executives said at the time that there would be small cuts, and they didn’t rule out layoffs.

At a more recent all-hands meeting, a number of questions regarding the potential for layoffs were highly rated by staffers on Google’s internal question-asking system called Dory. There were also questions about whether executives mismanaged headcount.

“It appears that we added 36k full-time role YoY, increasing headcount by about 24%,” one top-rated question read. “Many teams feel like they are losing headcount, not gaining it. Where did this headcount go? In hindsight, and given concerns around productivity, should we have hired so rapidly?”

Employees wanted details following the company’s latest earnings call and comments from CFO Ruth Porat regarding possible cuts.

One question read: “Can we get some more clarity on how we’re approaching headcount for 2023? Do we have any sense of how long we need to plan for difficult headwinds?”

Other questioners asked if employees “should expect any direct consequence to our teams, direction and/or compensation to reduced profits we saw in the earnings call” and wondered, “how are we going to achieve 20% more productivity? Will refocus be enough or are we expecting layoffs?”

Change to performance reviews

Furthering employee stress levels was a recent change to performance reviews and upcoming evaluation check-ins.

Earlier this year, Google said it was ditching its long-held practice of handing out lengthy promotion packets, which were long forms employees needed to fill out and that included reviews from bosses and co-workers. The company switched to a streamlined process it calls Googler Reviews and Development (GRAD).

A Google spokesperson said in an emailed statement that the GRAD system was launched “to help employee development, coaching, learning and career progression throughout the year,” adding that it “helps establish clear expectations and provide employees with regular feedback.”

Google said a new system would result in higher pay, but workers say the overhaul has left more room for ambiguity in ratings at a time when the company is looking for ways to cut costs.

The planned overhaul has already run into problems. The company decided to end its use of Betterworks, a program that was supposed to help with evaluating performance, employees told CNBC. Executives said they planned to instead use a home-grown tool, but the change has come uncomfortably close to expected year-end performance checks.

A guide titled “Support Check-Ins,” which are performance reviews targeting certain employees, began appearing in internal forums. The document, viewed by CNBC, says for those who receive the review, “the current performance trajectory is headed toward, or already is in, a lower rating.”

Three steps are recommended for check-ins. The first directs workers to “breathe,” before taking in managers’ feedback. Second is, “understand the feedback,” and third is to “devise a plan.” The document says check-ins may affect 10% to 20% of staffers over the course of a year.

Add it all up, and one big question employees are asking is — will a bunch of small cuts turn into something grander in the future?

CNBC reported last month that employees and executives clashed on the topic of cutbacks to things like swag, travel and holiday celebrations. Workers complained about a lack of transparency around travel cuts and asked why the company wasn’t saving money by cutting executive salaries.

Google engineering leaders recently began cracking down on employees’ ability to access links to the internal meme generator called Memegen, a repository of user-generated memes that has long been a part of the company’s open culture.

Last month, a Google vice president of corporate engineering said employees need to remove Memegen links from their profile pages, internally known as “Moma.” Engineering directors said in an internal message that having a Memegen link on profiles “prevents Googlers from sharpening their focus.”

Workers naturally flocked to Memegen to make fun of the decision.

Technology

Trump signs executive order for single national AI regulation framework, limiting power of states

Palantir Technologies CEO Alex Karp attends the Pennsylvania Energy and Innovation Summit on the campus of Carnegie Mellon University in Pittsburgh, Pennsylvania, July 15, 2025.

Andrew Caballero-reynolds | Afp | Getty Images

Palantir expanded its lawsuit against two former employees on Thursday to include the CEO of their new artificial intelligence startup, Percepta AI.

In the suit, Palantir alleged that Percepta CEO and co-founder Hirsh Jain, co-founder Radha Jain, and a third employee, Joanna Cohen, violated their non-solicitation agreements, hiring top talent to create a competitive business.

Palantir and Percepta didn’t immediately respond to CNBC’s request for comment.

The three defendants are accused of attempting to “poach” executives and developers from their former company and “plunder Palantir’s valuable intellectual property.”

Cohen and Radha Jain, who were named in the original lawsuit filed in October, were previously senior engineers at Palantir. Hirsh Jain, an executive responsible for the company’s healthcare portfolio, was added as another defendant in the latest complaint.

Palantir said the defendants were “entrusted” with the company’s “crown jewels,” including source code, customer workflows and proprietary customer engagement strategies.

The former employees “brazenly disregarded their contractual and legal commitments to Palantir and instead chose a path of deception and unjust competition,” the plaintiffs said in the document, which was filed in the U.S. District Court for the Southern District of New York.

Cohen and Radha Jain denied the initial allegations in a November filing, and agreed to stop working for Percepta during the proceedings.

The suit accused Hirsh Jain, who resigned from Palantir in August 2024, of an “aggressive campaign” to recruit other employees to join Percepta, and said the startup has already hired at least 10 former Palantir employees.

An alleged message written by Hirsh Jain in November 2024 read, “I’m down to pillage the best devs at palantir when they’re at their maximum richness.”

The complaint says Rhada Jain wrote another message saying, “God thinking about poaching is so fun.”

Palantir, which was co-founded by Peter Thiel, CEO Alex Karp and others, builds analytics software for companies and government agencies, including the U.S. military. The company’s stock price has soared more than tenfold since the end of 2023, lifting its market cap close to $450 billion.

Palantir also accused Cohen of sending herself highly confidential documents shortly after announcing her resignation from the company in March. Cohen allegedly took photos of sensitive information, the suit said, and downloaded the files onto her personal phone.

“At Percepta, they seek to succeed not through old-fashioned ingenuity and competition, but through outright theft and deceit,” Palantir said in the filing.

Among other things, Palantir is asking for the defendants to be forced to return any confidential information in their possession, and to avoid working at Percepta or venture backer General Catalyst for 12 months from the time of an order.

Technology

Trump ‘sells out’ U.S. national security with Nvidia chip sales to China, Sen. Warren says

Sen. Elizabeth Warren, D-Mass., speaks during a Senate Banking, Housing and Urban Affairs Committee confirmation hearing on President Donald Trump’s nominees to lead the National Economic Council, Consumer Financial Protection Bureau and Federal Housing Finance Agency, on Capitol Hill in Washington, Feb. 27, 2025.

Annabelle Gordon | Reuters

President Donald Trump‘s decision to let Nvidia sell its advanced H200 artificial intelligence chips to China “sells out American national security,” Sen. Elizabeth Warren, D-Mass., said Thursday.

Warren also reiterated her call for Nvidia CEO Jensen Huang to testify before Congress about the agreement, along with Commerce Secretary Howard Lutnick.

The senator’s fiery remarks on the Senate floor came three days after Trump announced on social media that the U.S. semiconductor giant Nvidia could sell the chips to “approved customers” in China, so long as the U.S. gets a 25% cut of the revenues.

The announcement drew concerns both from Democrats and some of Trump’s Republican allies, who have been vocal about protecting America’s hardware advantage over China in the race to AI superiority.

Warren, in Thursday’s remarks, urged Congress to pass bipartisan legislation that “reins in this administration” by imposing new chip export restrictions. Critics of the bill say it could undermine U.S. chipmakers’ competitiveness.

The Trump administration knows that China gaining access to the chips, which have previously been subject to export restrictions, “poses a serious threat to our technological leadership and national security,” Warren said on the Senate floor.

She noted that shortly before Trump announced his decision on the H200 chips on Monday, the Department of Justice touted a crackdown touted a crackdown on a “major China-linked AI tech smuggling network.”

“So why did the President make this bad deal that sells out the American economy and sells out American national security?” she asked. “It’s simple: In the Trump administration, money talks.”

“Mr. Huang understands that in this administration, being able to cozy up to Donald Trump might be the most important corporate CEO skill of all,” Warren said.

She pointed to Huang attending a $1 million-per-plate dinner at Trump’s Florida home Mar-a-Lago, and Nvidia’s later donations to the president’s under-construction White House ballroom.

“Those are just the most obvious possible reasons to cut this deal,” Warren said, “and who knows what else Mr. Huang might have done behind closed doors to persuade President Trump and Secretary Lutnick into making this dangerous concession.”

CNBC has reached out to Nvidia for comment on the senator’s remarks.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024