Surprise fall in retail sales before Christmas signals cost of living gloom

There was a surprise fall in retail sales last month as shoppers remained cautious given the squeeze on budgets from inflation in the run-up to Christmas.

The Office for National Statistics (ONS) reported a fall in sales volumes of 0.3% compared to October when the effects of fuel sales were excluded.

Economists had expected to see growth of 0.3%, given reports of healthy interest, and spending, on goods during the key bargain-hunting period of Black Friday.

But there was a negative performance across the board in every major retail category except for food during the month, suggesting shoppers were keen to eat at home rather than venture out to cafes and restaurants.

The ONS said it likely reflected evidence that many bought Christmas products early to spread the cost.

Non-food store sales volumes fell by 0.6% and were 1.8% below February 2020 levels, it added.

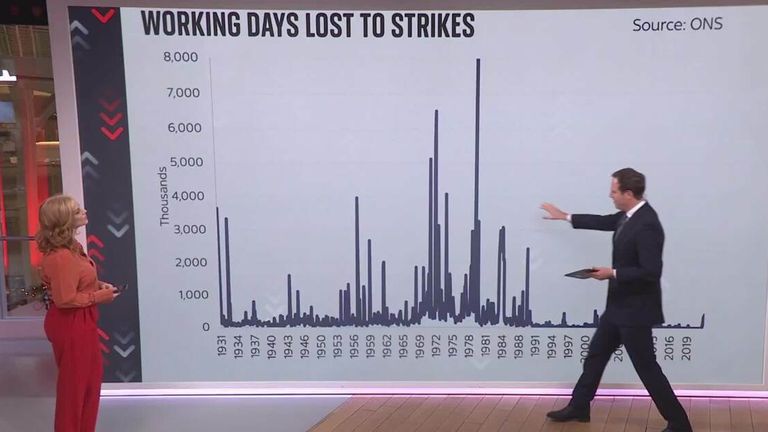

That could also reflect the impact of travel strikes while a 2.8% dip in online sales possibly included a hit from the bitter, continuing, dispute at Royal Mail.

The ONS upwardly revised data covering October when sales bounced back after a hit from the impact of widespread closures for the Queen’s funeral in September.

The number-crunchers recorded month-on-month growth of 0.9% compared to the previous reading of 0.6%.

The latest figures were released against a backdrop of gloom before the festive season, with consumers and businesses alike struggling under the weight of energy-driven inflation.

How will strikes hit the economy?

But while budgets are squeezed by rising bills, hopes were raised earlier this week that inflation had peaked after the core consumer prices index measure eased back in November – led by motor fuel prices.

The Bank of England gave some support to that theory on Thursday after it slowed the pace of interest rate rises, raising Bank rate by 0.5 percentage points following November’s 0.75 percentage point hike.

Andrew Bailey, the governor, pointed to a “glimmer” of hope that the worst was behind us – also expressing hope that the economy was performing a bit better than the Bank had expected.

However, it remains concerned that the country’s tight labour market – high vacancies and few workers to fill gaps – will fuel inflation through high pay rises.

UK inflation hits 10.7%

The issue is also compounded by the wave of public and private sector strikes – mostly over pay – dominating the landscape with unions in many cases seeking increases at least in line with inflation.

The retail sales figures are important as consumer spending accounts for about 80% of the economy.

A closely watched measure of consumer confidence, compiled by GfK, showed a slight improvement this month despite remaining near a record low level.

However, respondents remained concerned about the outlook for their personal finances next year, suggesting a cautionary approach to non-essential spending ahead.

Joe Staton, client strategy director at GfK, said: “Despite the latest GDP figures showing slight growth in October, the warning is of a tough road ahead and that the UK is not out of the recessionary woods.

“Real wages are falling as inflation continues to bite hard, further straining the discretionary budget of many households as we enter the last few shopping days before Christmas.”

Government borrowing last month was the highest in five years, official figures show, exacerbating the challenge facing Chancellor Rachel Reeves.

Not since 2020, in the early days of the COVID pandemic with the furlough scheme ongoing, was the August borrowing figure so high, according to data from the Office for National Statistics (ONS).

Money blog: Borrowers warned of wider market risk

Tax and national insurance receipts were “noticeably” higher than last year, but those rises were offset by higher spending on public services, benefits and interest payments on debt, the ONS said.

It meant there was an £18bn gap between government spending and income, a figure £5.25bn higher than expected by economists polled by Reuters.

A political headache

Also released on Friday were revisions to the previous months’ data.

Borrowing in July was more than first thought and revised up to £2.8bn from £1.1bn previously.

For the financial year as a whole, borrowing to June was revised to £65.8bn from £59.9bn.

State borrowing costs have also risen because borrowing has simply become more expensive for the government. Interest payments rose to £8.4bn in August.

Earlier this month: Why did UK debt just get more expensive?

It compounds the problem for Ms Reeves as she approaches the November budget, and means tax rises could be likely.

Her self-imposed fiscal rules, which she repeatedly said she will stick to, mean she must bring down government debt and balance the budget by 2030.

Read more:

The big story from Bank of England is an easing in tightening to avert massive losses

Next issues scathing attack on UK economy as it reports tens of millions in profit growth

Tax rises?

Ms Reeves will need to find money from somewhere, leading to speculation taxes will increase and spending will be cut.

“Today’s figures suggest the chancellor will need to raise taxes by more than the £20bn we had previously estimated,” said Elliott Jordan-Doak, the senior UK economist at research firm Pantheon Macroeconomics.

“We still expect the chancellor to fill the fiscal hole with a smorgasbord of stealth and sin tax increases, along with some smaller spending cuts.”

Sin taxes are typically applied to tobacco and alcohol. Stealth taxes are ones typically not noticed by taxpayers, such as freezing the tax bands, so wage rises mean people fall into higher brackets.

Increased employers’ national insurance costs and rising wages have meant the tax take was already up.

Responding to the figures, Ms Reeves’s deputy, chief secretary to the Treasury, James Murray, said: “This government has a plan to bring down borrowing because taxpayer money should be spent on the country’s priorities, not on debt interest.

“Our focus is on economic stability, fiscal responsibility, ripping up needless red tape, tearing out waste from our public services, driving forward reforms, and putting more money in working people’s pockets.”

For the most part, when people think about the Bank of England and what it does to control the economy, they think about interest rates.

And that’s quite understandable. After all, influencing inflation by raising or lowering the prevailing borrowing costs across the UK has been the Bank’s main tool for the vast majority of its history. There are data series on interest rates in the Bank’s archives that go all the way back to its foundation in 1694.

But depicting the Bank of England as being mostly about interest rates is no longer entirely true. For one thing, these days it is also in charge of regulating the financial system. And, even more relevant for the wider economy, it is engaged in another policy with enormous consequences – both for the markets and for the public purse. But since this policy is pretty complex, few outside of the financial world are even aware of it.

Money latest: What interest rate hold means for you

That project is quantitative easing (QE) or, as it’s better known these days, quantitative tightening (QT).

You might recall QE from the financial crisis. It was, in short, what the Bank did when interest rates went down to zero and it needed an extra tool to inject some oomph into the economy.

That tool was QE. Essentially it involved creating money (printing it electronically) to buy up assets. The idea was twofold: first, it means you have more money sloshing around the economy – an important concept given the Great Depression of the 1930s had been associated with a sudden shortage of money. Second, it was designed to try to bring down the interest rates prevailing in financial markets – in other words, not the interest rate set by the Bank of England but the yields on long-dated bonds like the ones issued by the government.

Bank of England’s decision in 90 seconds

So the Bank printed a lot of money – hundreds of billions of pounds – and bought hundreds of billions worth of assets. It could theoretically have spent that money on anything: stocks, shares, debt, housing. I calculated a few years ago that with the sums it forked out, it could theoretically have bought every home in Scotland.

Did Oasis cause a spike in inflation?

But the assets it chose to buy were not Scottish homes but government bonds, mostly, it said back at the time (this was 2009) because they were the most available liquid asset out there. That had a couple of profound consequences. The first was that from the very beginning QE was a technical policy most people didn’t entirely understand. It was all happening under the radar in financial markets. No one, save for the banks and funds selling government bonds (gilts, as they’re known) ever saw the money. The second consequence is that we’re starting to reckon with today.

Roll on a decade-and-a-half and the Bank of England had about £895bn worth of bonds sitting on its balance sheet, bought during the various spurts of QE – a couple of spurts during the financial crisis, another in the wake of the EU referendum and more during COVID. Some of those bonds were bought at low prices but, especially during the pandemic, they were bought for far higher prices (or, since the yield on these bonds moves in opposite directions to the price, at lower yields).

Then, three years ago, the Bank began to reverse QE. That meant selling off those bonds. And while it bought many of those bonds at high prices, it has been selling them at low prices. In some cases it has been losing astounding amounts on each sale.

Take the 2061 gilt. It bought a slug of them for £101 a go, and has sold them for £28 a piece. Hence realising a staggering 73% loss.

Tot it all up and you’re talking about losses, as a result of the reversal of QE, of many billions of pounds. At this point it’s worth calibrating your sense of these big numbers. Broadly speaking, £10bn is a lot of money – equivalent to around an extra penny on income tax. The fiscal “black hole” Rachel Reeves is facing at the forthcoming budget is, depending on who you ask, maybe £20bn.

UK long-term borrowing costs hit 27-year high

Well, the total losses expected on the Bank of England’s Quantitative Tightening programme (“tightening” because it’s the opposite of easing) is a whopping £134bn, according to the Office for Budget Responsibility.

Now it’s worth saying first off that, as things stand at least, not all of those losses have been crystallised. But over time it is expected to lose what are, to put it lightly, staggering sums. And they are sums that are being, and will be paid, by British taxpayers in the coming years and decades.

Now, if you’re the Bank of England, you argue that the cost was justifiable given the scale of economic emergency faced in 2008 and onwards. Looking at it purely in terms of fiscal losses is to miss the point, they say, because the alternative was that the Bank didn’t intervene and the UK economy would have faced hideous levels of recession and unemployment in those periods.

However, there’s another, more subtle, critique, voiced recently by economists like Christopher Mahon at Columbia Threadneedle Investments, which is that the Bank has been imprudent in its strategy of selling off these assets. They could, he argues, have sold off these bonds less quickly. They could, for that matter, have been more careful when buying assets not to invest too wholeheartedly in a single class of asset (in this case government bonds) that might be sensitive in future to changes in interest rates.

Most obviously, there are other central banks – most notably the Federal Reserve and European Central Bank – that have refrained from actively selling the bonds in their QE portfolios. And, coincidentally or not, these other central banks have incurred far smaller losses than the Bank of England. Or at least it looks like they have – trying to calculate these things is fiendishly hard.

But there’s another consequence to all of this as well. Because if you’re selling off a load of long-dated government bonds then, all else equal, that would have the tendency to push up the yields on those bonds. And this brings us back to the big issue so many people are fixated with right now: really high gilt yields. And it so happens that the very moment Britain’s long-term gilt yields began to lurch higher than most other central banks was the moment the Bank embarked on quantitative tightening.

But (the plot thickens) that moment was also the precise moment Liz Truss’s mini-budget took place. In other words, it’s very hard to unpick precisely how much of the divergence in British borrowing costs in recent years was down to Liz Truss and how much was down to the Bank of England.

Either way, perhaps by now you see the issue. This incredibly technical and esoteric economic policy might just have had enormous consequences. All of which brings us to the Bank’s decision today. By reducing the rate at which it’s selling those bonds into the market and – equally importantly – reducing the proportion of long-dated (eg 30 year or so) bonds it’s selling, the Bank seems to be tacitly acknowledging (without actually quite acknowledging it formally) that the plan wasn’t working – and it needs to change track.

However, the extent of the change is smaller than many would have hoped for. So questions about whether the Bank’s QT strategy was an expensive mistake are likely to get louder in the coming months.

For the most part, when people think about the Bank of England and what it does to control the economy, they think about interest rates.

And that’s quite understandable. After all, influencing inflation by raising or lowering the prevailing borrowing costs across the UK has been the Bank’s main tool for the vast majority of its history. There are data series on interest rates in the Bank’s archives that go all the way back to its foundation in 1694.

But depicting the Bank of England as being mostly about interest rates is no longer entirely true. For one thing, these days it is also in charge of regulating the financial system. And, even more relevant for the wider economy, it is engaged in another policy with enormous consequences – both for the markets and for the public purse. But since this policy is pretty complex, few outside of the financial world are even aware of it.

Money latest: What interest rate hold means for you

That project is quantitative easing (QE) or, as it’s better known these days, quantitative tightening (QT).

You might recall QE from the financial crisis. It was, in short, what the Bank did when interest rates went down to zero and it needed an extra tool to inject some oomph into the economy.

That tool was QE. Essentially it involved creating money (printing it electronically) to buy up assets. The idea was twofold: first, it means you have more money sloshing around the economy – an important concept given the Great Depression of the 1930s had been associated with a sudden shortage of money. Second, it was designed to try to bring down the interest rates prevailing in financial markets – in other words, not the interest rate set by the Bank of England but the yields on long-dated bonds like the ones issued by the government.

So the Bank printed a lot of money – hundreds of billions of pounds – and bought hundreds of billions worth of assets. It could theoretically have spent that money on anything: stocks, shares, debt, housing. I calculated a few years ago that with the sums it forked out, it could theoretically have bought every home in Scotland.

Did Oasis cause a spike in inflation?

But the assets it chose to buy were not Scottish homes but government bonds, mostly, it said back at the time (this was 2009) because they were the most available liquid asset out there. That had a couple of profound consequences. The first was that from the very beginning QE was a technical policy most people didn’t entirely understand. It was all happening under the radar in financial markets. No one, save for the banks and funds selling government bonds (gilts, as they’re known) ever saw the money. The second consequence is that we’re starting to reckon with today.

Roll on a decade-and-a-half and the Bank of England had about £895bn worth of bonds sitting on its balance sheet, bought during the various spurts of QE – a couple of spurts during the financial crisis, another in the wake of the EU referendum and more during COVID. Some of those bonds were bought at low prices but, especially during the pandemic, they were bought for far higher prices (or, since the yield on these bonds moves in opposite directions to the price, at lower yields).

Then, three years ago, the Bank began to reverse QE. That meant selling off those bonds. And while it bought many of those bonds at high prices, it has been selling them at low prices. In some cases it has been losing astounding amounts on each sale.

Take the 2061 gilt. It bought a slug of them for £101 a go, and has sold them for £28 a piece. Hence realising a staggering 73% loss.

Tot it all up and you’re talking about losses, as a result of the reversal of QE, of many billions of pounds. At this point it’s worth calibrating your sense of these big numbers. Broadly speaking, £10bn is a lot of money – equivalent to around an extra penny on income tax. The fiscal “black hole” Rachel Reeves is facing at the forthcoming budget is, depending on who you ask, maybe £20bn.

UK long-term borrowing costs hit 27-year high

Well, the total losses expected on the Bank of England’s Quantitative Tightening programme (“tightening” because it’s the opposite of easing) is a whopping £134bn, according to the Office for Budget Responsibility.

Now it’s worth saying first off that, as things stand at least, not all of those losses have been crystallised. But over time it is expected to lose what are, to put it lightly, staggering sums. And they are sums that are being, and will be paid, by British taxpayers in the coming years and decades.

Now, if you’re the Bank of England, you argue that the cost was justifiable given the scale of economic emergency faced in 2008 and onwards. Looking at it purely in terms of fiscal losses is to miss the point, they say, because the alternative was that the Bank didn’t intervene and the UK economy would have faced hideous levels of recession and unemployment in those periods.

However, there’s another, more subtle, critique, voiced recently by economists like Christopher Mahon at Columbia Threadneedle Investments, which is that the Bank has been imprudent in its strategy of selling off these assets. They could, he argues, have sold off these bonds less quickly. They could, for that matter, have been more careful when buying assets not to invest too wholeheartedly in a single class of asset (in this case government bonds) that might be sensitive in future to changes in interest rates.

Most obviously, there are other central banks – most notably the Federal Reserve and European Central Bank – that have refrained from actively selling the bonds in their QE portfolios. And, coincidentally or not, these other central banks have incurred far smaller losses than the Bank of England. Or at least it looks like they have – trying to calculate these things is fiendishly hard.

But there’s another consequence to all of this as well. Because if you’re selling off a load of long-dated government bonds then, all else equal, that would have the tendency to push up the yields on those bonds. And this brings us back to the big issue so many people are fixated with right now: really high gilt yields. And it so happens that the very moment Britain’s long-term gilt yields began to lurch higher than most other central banks was the moment the Bank embarked on quantitative tightening.

But (the plot thickens) that moment was also the precise moment Liz Truss’s mini-budget took place. In other words, it’s very hard to unpick precisely how much of the divergence in British borrowing costs in recent years was down to Liz Truss and how much was down to the Bank of England.

Either way, perhaps by now you see the issue. This incredibly technical and esoteric economic policy might just have had enormous consequences. All of which brings us to the Bank’s decision today. By reducing the rate at which it’s selling those bonds into the market and – equally importantly – reducing the proportion of long-dated (eg 30 year or so) bonds it’s selling, the Bank seems to be tacitly acknowledging (without actually quite acknowledging it formally) that the plan wasn’t working – and it needs to change track.

However, the extent of the change is smaller than many would have hoped for. So questions about whether the Bank’s QT strategy was an expensive mistake are likely to get louder in the coming months.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment12 months ago

Environment12 months agoHere are the best electric bikes you can buy at every price level in October 2024