‘Groundhog year’: Cost of living crisis to deepen in 2023 with falling pay and rising bills, warns think tank

The cost of living crisis will deepen next year as people continue to be hit with falling pay, higher taxes and soaring bills, a think tank has warned.

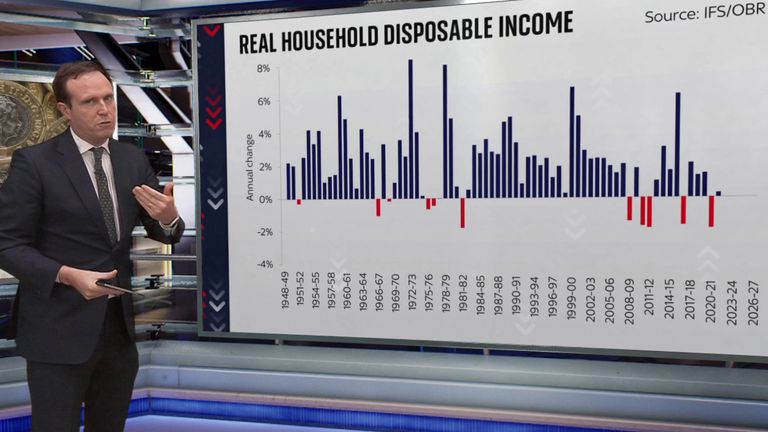

Households face a cost of living “groundhog year” with disposable incomes plummeting even further than in 2022 and living standards getting “far worse” before they improve, according to the Resolution Foundation.

This is due to the continued shrinking of pay packets in real terms, with wages remaining well below current levels of inflation well into 2024.

Although inflation looks set to have peaked, this does not equal lower prices, just smaller price rises, meaning families still face sky-high costs.

Resolution Foundation chief executive Torsten Bell said: “From a cost of living perspective, 2022 was a truly horrendous year – far worse than any year in the pandemic or financial crisis.

“2023 should see the back of double-digit inflation, but it looks set to be a groundhog year for many families whose incomes look set to fall by just as much as they did in 2022.”

Mr Bell said many families will be helped by benefits and the National Living Wage rising, both by around 10% next April.

But he said this will be “swamped by shrinking pay packets, a record £900 rise in energy bills, tax bills for the typical household rising by £1,000, and millions seeing four digit increases in their mortgage bills”.

“For families’ living standards, things will get far worse in 2023 before they start to get better.”

2022 : An economic slowdown

This year saw the biggest annual fall in disposable income in a century as well as a collapse in living standards.

Surging energy prices have been the main driver of the cost of living crisis – mostly a consequence of Russia’s invasion of Ukraine in February that sent the price of many commodities such as wheat, and the price of producing them, through the roof.

But experts have also pointed to trade barriers caused by Brexit and the disastrous mini-budget of the Truss administration.

In his Autumn Statement, Chancellor Jeremy Hunt announced a raft of tax hikes to help fill a £54bn black hole.

The measures will see a typical middle-income household’s personal tax bills jump by around £1,000 from April, according to the Resolution Foundation, which focuses on living standards.

On top of this, household energy spending is set to rise by a record £900 to £2,450 in 2023, up from £1,550 this year.

This is despite wholesale energy prices having dropped, as retail prices continue to climb and government support is scaled back.

Incomes are also being squeezed by rising interest rates, which mean some 2 million households will move onto more expensive fixed-rate mortgages, costing the average mortgage-holder £3,000 more a year.

People are four times as likely to think that their financial situation has worsened than improved over the past year, according to a Resolution Foundation-commissioned YouGov survey of 10,470 adults.

The poll also found that low-income families are three times as likely as high-income families to not feel confident about their financial situation over the next three months.

Read More:

Inflation may have peaked but you should still be prepared for a bleak winter ahead

Millions of adults with health issues are living in cold and damp homes

The analysis comes as the UK braces for further strike action next year, as unions representing many sectors seek pay rises in-line with inflation.

An analysis by the Trade Union Congress suggested that workers have lost £20,000, on average, in real wages since 2008 as a result of pay not keeping up with inflation, and by 2025 the loss will total £24,000.

The government is being urged to negotiate to prevent coordinated industrial action, but on Thursday Defence Secretary Ben Wallace insisted there is “no magic wand” to produce money for the pay demands.

In response to the Resolution Foundation’s report, the Treasury said it has increased child benefit and child tax credits in line with inflation and made changes to Universal Credit “so that working families can keep more of what they earn”.

Click to subscribe to the Sky News Daily wherever you get your podcasts

The spokesperson added: “We also have a plan that will help to more than halve inflation next year, bearing down on the financial pressures that households face, and have already lifted millions of people out of paying tax altogether by raising the tax-free allowances for both income tax and National insurance by more than inflation since 2010.

“This is on top of substantial support with the cost of living, with everyone benefiting from energy bills being held down this winter and more than eight million vulnerable households having already received £1,200 in cash payments straight to their bank accounts – with a further £900 for those on means-tested benefits next year.”

Retail sales rose a surprising amount in July, as good weather and the Women’s Euros led people to part with their cash, official figures show.

The amount of spending rose 0.6% in July, according to figures from the Office for National Statistics (ONS), far above the 0.2% rise anticipated by economists polled by Reuters.

In particular, clothing and footwear stores, as well as online shopping, experienced strong growth.

Money blog: UK airport ranked worst for fourth year in a row

When looked at on a three-month basis, the numbers are weaker, with a 0.6% fall in sales up to July due in part to downward revisions in June.

Spending has declined since March, when supermarkets, sports shops, and household goods saw strong sales at the beginning of the year as warm and sunny weather pushed summer purchases earlier. Though compared to a year ago, sales are up 1.1%.

Fans gather during a Homecoming Victory Parade in London after England’s win in the final of the Women’s Euros. Pic: PA

Retail sales figures are significant as they measure household consumption, the largest expenditure in the UK economy.

Growing retail sales can mean economic growth, which the government has repeatedly said is its top priority.

A problem with the figures

These figures were originally due to be published in August but were delayed by two weeks so the ONS could carry out “quality assurance” checks.

Following the checks, the statistics body found a “problem”, which meant it had to correct seasonally adjusted figures.

It hasn’t been the only question mark over the reliability of ONS figures.

In March, UK trade figures were delayed due to errors from 2023, and the office continues to advise caution in interpreting changes in the monthly unemployment rate due to concerns over data reliability.

UK growth slowed amid rising costs in June.

As a result of the latest error, previously monthly figures overstated the monthly volatility in the first five months of 2025, the ONS’s director general of economic statistics, James Benford, said.

Mr Benford apologised for the release delay and for the errors.

What could it mean?

It could mean retrospective changes to the UK economic growth rate, according to Rob Wood, the chief UK economist at Pantheon Macroeconomics.

Read more:

Firms cut jobs at fastest pace since 2021, Bank of England data shows

More than a quarter of cars sold in August were electric vehicles

April’s economic growth rate will be revised down, and May’s will be moved up as a result, Mr Wood said.

There will be no impact on the Bank of England’s interest rate decision, he added.

A greater proportion of electric cars were sold last month than at any point this year, industry data shows.

More than a quarter (26.5%) of cars sold in August were electric vehicles (EVs), according to figures from motor lobby group the Society for Motor Manufacturers and Traders (SMMT).

It’s the largest amount of sales since December 2024 and comes as the government introduced financial incentives to help drivers make the move to zero tailpipe emission cars.

Money blog: KFC rival coming to UK

The full suite of grants were not available during the month, however, with a further 35 models eligible for £1,500 off early in September.

Throughout August more models became eligible for price reductions, meaning more consumers could be tempted to purchase an EV in September.

New EV grants to drive sales came into effect in July

The increased percentage of EV sales came despite an overall 2% drop in buying, compared to a year earlier, in what is typically the quietest month for car purchases.

What are the rules?

The numbers suggest the car industry could be on course to meet the government’s zero-emission vehicle (ZEV) mandate, the thinktank Energy & Climate Intelligence Unit (ECIU) has said.

It stipulates that new petrol and diesel cars may not be sold from 2030.

Read more:

Bank lobby chief warns Reeves over budget tax raid

Tax the rich to thwart Reform, TUC chief urges Labour

Amid pressure from industry, the government altered the mandate in April to allow for hybrid vehicles, which are powered by both fuel and a battery, to be sold until 2035.

Sales of new petrol and diesel vans are also permitted until 2035.

Until then, 28% of cars sold must be electric this year, with the share rising to 33% in 2026, 38% in 2027 and 66% in 2029, the final year before the new combustion engine ban.

Manufacturers face fines for not meeting the targets.

Last year, the objective of making 22% of all car sales purely EVs was surpassed, with EVs comprising 24.3% of the total sold in 2024.

Why?

The increased portion of EV sales can be attributed to increased model choice and discounting, on top of the government reductions, the SMMT said.

Savings from running an electric car are also enticing motorists, the ECIU said. “Demand for used EVs is already surging because they can offer £1,600 a year in savings in owning and running costs.”

“This matters for regular families as the pipeline of second-hand EVs is dependent on new car sales, which hit the used market after around three to four years.

Businesses have cut jobs at the fastest pace in almost four years, according to a closely-watched Bank of England survey which also paints a worrying picture for employment and wage growth ahead.

Its Decision Maker Panel (DMP) data, taken from chief financial officers across 2,000 companies, showed employment levels over the three months to August were 0.5% lower than in the same period a year earlier.

It amounted to the worst decline since autumn 2021 as firms grappled with the implementation of budget measures in the spring that raised their national insurance contributions and minimum wage levels, along with business rates for many.

Money latest: Eight supermarkets ranked for price

The start of April also witnessed the escalation in Donald Trump’s global trade war which further damaged sentiment, especially among exporters to the United States.

The survey showed no improvement in hiring intentions in the tough economy, with companies expecting to reduce employment levels by 0.5% over the coming year.

That was the weakest outlook projection since October 2020.

At the same time, the panel also showed that participants planned to raise their own prices by 3.8% over the next 12 months. That is in line with the current rate of inflation.

The news on wages was no better as the central forecast was for an average rise of 3.6% – down from the 4.6% seen over the past 12 months.

If borne out, it would mean private sector wages rising below the rate of inflation – erasing household and business spending power.

The Bank of England has been relying on data such as the DMP amid a lack of confidence in official employment figures produced by the Office for National Statistics due to low response rates.

August: Tax rises playing ’50:50′ role in rising inflation

Bank governor Andrew Bailey told a committee of MPs on Wednesday that he was now less sure over the pace of interest rate cuts ahead owing to stubborn inflation in the economy.

The consumer prices index measure is expected to peak at 4% next month – double the Bank’s target rate – from the current level.

Higher interest rates only add to company costs and make them less likely to borrow for investment purposes.

At the same time, employers are fearful that the coming budget, set for late November, may contain no relief.

Why aren’t we hearing about the budget ‘black hole’?

Sky News revealed on Thursday how the head of the banking sector’s main lobby group had written to the chancellor to warn that any additional levy on bank profits, as suggested by a think-tank last week, would only damage her search for growth.

Rachel Reeves is believed to be facing a black hole in the public finances amounting to £20bn-£40bn.

Tax rises are believed to be inevitable, given her commitment to fiscal rules concerning borrowing by the end of the parliament.

Heightened costs associated with servicing such debts following recent bond sell-offs across Western economies have made more borrowing even less palatable.

Why did UK debt just get more expensive?

Ms Reeves is expected to raise some form of wealth tax, while other speculation has included a shake-up of council tax.

She has consistently committed not to target working people but the Bank of England data, and official ONS figures, would suggest that businesses have responded to 2024 budget measures by cutting jobs since April, with hospitality and retail among the worst hit.

Commenting on the data, Rob Wood, chief UK economist at Pantheon Macroeconomics, said: “The DMP survey shows stubborn wage and price pressures despite falling employment, continuing to suggest that structural economic changes and supply weakness are keeping inflation high.

“The MPC [monetary policy committee of the Bank of England] will have to be cautious, so we remain comfortable assuming no more rate cuts this year.”

“That said, the increasing signs of labour market weakness suggest dovish risks,” he concluded.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment11 months ago

Environment11 months agoHere are the best electric bikes you can buy at every price level in October 2024