These stocks were our best and worst performers in the fourth quarter

")

Can an EV really help power your home when the power goes out? It’s one of the biggest FAQs people have about electric cars — but the answer can be a bit confusing. It’s either a yes, with a but – or a no, with an unless. To find out which EVs can offer vehicle-to-home (V2H) tech to keep the lights on or even lower your energy bills, keep on reading.

Modern EVs have big, efficient batteries capable of storing enough energy to power home for days. That can mean backup power during a storm or the ability to use stored energy during expensive peak hours and recharge again when kilowatts are cheap.

That’s all true – but only in theory. Because, while your EV might have a big battery, that doesn’t mean it has the special hardware and software that allow electricity to safely flow back out of the car baked in. Car companies call this vehicle-to-home (V2H) or bi-directional charging, and only a handful of models currently support it. That’s that, “yes, with a but” asterisk.

Yes, an EV can power your home, but it has to be one of these.

Ford F-150 Lightning

Ford made early headlines using its F-150 Lightning as a life-saving generator during winter ice storms and hurricanes, so it should come as no surprise that it’s included in this list. The best-selling electric truck in America can send up to 9.6 kW of power from its onboard batteries back to the house. More than enough to keep the lights on and the refrigerator running during an outage.

To make it work, you’ll need to install the Charge Station Pro (formerly called Intelligent Backup Power) home charger, the Home Integration System (HIS), which includes an inverter, a transfer switch, and a small battery to switch the system on, as well Ford’s Charge Station Pro 80A bi-directional charger (which comes free with the Extended Range F-150 Lightning, but costs about $1,300 otherwise).

All-in, you’re looking at about $5,000 in hardware, plus installation, to make it work.

Kia EV9

With up to 300 miles of range and ultra-fast charging, the seven-passenger electric SUV from Kia has been a hot seller. And back in March, the Kia EV9 unlocked yet another new feature: vehicle-to-home charging.

When paired with the Quasar 2 bidirectional charger from Wallbox (and the associated Power Recovery Unit, or PRU), a fully-charged Kia EV9 can power a standard suburban home for three days. Longer, still, if you’re keeping the energy use low. The Wallbox Quasar 2 isn’t cheap, though – pricing starts at $6,440 (again, plus installation). For that price, you the PRU plus a wall-mounted 12 kW L2 charger with 12.8 kW of with discharge power on a split-phase system.

Pretty much all the GM EVs

With the exception of the Chevy Brightdrop, GMC Hummer EV, and the hand-built, ultra-luxe Cadillac CELESTIQ, every Ultium-based GM EV can send battery power back to your home through GM Energy’s Ultium Home System – arguably the most fully integrated EV + battery backup + solar option out there outside of Tesla.

GM Energy says its new 19.2 kW Powershift Charger delivers around 6-7% more juice than a typical 11.5 kW L2 charger, delivering up to 51 miles of range per charge hour. Bi-directional charging requires the Powershift Charger to be paired up with a compatible GM EV and the GM Energy V2H Enablement Kit. The full system retails for $12,699, plus installation, and can be financed through GM Financial.

NOTE: some 2024 models might require a software update to enable V2H functionality, which can be done either at the dealer or through an OTA update.

Tesla Cybertruck

Tesla Cybertruck owners may have zero taste, but they have two options when it comes to powering their homes with their trucks. If they already have a Tesla Powerwall, they don’t need anything else. If they don’t, they’ll need to install a Universal Wall Connector charger, a Powershare Gateway, and a Tesla Backup Switch.

That second option will run about $3,500, plus installation.

That rounds off the list of vehicles that ship with V2H software baked in, so if you’re wondering whether or not your EV can be used to power your home, now you know the answer is yes, as long as it’s one of the ones listed above.

But you might remember that I answered the initial question by saying it was either a yes, with a but – or a no, with an unless. So if you want to use your car’s battery as a backup, but don’t have one of the EVs liksted above, that doesn’t mean you’re completely out of luck.

No, with an unless

As some of the earliest and most enthusiastic EV adopters, Tesla fans have also been among the loudest advocates for using the energy stored their cars’ batteries to back up their homes — or even the grid itself. Unfortunately for them, the slow-selling Cybertruck is the only Tesla vehicle that officially supports bi-directional charging. If you’re one of the many Model 3 and Y owners frustrated by those delays, there’s good news: those vehicles are now capable of V2H charging thanks to an “impressive” Powerwall competitor, Sigenergy.

The good news doesn’t stop there, however. The Sigenergy V2X also works with both the popular Kia EV6 and Electrek‘s 2024 EV of the Year, the Volvo EX30 over the DIN70121 protocol, and several VW/Audi/Porsche and Mercedes-Benz EVs over the ISO15118-2 protocol.

Our own Editor-in-Chief, Fred Lambert, recently went on a Sigenergy deep dive with Sylvain Juteau, President of Roulez Electrique, and came away deeply impressed with the system. I’ve included the video, above, and you can read more about the system itself at this link.

And, of course, I look forward to learning about any V2H models or more universal battery backup systems from you, the smartest readers in the blogosphere, in the comments.

Original content from Electrek.

If you’re considering going solar, it’s always a good idea to get quotes from a few installers. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

Tesla has changed the meaning of “Full Self-Driving”, also known as “FSD”, to give up on its original promise of delivering unsupervised autonomy.

Since 2016, Tesla has claimed that all its vehicles in production would be capable of achieving unsupervised self-driving capability.

CEO Elon Musk has claimed that it would happen by the end of every year since 2018.

Tesla has even sold a software package, known as “Full Self-Driving Capability” (FSD), for up to $15,000 to customers, promising that the advanced driver-assist system would become fully autonomous through over-the-air software updates.

Almost a decade later, the promise has yet to be fulfilled, and Tesla has already confirmed that all vehicles produced between 2016 and 2023 don’t have the proper hardware to deliver unsupervised self-driving as promised.

Musk has been discussing the upgrade of the computers in these vehicles to appease owners, but there’s no concrete plan to implement it.

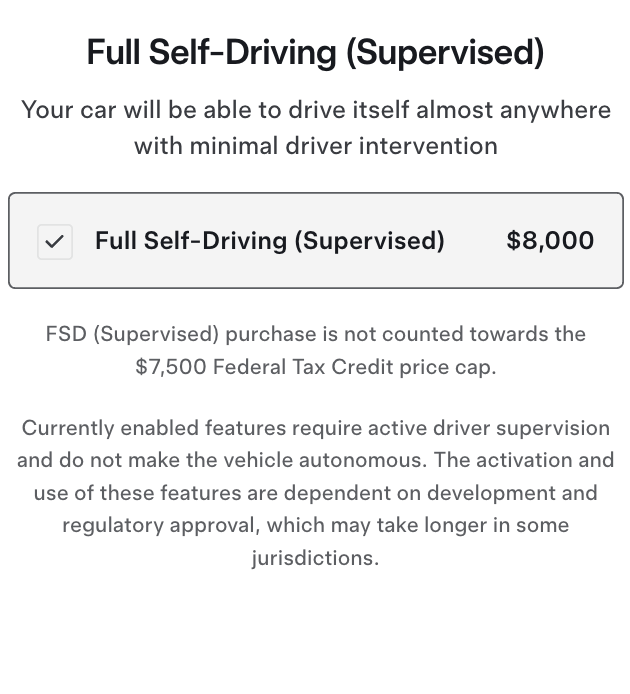

While there’s no doubt that Tesla has promised unsupervised self-driving capabilities to FSD buyers between 2016 and 2023, the automaker has since updated its language and now only sells “Full Self-Driving (Supervised)” to customers:

The fine print mentions that it doesn’t make the vehicle “autonomous” and doesn’t promise it as a feature.

In other words, people buying FSD today are not really buying the capability of unsupervised self-driving as prior buyers did.

Furthermore, Tesla’s board has just submitted a new, unprecedented CEO compensation package for shareholders’ approval, which could give Musk up to $1 trillion in stock options pending the achievement of certain milestones.

One of these milestones is Tesla having “10 Million Active FSD Subscriptions.”

At first glance, this would be hopeful for FSD buyers since part of Musk’s compensation would be dependent on delivering on the FSD promises.

However, Tesla has changed the definition of FSD in the compensation package with an extremely vague one”

“FSD” means an advanced driving system, regardless of the marketing name used, that is capable of performing transportation tasks that provide autonomous or similar functionality under specified driving conditions.

Tesla now considers FSD only an “advanced driving system” that should be “capable of performing transportation tasks that prove autonomous or similar functionality”.

The current version of FSD, which requires constant supervising by the driver, could easily fit that description.

Therefore, FSD now doesn’t come with the inital promise of Tesla owners being able to go to sleep in their vehicles and wake up at their destination – a promise that Musk has used to sell Tesla vehicles for years.

Electrek’s Take

The way Tesla discusses autonomy with customers and investors versus how it presents it in its court filings and legally binding documents is strikingly different.

It should be worrying to anyone with an interest in this.

With this very vague description in the new CEO compensation package, Tesla could literally lower the price of FSD and even remove base Autopilot to push customers toward FSD and give Musk hundreds of billions of dollars in shares in the process.

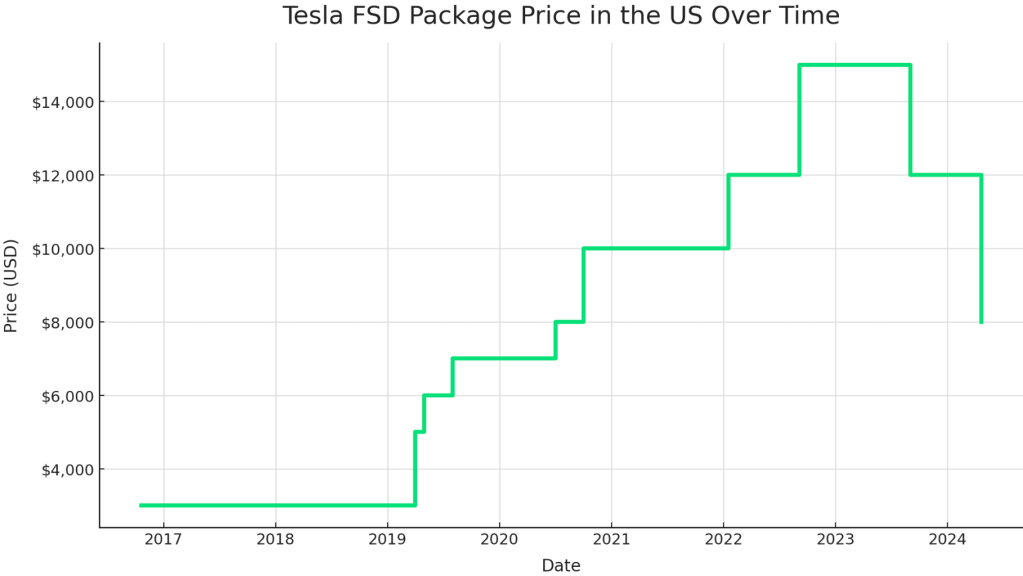

There’s precedent for Tesla decreasing pricing on FSD. Initially, Musk said that Tesla would gradually increase the price of the FSD package as the features improved and approached unsupervised autonomy.

That was true for a while, but then Tesla started slashing FSD prices, which are now down $7,000 from their high in 2023:

The trend is quite apparent and coincidentally began when Tesla’s sales started to decline.

FSD is now a simple ADAS system without any promise of unsupervised self-driving. This might quite honestly be one of the biggest cases of false advertising or bait-and-switch ever.

FTC: We use income earning auto affiliate links. More.

The new Chevy Bolt EV is set to enter production later this year, with one fewer shift, following GM’s reduction in production plans at several US plants. Apart from the Bolt, GM promised a new family of affordable EVs. Are those, too, now at risk?

GM says more affordable EVs are coming, but when?

GM remained the number two EV maker in the US after back-to-back record sales months in July and August. However, with the $7,500 federal tax credit set to expire at the end of the month, the company expects a slowdown.

On Thursday, GM sent a note to employees at its Spring Hill plant in Tennessee, outlining plans to reduce output of two Cadillac electric SUVs, the Lyriq and Vistiq.

A source close to the matter confirmed the news to Reuters, saying the production halt will begin in December. GM will significantly reduce output during the first five months of 2026, according to the source.

GM is also delaying the second shift at its Fairfax Assembly Plant in Kansas City, where the new Chevy Bolt is slated to enter production later this year. The Bolt will be the first of a new series of affordable EVs that GM intends to build in Kansas.

However, those too, may now be in jeopardy. According to local news outlets, GM Korea Technical Research Center (GMTCK), a spin-off of GM’s Korean subsidiary, was recently cut out of a secret small EV project it was developing.

GMTCK president Brian McMurray reportedly announced internally last month during a trip to the US that the project was cancelled and only 30% to 40% complete.

A GM Korea spokesperson clarified that “the EV project being led by GMTCK was a global undertaking, not undertaken solely by GM Korea. The spokesperson added, “The project itself has not been canceled; the role of the Korean team has simply changed.”

The new electric car, dubbed “Fun Family,” was scheduled to launch under the Chevy and Buick brands, using a single platform. Production was expected to begin in 2027 with deliveries starting in 2028.

GM Korea exports over 90% of the vehicles it makes to the US, but with the new auto tariffs, the subsidiary is expected to play a drastically smaller role, if any at all. The news is fueling the ongoing rumors that GM could withdraw from Korea altogether.

In addition to the tariffs, South Korea’s recently passed “Yellow Envelope Law” could make it even more difficult for GM with new labor laws.

Will this impact the affordable EVs GM is promising to launch in the US? They are scheduled to be built in Kansas, but with the R&D Center, GM’s second largest globally, following the US, claiming to be excluded from a major global EV project, it can’t be a good sign.

In the meantime, GM already has one of the most affordable electric vehicles in the US, the Chevy Equinox EV. Starting at under $35,000, the company calls it “America’s most affordable” EV with over 315 miles of range.

With the $7,500 federal tax credit still available, GM is promoting Chevy Equinox EV leases for under $250 a month. Nowadays, it’s hard to find any vehicle for under that.

Source: Newsworks Korea

FTC: We use income earning auto affiliate links. More.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment11 months ago

Environment11 months agoHere are the best electric bikes you can buy at every price level in October 2024