Ministers ask Hunt for £300m to avert mass British Steel job losses

Ministers are urging the chancellor to provide £300m of taxpayers’ money to avert the closure of British Steel’s two blast furnaces – a move that would trigger the loss of thousands of industrial jobs in northern England.

Sky News has learnt that Grant Shapps, the business secretary, and Michael Gove, the levelling-up secretary, wrote to Jeremy Hunt this month to warn that the demise of British Steel could cost the government up to £1bn in decommissioning and other liabilities.

In their letter, a copy of which has been seen by Sky News, Mr Hunt was asked to consider the economic case for supporting both British Steel, which is owned by a Chinese conglomerate, and the wider UK steel industry.

“Every other G20 nation has maintained domestic steel production and, while we do not think that this should come at any cost, we do believe it is in HMG’s interest to offer well-designed and targeted funding which unlocks private investment, achieves a good outcome for taxpayers, and enables transformed, decarbonised and viable domestic steel production to continue in the UK in the long-term,” Mr Shapps and Mr Gove wrote.

“We do not want to become reliant on steel sources elsewhere in the same way that energy security has become self-evidently important.

“Moreover, our steel requirement will increase by 20% due to large domestic infrastructure projects already committed to in the UK.”

One industry source briefed on the discussions in Whitehall said the chancellor had instructed Treasury officials to scrutinise the request.

The letter to Mr Hunt warned that British Steel “does not have a viable business without government support”.

The British Steel plant in Scunthorpe

“Closing one blast furnace would be a stepping-stone to closure of the second blast furnace, resulting in a highly unstable business model dependent on Chinese steel imports,” Mr Shapps and Mr Gove wrote.

“The local economic impact of closing both blast furnaces is estimated to be in the region of £360m to £640m, with a further £500m to £1bn liability for HMG through compulsory liquidation, insolvency and land liabilities (though £40m could potentially be raised through asset recovery”.

“Given the magnitude of the liabilities due to fall on HMG in the event of blast furnace closure, and following the PM’s steer, we would like officials to test whether net government support in the region of £300m for British Steel could prevent closure, protect jobs and create a cleaner viable long-term future for steel production in the United Kingdom.”

The fate of British Steel, which was bought by Jingye Group out of a previous insolvency process less than three years ago, has become increasingly unclear in recent months as the current owners have indicated that they would not maintain its operations without taxpayer funding.

British Steel employs about 4,000 people, with thousands more jobs in its supply chain dependent upon the company.

According to the letter to Mr Hunt, British Steel has already informed the government that it could close one of the Scunthorpe blast furnaces as soon as next month, with the loss of 1,700 jobs.

This would be “followed by the second blast furnace closing later in 2023, creating cumulative direct job losses of around 3,000”, Mr Shapps and Mr Gove wrote.

The plea to Mr Hunt followed a round of talks between Mr Shapps and Jingye earlier in December about supporting Britain’s second-largest steel producer.

Mr Shapps’ predecessor, Jacob Rees-Mogg – who lasted just weeks as business secretary under Liz Truss – opened formal talks with Jingye in October about the provision of government funding to help British Steel decarbonise.

One of the pre-conditions set by Whitehall for the discussions was that Jingye would not cut jobs at British Steel while the discussions were ongoing, although the recent letter to Mr Hunt said that ministers “cannot guarantee the company will choose to support jobs in the short term”.

Tata Steel, which is the biggest player in the UK steel sector, has also requested financial help from the government.

Responding to an enquiry from Sky News, a government spokesman said: “The government is committed to securing a sustainable and competitive future for the UK steel sector and we are working closely with industry to achieve this.

“We recognise that businesses are feeling the impact of high global energy prices, including steel producers, which is why we announced the Energy Bill Relief Scheme to bring down costs.

“This is in addition to extensive support we have provided to the steel sector as a whole to help with energy costs, worth more than £800m since 2013.”

The request for financial support from Jingye poses a political headache for ministers, given the scale of the potential job losses which might result from a refusal to provide taxpayer aid.

An agreement to provide substantial taxpayer funding to a Chinese-owned business, however, would inevitably provoke outrage among Tory critics of Beijing.

China’s role in global steel production, after years of international trade rows about dumping, would make any subsidies even more contentious.

In May 2019, the Official Receiver was appointed to take control of the company after negotiations over an emergency £30m government loan fell apart.

British Steel had been formed in 2016 when India’s Tata Steel sold the business for £1 to Greybull Capital, an investment firm.

As part of the deal that secured ownership of British Steel for Jingye, the Chinese group said it would invest £1.2bn in modernising the business during the following decade.

Jingye’s purchase of the company, which completed in the spring of 2020, was hailed by Boris Johnson, the then prime minister, as assuring the future of steel production in Britain’s industrial heartlands.

British Steel has previously said of its negotiations with Whitehall: “We are continuing formal talks with the UK Government to help us overcome the global challenges we currently face.

“The government understands the significant impact the economic slowdown, rising inflation and exceptionally high energy and carbon prices are having on businesses like ours and we look forward to working together to build a sustainable future.”

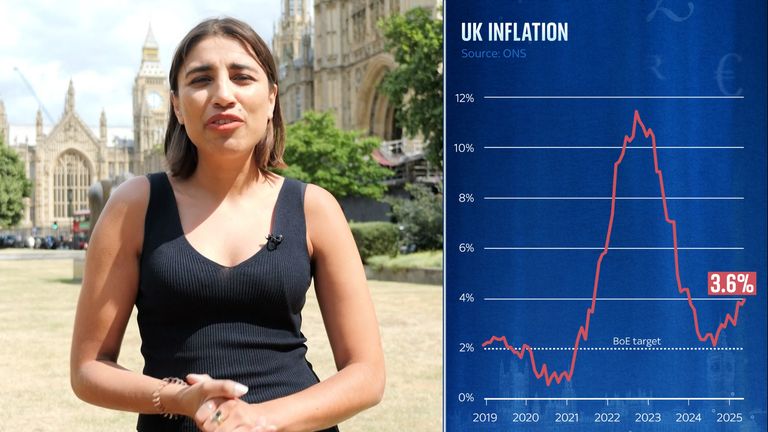

Retail sales grew in June as warm weather boosted spending and day trips, official figures show.

Spending on goods such as food, clothes and household items rose 0.9%, the Office for National Statistics (ONS) said.

It’s a bounce back from the 2.8% dip in May, but last month’s figure was below economists’ forecast 1.2% uplift as consumers dealt with higher prices from increased inflation.

Money blog: The odd rules that could land you with a big fine on holiday

Also weighing on spending was reduced consumer confidence amid talk of higher taxes, according to a closely watched indicator from market research firm GfK.

Retail sales figures are significant as they measure household consumption, the largest expenditure in the UK economy.

Growing retail sales can mean economic growth, which the government has repeatedly said is its top priority.

What does ‘inflation is rising’ mean?

Where have people been shopping?

June’s retail sales rise came as people bought more in supermarkets, and retailers said drinks sales were up.

While hot and sunny weather boosted some brick-and-mortar shops, the heat led some to head online.

Read more from Money:

Satellite tracker Spaceflux reaches lift-off with £5m funding boost

Trade war uncertainty prompts halt to eurozone rate cuts

Non-store retailers, which include mainly online shops, but also market stalls, had sold the most in more than three years.

Not since February 2022 had sales been so high as the Met Office said England had its warmest ever June, and the second warmest for the UK as a whole.

The June increases suggest that the May drop was a bump in the road. When looked at as a whole, the first six months of the year saw retail sales up 1.7%.

Filling up the car for day trips to take advantage of the sun played an important role in the retail sales growth.

When fuel is excluded, the rise was smaller, just 0.6%.

Welcome news

Despite lower consumer sentiment and more expensive goods, consumers are benefitting from rising wages and are cutting back on savings.

The ONS lifestyle survey – backed up by hard data like the Bank of England’s money and credit figures – shows that households have rebuilt their rainy day savings and are cutting back on the amount of money they squirrel away each month.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike