Westminster Accounts: Middlemen, brokers, and clients – who really pays MPs for their other jobs?

Thirty-eight MPs have taken on second jobs where the ultimate party paying them is unclear, according to Sky News’ analysis of the MPs’ Register of Financial Interests.

The jobs mainly involve MPs being paid through a broker – a consultancy business, a communications firm, or a speakers’ bureau – while not declaring the clients they are working for.

It casts doubt on the systems which are supposed to ensure transparency around MPs’ earnings.

The analysis was conducted as part of the Westminster Accounts – a Sky News and Tortoise Media project that aims to shine a light on money in UK politics.

But this light has made the remaining shadows all the more stark.

Read more:

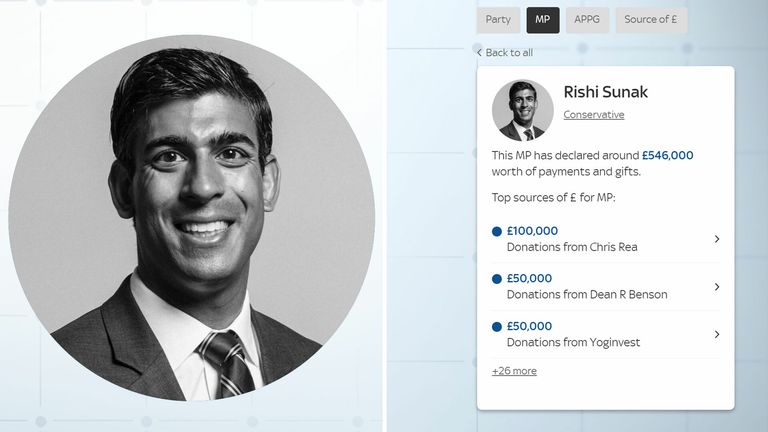

Search for your MP

Why the Westminster Accounts matter

Ex-cabinet minister Sir John Whittingdale provides one of the clearest examples of these cases, but two current ministers – Andrew Mitchell and Johnny Mercer – also appear to fall into this category. Some MPs told Sky News they had signed contracts restricting them from being transparent about the clients they’d worked with.

It begs the question of who is really influencing UK politicians, with Transparency International saying the findings could suggest there’s a “culture of opacity” among some MPs.

MPs are supposed to give details about their non-parliamentary earnings in the Register of Members’ Financial Interests.

On the face of it, that is what Sir John has done.

He’s a former culture secretary and a long-serving MP with a wealth of political experience. He’s been offering his insight, as MPs are entitled to do, via a company called AlphaSights, which connects experts like him with its clients.

But it remains unknown who the clients Sir John spoke to are.

Sam Coates explains how and why the Westminster Accounts tool was made

He’s reported in his public filings that he’s received more than £10,500 from AlphaSights to tap into his expertise across 17 different engagements.

He was quizzed earlier this year on two of these dealings by the Advisory Committee on Business Appointments (ACOBA), the watchdog overseeing ex-ministers’ jobs, after he failed to seek approval for this work from the committee.

He was deemed not to have broken any rules, however, as he told the chair of ACOBA that he had no long-term relationship with AlphaSights and they were separate “one-off” speeches he delivered. Prior approval is not necessary for one-off speeches.

However, this seems hard to reconcile with the fact that Sir John has had 15 other engagements with AlphaSights since 2017, as the Westminster Accounts help reveal. And an ex-AlphaSights employee has told Sky News that rather than “speeches”, the work typically involves attending a meeting or having a call with two or three people from the client company.

These clients, who pay a fee for the privilege, are usually investment firms and consultancies looking for insight from experts to help make business decisions.

Sir John did not respond to questions from Sky News regarding who these clients were.

Read more:

Westminster Accounts: Following the money

How to explore the database for yourself

It is a clear example where the companies paying to contract an MP’s services, and the company reported publicly in the Register of Interests – AlphaSights in this case – differ.

Sir John’s case is just one of many where these questions apply.

Defence minister Mr Mercer, for example, declared payments of £3,600 and £1,110 in 2021 for two speaking engagements from Chartwell Speakers, a speaker agency.

No details are given in the register as to who the clients acting through the agency were, as MPs are usually expected to report in these instances.

Beyond speeches and individual engagements, there is a wider group of 11 MPs who are on the books of communications or political consultancies who often don’t give details about the clients they work with.

MPs’ second jobs – what are the rules?

International development minister Mr Mitchell, for example, had been working as an advisor to Montrose Associates until last October, when he returned to government as a minister.

Montrose Associates is a strategic consultancy which, according to its website, draws on “access to privileged networks of decision-makers” when advising its clients.

Mr Mitchell received more than £340,000 for around 75 days of work since taking up the role in 2013. Exactly which clients he worked with and what he did cannot be known from the cursory description of his work given in the Register of Interests.

This lack of transparency creates particular problems for holding ex-ministers to account. They often undertake new roles on the condition they refrain from lobbying government on behalf of clients of their employers.

Tracey Crouch, another former minister, received approval from ACOBA to become a senior advisor to communications firm The Playbook between February 2018 and March 2020. Her role was to advise some of The Playbook’s clients in the technology and energy sector.

But who these clients were has not been reported in the public record. This was despite ACOBA advising Ms Crouch she couldn’t lobby on behalf of The Playbook’s clients for two years after leaving government.

There is no suggestion Ms Crouch – or any other MP – has broken lobbying rules. But Steve Goodrich, head of research and investigations at Transparency International UK, has cast doubt on the systems designed to ensure politicians aren’t being unduly influenced.

“ACOBA is a paper tiger – it has no teeth, no ability to enforce the advice that it gives,” he said.

“And there’s a broader question about whether these omissions reflect a wider culture of opacity within parliament, at least among some members, that needs challenging. That’s more of a cultural issue, which may be harder to shift.”

How you can explore the Westminster Accounts

There is also another group of MPs who have financial interests that may not be apparent from public disclosures.

Ten MPs have had employment with investment or private equity funds where there is a reasonable expectation they will be advising or making investment decisions about firms within the portfolios of these parent companies.

Yet the current rules – or the enforcement around them – put little onus on MPs to report these details.

David Davis, for example, the former Brexit secretary, sits on the advisory board of THI Holdings GmbH, an investment firm that declares holdings in seven companies on its website.

One of these companies is Oxford International Education Group – where Conservative MP Chris Skidmore sits on the advisory board. Were Mr Skidmore to speak in parliament on higher education issues, he would be expected to draw attention to his financial interest in this area.

But from what Mr Davis has disclosed, it is far more difficult to understand how ACOBA’s advice – which stated that Mr Davis should not lobby on behalf of THI’s subsidiaries in the two years after leaving government in 2019 – could be easily enforced.

Mr Davis is far from alone in working for one of these firms. Andrew Mitchell, Johnathan Djanogly, Richard Fuller, Bim Afolami, Alun Cairns and Stephen McPartland have all had positions with boutique investment firms in the past three years. There is no suggestion these MPs have broken any rules.

A spokesperson for Mr Mitchell told Sky News that all his outside business interests have always been properly registered in the normal way. Mr Mercer, Ms Crouch, and Mr Davis did not respond when asked for comment.

‘We all welcome transparency’

MPs more likely to ask questions in parliament after taking up jobs in finance

Recent research from Dr Simon Weschle, author of Money In Politics, shows that MPs in certain types of second jobs behave differently.

He found that MPs were more likely to ask questions in parliament after taking up jobs in finance or the legal profession.

Dr Weschle said the lack of detail disclosed around these jobs makes it difficult to know if this amounts to lobbying, which would break the rules.

He said: “They could be asking more questions for a number of other reasons or for a reason directly relating to their work… but because we don’t know who they’re advising, who they have holdings in – who they’re ultimately working for – it’s really hard to make that connection.”

One reason MPs may not disclose further details is if doing so may conflict with professional practices.

Ten current MPs, for example, have worked as lawyers and accountants this parliament without naming their clients. Some may feel it inappropriate to disclose the firms or individuals contracting their services.

Click to subscribe to the Sky News Daily wherever you get your podcasts

Labour leader Sir Keir Starmer, for instance, is one MP who has reported payments for giving legal advice with little detail offered as to the source of these funds. Sir Geoffrey Cox, who has earned more than £2m in legal fees this parliament, is another who provides details of the chambers who pay him, but rarely his clients.

Sky News understands there are no professional standards rules in the legal or accountancy profession that would stop MPs disclosing their clients, unless they expressly requested anonymity.

Some MPs involved in business consulting have told Sky News they have signed contracts that prevent them from naming clients publicly.

Yet if these obligations are sometimes the reason for a lack of disclosure, it calls into question the rules which at times seem to put MPs’ private interests above the transparency of the system. In some places, like the US, this problem has been solved by banning politicians from having second jobs.

Dr Weschle thinks there’s room for reform in the UK: “It seems to be that second jobs clearly undermine the public’s trust in politicians… so we should think about whether certain kinds of jobs should be more restricted, or whether MPs should be made to be more transparent about what they’re doing.”

Additional reporting: Ganesh Rao

Shares in UK banks have fallen sharply on the back of a report which urges the chancellor to place their profits in her sights at the coming budget.

As Rachel Reeves stares down a growing deficit – estimated at between £20bn-£40bn heading into the autumn – the Institute for Public Policy Research (IPPR) said there was an opportunity for a windfall by closing a loophole.

It recommended a new levy on the interest UK lenders receive from the Bank of England, amounting to £22bn a year, on reserves held as a result of the Bank’s historic quantitative easing, or bond-buying, programme.

Money latest: Ryanair changes cabin bag sizing

It was first introduced at the height of the financial crisis, in 2009.

The left-leaning think-tank said the money received by banks amounted to a subsidy and suggested £8bn could be taken from them annually to pay for public services.

It argued that the loss-making scheme – a consequence of rising interest rates since 2021 – had left taxpayers footing the bill unfairly as the Treasury has to cover any loss.

Why taxes might go up

The Bank recently estimated the total hit would amount to £115bn over the course of its lifetime.

The publication of the report coincided with a story in the Financial Times which spoke of growing fears within the banking sector that it was firmly in the chancellor’s sights.

Her first budget, in late October last year, put businesses on the hook for the bulk of its tax-raising measures.

Ms Reeves is under pressure to find more money from somewhere as she has ruled out breaking her own fiscal rules to help secure the cash she needs through heightened borrowing.

Is Labour plotting a ‘wealth tax’?

Other measures understood to be under consideration include a wealth tax, new property tax and a shake-up that could lead to a replacement for council tax.

Analysts at Exane told clients in a note: “In the last couple of years, the chancellor has been protective of the banks and has avoided raising taxes.

“However, public finances may require additional cash and pressures for a bank tax from within the Labour party seem to be rising,” it concluded.

The investor flight saw shares in Lloyds and NatWest plunge by more than 5%. Those for Barclays were more than 4% lower at one stage.

A spokesperson for the Treasury said the best way to strengthen public finances was to speed up economic growth.

“Changes to tax and spend policy are not the only ways of doing this, as seen with our planning reforms,” they added.

The man dubbed “Britain’s most hated boss” for his controversial policy of sacking hundreds of seafarers and replacing them with cheaper agency staff is to quit.

Sky News can exclusively reveal that Peter Hebblethwaite, the chief executive of P&O Ferries, is leaving the company.

Sources said he had decided to resign for personal reasons.

Money latest: The exact time to book train ticket at bargain price

Mr Hebblethwaite joined the ranks of Britain’s most notorious corporate figures in 2022 when P&O Ferries – a subsidiary of the giant Dubai-based ports operator DP World – said it was sacking 800 staff with immediate effect – some of whom learned their fate via a video message.

The policy, which Mr Hebblethwaite defended to MPs during subsequent select committee hearings, erupted into a national scandal, prompting changes in the law to give workers greater protection.

Under the new legislation, the government plans to tighten collective redundancy requirements for operators of foreign vessels.

In a statement issued in response to a request from Sky News, a P&O Ferries spokesperson said: “Peter Hebblethwaite has communicated his intention to resign from his position as chief executive officer to dedicate more time to family matters.

Peter Hebblethwaite gives evidence to a committee of MPs in 2022. Pic: PA

“P&O Ferries extends its gratitude to Peter Hebblethwaite for his contributions as CEO over the past four years.

“During his tenure the company navigated the challenges of the COVID-19 pandemic, initiated a path towards financial stability, and introduced the world’s first large double-ended hybrid ferries on the Dover-Calais route, thereby enhancing sustainability.

“We extend our best wishes to him for his future endeavours.”

A source close to the company said it anticipated making an announcement on Mr Hebblethwaite’s successor in the near term.

A former executive at J Sainsbury, Greene King and Alliance Unichem, Mr Hebblethwaite joined P&O Ferries in 2019, before taking over as chief executive in November 2021.

Insiders claimed on Friday that he had “transformed” the business following the bitter blows dealt to its finances by the COVID-19 pandemic and – to some degree – by the impact of Britain’s exit from the European Union.

A union protest is shown at the height of the mass sackings row in 2022

P&O Ferries carries 4.5 million passengers annually on routes between the UK and continental European ports including Calais and Rotterdam.

It also operates a route between Northern Ireland and Scotland, and is a major freight carrier.

The company’s losses soared during the pandemic, with DP World – its sole shareholder – supporting it through hundreds of millions of pounds in loans.

Its most recent accounts, which were significantly delayed, showed a significant reduction in losses in 2023 to just over £90m.

The reduction from the previous year’s figure of almost £250m was partly attributed to cost reduction exercises.

The accounts also showed that Mr Hebblethwaite received a pay package of £683,000, including a bonus of £183,000.

“I reflected on accepting that payment, but ultimately I did decide to accept it,” he told MPs.

“I do recognise it is not a decision that everybody would have made.”

The row over his pay was especially acute because of his admission that P&O Ferries’ lowest-paid seafarers received hourly pay of just £4.87.

Mr Hebblethwaite had argued since the mass sackings of 2022 that the company would have gone bust without the drastic cost-cutting that it entailed.

The company insisted at the time that those affected by the redundancies had been offered “enhanced” packages to leave.

Last October, the then transport secretary, Louise Haigh, said: “The mass sacking by P&O Ferries was a national scandal which can never be allowed to happen again,” adding that measures to protect seafarers from “rogue employers” would prevent a repetition.

“This issue has been ignored for over 2 years, but this new government is moving fast and bringing forward measures within 100 days,” Ms Haigh added.

“We are closing the legal loophole that P&O Ferries exploited when they sacked almost 800 dedicated seafarers and replaced them with low-paid agency workers and we are requiring operators to pay the equivalent of National Minimum Wage in UK waters.

“Make no mistake – this is good for workers and good for business.”

The minister’s description of P&O Ferries as “rogue”, and suggestion that consumers should boycott the company, sparked a row which threatened to overshadow the government’s International Investment Summit last October.

Sky News’s business and economics correspondent, Paul Kelso, revealed that DP World had withdrawn from participating in the event, and paused a £1bn investment announcement.

The company relented after Sir Keir Starmer publicly distanced the government from Ms Haigh’s characterisation of DP World.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment11 months ago

Environment11 months agoHere are the best electric bikes you can buy at every price level in October 2024