Volkswagen Commercial doubled EV deliveries in 2022, led by tremendous ID.Buzz demand

Volkswagen Commercial Vehicles has released its annual numbers for 2022 and is reporting strong output for its vehicles, including a doubling of EV deliveries dominated by the ID.Buzz electric van. Better still, the number of Buzz vans delivered last year is a mere fraction of what Volkswagen already has in its order books.

If the name didn’t already give it away, Volkswagen Commercial Vehicles is a marque of Volkswagen Group centered around the light commercial segment. 2022 saw the start of production of the ID.Buzz electric van after it was officially unveiled last March.

Contrary to other ID EVs donning VW badge built at the automaker’s Zwickau-Mosel Plant, the ID.Buzz is produced by the commercial division at its plant in Hannover-Stöcken, following a major overhaul to support EV production – a new assembly process for the long-running facility.

Deliveries of the ID.Buzz did not begin until the latter half of 2022, but Volkswagen is optimistic about its future based on the number of deliveries completely thus far. Furthermore, the number of deliveries on order for 2023 is already tenfold.

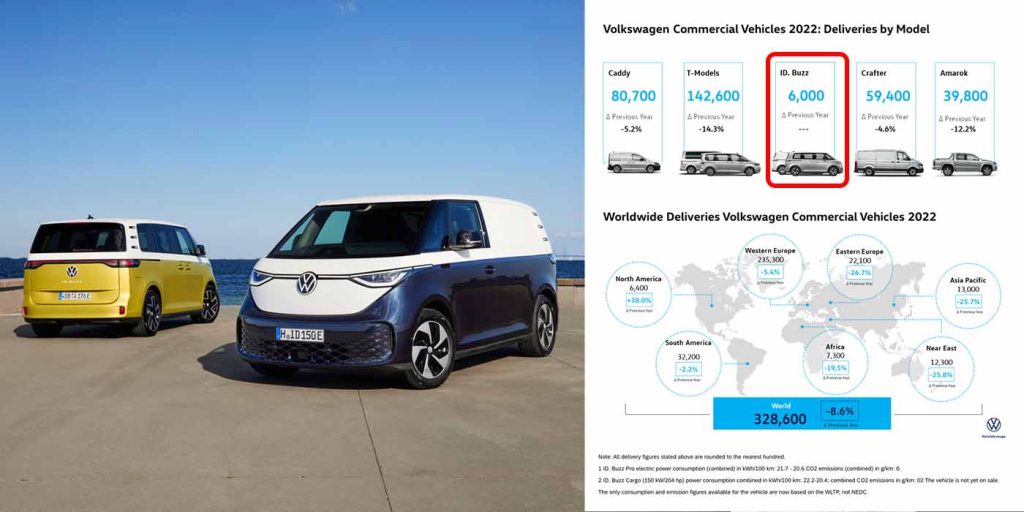

Volkswagen reports over 6,000 ID.Buzz deliveries so far

Despite 6,000 Buzz deliveries alone by the end of 2022, Volkswagen also reported over 10,000 electric vans already built in Hannover, with even more on the way. The German automaker shared that by the time the ID.Buzz reached dealerships this past fall, it already had over 21,000 customer orders in place.

The commercial division of Volkswagen will look to fill this growing number of Buzz orders in 2023 en route to a new record in EV deliveries. If that does happen, Volkswagen Commercial Vehicles will continue its trend from last year, which saw 7,500 EV deliveries – more than double the 3,600 that made their way to customers in 2021. VWCV’s member of the board of management for sales and marketing Lars Krause shared in the excitement, puns and all:

Our ID. Buzz created a real BUZZ in 2022 – not just here, but all over the world. We are very happy with the launch of our first all-electric Bulli from Hannover. Now, our task is to further ramp up production of all models and to deliver the vehicles to our customers and fans.” Krause continued: “In the last few months, we’ve already succeeded in doing this and we’ve been able since September to increase deliveries to customers significantly. In November and December, we sent out 30 per cent more vehicles than in the same period last year.

By the end of 2022, Volkswagen stated that orders for the ID.Buzz Pro and ID.Buzz cargo totaled 26,600, leaving plenty to keep the commercial division busy overseas. VWCV reported 328,600 customer deliveries in total last year, marking a downward trend of 8.6%.

However, growing demand for the ID.Buzz at both the commercial and consumer level leaves room for optimism, especially as the division looks to make 55% of all sales BEV by 2030.

FTC: We use income earning auto affiliate links. More.

From the ashes of Elon Musk’s decision to fire the whole Supercharger team last year, a new company has risen: Hubber, which will take its founders’ expertise at setting up Tesla Superchargers and apply that to addressing the lack of high-speed urban charging for taxis and other commercial vehicles.

Last year, Tesla CEO Elon Musk suddenly fired the entire charging department, in what is one of the more chaotic decisions he’s made yet.

In the immediate aftermath of this decision, a lot of questions were asked around the industry – and a lot of companies started snatching up talent from the best EV charging team in the world.

Or, alternately, some of that talent went to form their own companies. That’s the case for Harry Fox, Connor Selwood and Hugh Leckie, who met at Tesla and together oversaw the rollout of 100 Supercharger sites with 1,200 total chargers across the UK & Ireland. And after the shakeup of the Supercharger team, they set off to charge a new path of their own.

The three formed Hubber, which pitches itself as a new type of EV charging company, focused on solving “the urban charging gap.”

Hubber describes itself as “the UK’s leading specialist in urban high-powered EV charging, addressing one of the most urgent constraints in the energy transition: the shortage of fast, reliable charging in major cities.” It “acquires and develops prime urban sites into large-scale charging hubs, combining deep grid-connection know-how with a proven ability to deliver complex infrastructure at speed”.

A large amount of the traffic in UK cities is taken up by taxis and last-mile, and these vehicles tend to see higher utilization than commuter cars, so they need to charge more often. Hubber says that taxis charge five times as often as a private vehicle, which means they’ll need more access to fast EV charging.

This is further exacerbated in urban environments, where EVs might not park in a place they can charge. Lots of urban homes don’t have garages, and while there are street EV chargers available in London, they’re not everywhere yet. So convenient fast charging is essential.

And the needs for commercial drivers are different than those of other commuters. While nicely-appointed charging plazas (like Rove’s “full service” EV charger in Santa Ana, CA) are great for the average consumer, commercial EV drivers put more of a premium on speed and affordability, and don’t mind if a site is a little further off of a main thoroughfare, or not as close to food or shopping as other drivers might want.

So Hubber is looking at sites that other developers might pass over – like old warehouses or gas stations – and figuring out how to turn them into an ideal site for high-throughput charging.

With its cofounders’ experience at Tesla, Hubber will buy sites, transform them into a charger-ready location, and essentially provide the dream location that they would have liked to see during the site selection processes they went through in their previous jobs.

The charging hubs could still have some amenities, like restrooms and vending machines, of the type that would be useful for taxi or ride-hailing drivers to grab during a quick stop. But the main focus would be on getting people in and out and back on the road.

Here’s a rendering of what a potential site might look like. In this sample location, there would be room for light-duty vehicles up front, with an area for larger last-mile delivery vehicles with larger charging bays. A small covered area could provide restrooms and vending, and another portion of the site could be dedicated to transformers, batteries and the like.

Hubber is also thinking ahead to a possible autonomous future, where driverless ride-hailing vehicles like those from Waymo could have a place to charge. Although given that there aren’t currently great solutions for autonomous charging, an attendant might have to be involved for the foreseeable future.

The company would also like to expand beyond the UK and Ireland, but they’re sticking to home base for the time being. After all, things are just getting off the ground – but the £60 million (~$81m) investment that Hubber just secured is certainly a big boost towards getting the project moving.

Speaking of projects, Hubber’s first facility is opening this coming week, on August 20th. The site is at Forest Hill in South London, near Forest Hill Station. It will have 12 EV charging bays, with 3 150kW and 3 300kW dual-head chargers. The site will be operated by RAW charging, which will offer free fast charging for its first week of operation.

Electrek’s Take

As we said at the time, firing the whole Supercharger team was a dumb decision. It was immediately obvious to everyone in the industry that it was a dumb decision, and Tesla did eventually relent and rehire some of the fired workers, but the damage was done – and not just for the charging team, but morale was made low throughout the organization.

The silver lining, at least for the rest of the industry, is that it allowed this talent to be distributed around to other companies. This isn’t beneficial for Tesla and did cause chaos which has likely affected the rollout of NACS, slowed EV charging site development in the US, and so on, but it has been beneficial for other companies who managed to snatch up talent.

Or, for companies like Hubber, which were formed by that talent.

It’s an interesting idea, and I like the angle of focusing on taxis in order to increase utilization of the site. EV charging is potentially an interesting business long term, but currently a lot of chargers see low usage because it’s so easy for most of the people who own EVs to charge at home.

But we’re going to have to move beyond the market of people who can easily charge in a garage attached to a single family home, especially in cities. Getting an easy way for the cars that get used the most in a city to charge is a really important move, and we’re looking forward to seeing how Hubber can help with this. And having a leadership team consisting of people who formerly worked at the best charging team in the industry isn’t a bad start.

The 30% federal solar tax credit is ending this year. If you’ve ever considered going solar, now’s the time to act. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

Indian ag and automaker Mahindra has launched a limited-run Batman Edition of its BE 6 Electric Origin SUV, calling it, “a production car that brings to life a rare fusion of cinematic heritage and modern luxury, inspired by Christopher Nolan’s critically acclaimed The Dark Knight Trilogy from Warner Bros. Pictures.”

And, you guys – the new Mahindra BE 6 is. So. Serious.

Someone at Mahindra is very taken with American culture it seems. After launching the Willys MB Jeep-inspired Mahindra Roxor a few years ago, the company followed it up by building a credible line of EVs co-developed with VW. Now, they’re building a limited edition of one of those EVs inspired by another American cultural icon.

“Batman is more than a pop-culture icon — he represents innovation, resilience, and an unyielding drive to push boundaries,” says Vikram Sharma, Senior Vice President, Warner Bros. Discovery Global Consumer Products, APAC. “This collaboration brings that spirit to the road in a bold, electric way. With this limited-edition range, fans in India can now experience the thrill of Batman every time they drive. It’s a collector’s statement on wheels.”

To separate the Batman Edition from the other Mahindra SUVs, its makers have festooned their EV with Dark Knight logos and branding, inside and out.

Batman Edition features

Exterior

- Custom Satin Black Colour premieres on the Batman Edition

- Custom Batman Decal on front doors

- R20 alloy wheels for an aggressive, athletic stance

- Alchemy Gold-painted suspension and brake callipers a bold, premium contrast to the Satin black body

- “BE 6 × The Dark Knight”, limited edition, rear badging

- The Bat emblem, as seen in The Dark Knight Trilogy, uniquely placed on:

- Hub caps

- Front quarter panels

- Rear bumper

- Windows & Rear Windshield

- Infinity Roof featuring The Dark Knight Trilogy Bat emblem

- Night Trail – Carpet lamps with The Dark Knight Trilogy Bat emblem logo projection

- ‘Batman Edition’ signature sticker on rear door cladding

Interior

- Brushed Alchemy Gold Batman Edition plaque on the dashboard with numbering

- Charcoal leather instrument panel (IP) with brushed gold halo around driver cockpit

- Suede and leather upholstery with gold sepia accent stitching and integrated The Dark Knight Trilogy Bat emblem for a rich, tactile experience

- Gold-accented steering wheel, In-Touch Controller, Electronic Parking Brake, custom key fob with Alchemy gold detailing

- The Dark Knight Trilogy Bat emblem embossed on:

- The “Boost” button

- Seats

- Interior labels

- Pinstripe graphic and The Dark Knight Trilogy Bat Emblem across the passenger dashboard panel

- Race car inspired open straps with Batman Edition Branding Batman Edition welcome animation on the infotainment display

- Custom Batman inspired exterior engine sounds

Despite all the Batman branding, the end result is almost tasteful. I could do without the custom Batman decal on the front quarter panels, but the rest of the mods are far less offensive. I even like the little “Bat Signal” puddle lights on the wing mirrors.

Mahindra Batman BE 6

As a car, the special edition Batman Mahindra is based on the top-shelf version of the BE 6, fitted with a 79 kWh battery good for 550 km (about 340 miles) of range according to its WLTP rating. That battery sends power to a rear-mounted 282 hp (210 kW / 286 PS) electric motor generating and 380 Nm (about 280 lb-ft) of torque that sends power to the rear wheels.

The BE6 also features a modern Level 2 ADAS tech and screens everywhere, including in the steering wheel hub – which seems like it might get particularly nasty in an airbag deployment (but no one asked me).

Pricing starts at ₹27.79 lakh (a little under $27,500, as I type this), and production will be limited to just 300 units. Order books are set to open 23AUG.

SOURCE | IMAGES: Mahindra.

If you’re considering going solar, it’s always a good idea to get quotes from a few installers. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

Electric bike and scooter safety is now part of the curriculum in some schools – and surprisingly, it’s happening in Florida.

Yes, Florida. The state that’s better known for keeping education out of schools, banning everything from books to the word “gay.” But now, a Central Florida nonprofit is stepping in to make sure students are at least learning how to ride responsibly.

The group Best Foot Forward for Pedestrian Safety has partnered with local police departments and Orange County Public Schools to bring e-bike and e-scooter safety programs directly into middle schools and high schools. The initiative is focused on addressing the growing number of crashes and injuries involving students riding electric two-wheelers.

The safety course covers basics like wearing helmets, obeying traffic laws, and making yourself visible to drivers — skills that are important for the many young riders who are increasingly taking to electric bikes as a form of independent transportation around their cities and neighborhoods. One of the main topics of the program is said to be speed management. The program addresses the importance of keeping speeds reasonable and the impacts of faster riding.

Like much of the US, Florida has seen a surge in e-bike and e-scooter popularity among kids and teens, especially in suburban and coastal areas. While many embrace them as a fun and fast way to get around, the sudden rise has also come with a worrying spike in injuries and deaths, prompting calls for improvements in both infrastructure and education.

With e-bike usage exploding across the US, more schools and communities are exploring steps to increase rider education. It’s a sign that America’s transportation habits are changing – and our education systems are beginning to catch up.

Electrek’s Take

I think programs like this are great because they teach kids things that they’d otherwise have to learn through trial and error. We don’t just hand cars to sixteen-year-olds and say, “figure it out.” So it follows that some form of organized rider education would be important as more youths take to e-bikes than ever before.

In cycling-intensive cities in Europe, all schools teach kids to ride bikes, often giving the kids some form of cute little cycling diploma to demonstrate that they’ve passed the course and can safely ride a bike.

But at the same time, this makes me wonder if we’re still missing the point. Responding to an increase in e-bike rider deaths with lessons about bicycle speed management is a bit like responding to mass shootings by lecturing innocent passersby about why they shouldn’t run into bullets.

Educating riders is always great and I’ll always support it. But in parallel, perhaps we should also be addressing the root cause of all of these tragics deaths. At the end of the day, most electric bike-related deaths aren’t a result of an e-bike rider doing too much fast riding; they’re a result of a car driver doing too much running over a cyclist.

via: Fox13

FTC: We use income earning auto affiliate links. More.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike