Mortgage approvals at lowest level since early months of pandemic

The number of new mortgages approved has dropped for the fourth month in a row, to a low not seen since the early days of the pandemic.

Mortgage approvals fell to 35,600 in December, the lowest number since May 2020 and down from 46,200 in November, according to data from the Bank of England.

The figure from the central bank lower than had been expected – a Reuters poll of economists had forecast approvals of about 45,000 during December.

If the pandemic era is excluded, house purchase approvals are at the lowest level since January 2009 when 32,400 home purchase loans were approved.

Approvals have been slow since the Liz Truss government’s mini-budget, when a number of mortgage products were pulled from the market as uncertainty spooked lenders.

The figures are just the latest sign of a slowing housing market.

Prices have been coming down overall as persistent double digit inflation means the cost of living is higher, and raised interest rates – hiked by the Bank of England in an effort to slow the economy to reduce inflation – have made the cost of mortgage payments more expensive, putting off would-be buyers.

While the Bank set the interest rate to 3.5%, the latest figures found that the effective interest rate – the actual interest rate paid – on new mortgages increased by 32 percentage points, to 3.67% last month.

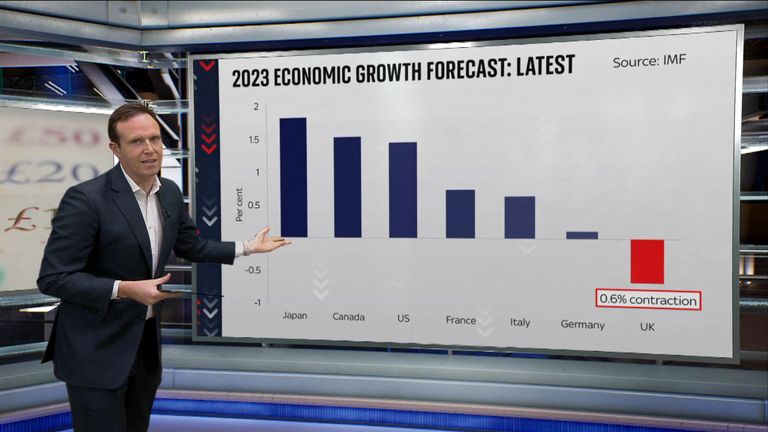

The International Monetary Fund (IMF) forecast says that this year the UK economy will fare worse than any other country in the developed world – including Russia.

Read more:

UK economy set to fare worse than any other country in developed world

At the same time, mortgage debt has reduced. Tuesday’s figures showed net mortgage borrowing by individuals – the total amount borrowed minus the amount repaid – decreased from £4.3bn in November to £3.2bn last month.

The signs show this figure will continue to decrease while mortgage approvals, which indicate future borrowing, were down.

Cost of living pressures on households could be seen as people also continued to borrow more than they’re repaying on credit cards. An additional £500m in net consumer credit – the amount borrowed minus the amount repaid – was borrowed in December. The annual growth rate of credit card borrowing rose to 12.4% in December from 12.2% in November.

A company which makes miniaturised electric versions of classic cars has secured a rescue deal led by an American merchant banking group.

Sky News understands that the future of Hedley Studios – formerly known as The Little Car Company – has been salvaged through a pre-pack administration deal.

FRP Advisory is understood to have acted as administrator before selling the business to an entity controlled by Island Capital Group.

Hedley Studios was founded in 2018, when luxury car-maker Bugatti approached Ben Hedley to see if he could recreate a 1920s Type 35 racing car at half-scale to mark its 110th anniversary.

In a statement issued in response to an enquiry from Sky News, the company said it had built and delivered more than 500 vehicles to clients in more than 60 countries in the last 17 months.

Hedley Studios manufactures its cars at three-quarters the size of the original model, with the resulting vehicles typically costing £75,000 or more.

Pic: Hedley Studios

“We’re thrilled to welcome Island Capital Group as a strategic partner in the next phase of Hedley Studios’ growth,” Mr Hedley said.

“Its investment and belief in our vision mark a pivotal moment for the company as we accelerate our expansion and reach new global audiences.

Hedley Studios makes its cars in partnership with a range of luxury manufacturers, including Aston Martin, Bentley and Ferrari.

Andrew Farkas, founder, chairman and CEO of Island Capital, which initially backed Hedley Studios in 2023, said: “This latest investment is testament to the entrepreneurial spirit of Ben and his team in building a successful British luxury brand in a short period of time.

“Automotive enthusiasts globally are increasingly keen to honour these historic icons, bringing them to new audiences in a new, fully electric way.

“Our broader investment marks the beginning of a new chapter for Hedley Studios, reinforcing its position as a leader in the creation of luxury, driveable artworks, and Island Capital is excited to be part of that growth journey.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike