Nursery fees ‘to rise by £1,000 this year’ as childcare providers struggle with costs – forcing parents to quit work

The soaring cost of childcare in the UK is revealed in new figures today, suggesting nurseries will raise fees by £1,000 this year.

A survey of 1,156 providers by the Early Years Alliance found nine out of 10 expect to increase fees, typically in April, and by an average of 8% – higher than in previous years.

Cost of living – latest: Semi-skimmed milk and children’s jeans – the details behind inflation

UK childcare costs are already among the most expensive in the world, with full-time fees for a child under two at nursery reaching an average £269 a week last year – or just under £14,000 annually.

An 8% rise would take that to more than £15,000.

Three and four-year-olds in England attending a nursery or childminder are eligible for either 15 or 30 free hours a week depending on whether their parents work, so their costs are a lot lower.

There are different schemes in Wales and Scotland.

But the concern is that by this stage many parents – particularly mothers – have felt forced to drop out of work or cut their hours.

Tory MPs have been pressing the chancellor to take measures to make childcare more affordable in the March budget in order to reduce pressure on families, and enable more women to re-enter the workforce.

But an option to extend free hours to all two-year-olds is understood to have been ruled out.

Most nurseries and childminders surveyed – 87% – said the money they get from the government does not cover their costs to provide the “free” hours – leaving them out of pocket.

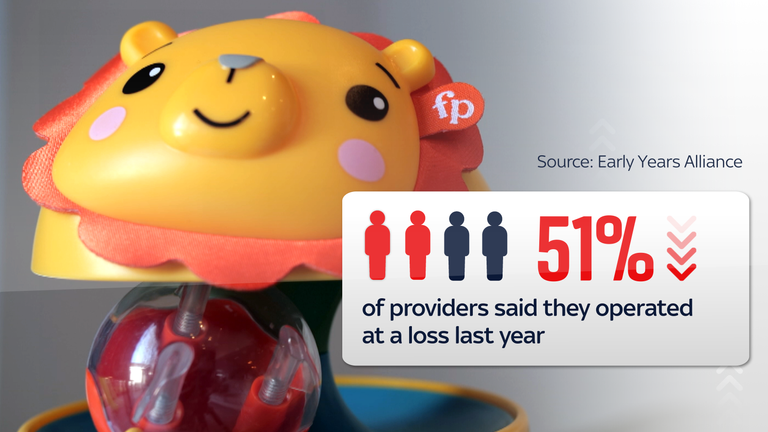

More than half of providers (51%) said they had operated at a loss last year. A handful said they were looking at fee increases of as much as 25%.

Becky Burdaky, 26, from Wythenshawe, Greater Manchester, told Sky News she had taken the “daunting” decision to leave her job in sales after having her second child, Bobby, last year.

Her daughter Harriet, aged three, goes to pre-school near their home, but the family found the costs they would face for their baby son beyond their reach.

She will stay at home and they will live on the wages of her partner Steve, an electrician.

‘Not asking other people to pay for my kids’

Becky said: “When we looked into the fees it was £70 a day – it would have been all of my wage. With Harriet it was about £54, so that’s a huge difference.

“And if he was home poorly, I wouldn’t get paid but I’d still have to pay his fee. Once we sat down and worked it out I would have been paying to go to work.

“I never envisaged myself being a stay-at-home mum, you know just cooking and cleaning and bringing up children, as I’ve always worked.

Becky says she could be starting from the bottom again when she returns to work

“It’s our decision to have children – I’m not asking other people to pay for my children. And I definitely don’t want people’s taxes to go up because of it.

“But I think slightly subsidising the cost of fees so it’s affordable for working parents means we can work and contribute.

“You don’t know what it’s going to be like when you return to work, you’re starting from the bottom.”

The campaign group Pregnant Then Screwed surveyed 27,000 parents last year and found nearly two thirds paid more for childcare than their rent or mortgage.

Although childcare costs have risen significantly in recent years, many providers are struggling to stay in business – with 5,400 closing their doors in the year to August 2022.

Fees for the youngest children, aged under three, are often used to keep the nurseries in business, and the rising cost of living means parents are cutting back.

‘I’ve put my savings in to cover wages’

Delia Morris is the owner of Morris Minors pre-school in Croxley Green, Hertfordshire, where children used to start aged two but are now increasingly starting at three.

She is paid £5.41 an hour by the local authority for their free hours, but says providing it costs her around £7.

“Children come in later, when they are funded,” she said.

“That’s had a huge impact. I did raise my fees a very small amount this year but it doesn’t cover it because we only have one or two children doing a couple of sessions a week [that parents pay for].

“I’ve had to put my own savings in to cover the wages last summer, and the staff had to drop a session.”

As to what the government should do, she said: “They have to put money in. It’s difficult to say, but I have to be realistic that if I can’t make ends meet I will have to close and that’s it.”

Delia Morris says the government should provide extra funding for childcare

Neil Leitch, chief executive of the Early Years Alliance, said the organisation had closed half of the 132 nurseries it operated in the last four years.

“They are exclusively in areas of deprivation, which seems to fly in the face of any levelling up agenda. These are families and children who would benefit most from support and care,” he said.

According to the OECD, the UK tops the table for the proportion of a mother’s income taken up by childcare costs – based on two children in full-time care.

‘The gender pay gap just explodes’

Christine Farquharson, education economist at the Institute for Fiscal Studies, said childcare costs for two-year-olds have risen twice as fast as inflation in the past decade – with a lasting effect on women’s pay.

“We ended up in a situation where the youngest children have the highest prices they’re ever going to pay, with the least access to government support,” she said.

“And it’s coming at this critical moment where parents are making decisions about whether or not to go back to work after they’ve been on parental leave.

“When mothers – and it is mostly mothers – make that choice to step back from the labour market it’s not just those few years. The gender pay gap just explodes and literally takes decades to come back to anything approaching the situation before they became parents.”

Proposals, championed by Liz Truss, to increase the ratio of children looked after by each adult, have attracted opposition from nurseries and parents.

Click to subscribe to the Sky News Daily wherever you get your podcasts

But Tory MPs are pressing the government to help parents with the cost of childcare by reducing business rates for nurseries or extending free hours to two-year-olds.

Robin Walker, chair of the education select committee, said some of the existing schemes are not working effectively – such as tax-free childcare – for which uptake is only around 40%.

Universal Credit claimants are also eligible to have up to 85% of their childcare costs funded but are put off by having to make upfront payments.

“There is money there that isn’t being used,” he said. “Upfront payment for Universal Credit and tax-free childcare are putting a lot of parents off using them at all.

“The government is already spending more than any previous government has in this space, but other countries in Europe are spending more particularly in the 0-2 age bracket.

“If we were to make the case for more investment it would unlock those opportunities for people to continue in the workplace and stimulate children in the early years.”

If they win power, Labour have promised an expansion of childcare from the end of maternity leave until the start of primary school.

Shadow education secretary Bridget Philipson told Sky News this would be a “key battleground issue” at the next election.

A Department for Education spokesperson said: “We recognise that families and early years providers across the country are facing financial pressures and we are currently looking into options to improve the cost, flexibility, and availability of childcare.

“We have spent more than £20bn over the past five years to support families with the cost of childcare and the number of places available in England has remained stable since 2015, with thousands of parents benefitting from this.”

The world’s two largest economies, the US and China, have again extended the deadline for tariffs to come into effect.

A last-minute executive order from US President Donald Trump will prevent taxes on Chinese imports to the US from rising to 30%. Beijing also announced the extension of the tariff pause at the same time, according to the Ministry of Commerce.

Those tariffs on goods entering the US from China were due to take effect on Tuesday.

The extension allows for further negotiations with Chinese Premier Xi Jinping and also prevents tariffs from rising to 145%, a level threatened after tit for tat increases in the wake of Trump’s so-called liberation day announcement on 2 April.

Apple boss gives Trump 24 karat gold gift

It’s the second 90-day truce between the sides.

The countries reached an initial framework for cooperation in May, with the US reducing its 145% tariff on Chinese goods to 30%, while China’s 125% retaliatory tariffs went down to 10% on US items.

A tariff of 20% had been implemented on China when Mr Trump took office, over what his administration said was a failure to stop illegal drugs entering the US.

Sector-specific tariffs, such as the 25% tax on cars, aluminium and steel, remain in place.

Chinese stock markets were mixed in response to the news, with Hong Kong’s Hang Seng down 0.08%

The Shanghai Composite stock index rose 0.46%, and the Shenzhen Component gained 0.35%.

The rate of wage rises in the UK continued to slow as the number of job vacancies and people in work fell, according to new figures.

Average weekly earnings slowed to 4.6% down from 5%, while pay excluding bonuses continued to grow 5%, according to data from the Office for National Statistics (ONS) for the three months to June.

It means the gap between inflation – the rate of price rises – and wage increases is narrowing, and the labour market is slowing. Inflation stood at 3.6% in June.

Money latest: Supermarket coffee beats big brands in Americano taste test

The number of employees on payroll has fallen in ten of the last 12 months, with the falls concentrated in hospitality and retail, the ONS said. It came as employers faced higher wage bills from increased minimum wages and upped national insurance contributions.

As a result, it’s harder to get a job now than a year ago.

“Job vacancies, likewise, have continued to fall, also driven by fewer opportunities in these industries,” the ONS director of economic statistics, Liz McKeown, said.

The number of job vacancies fell for the 37th consecutive period and in 16 of the 18 industry sectors. Feedback from employers suggested firms may not be recruiting new workers or replacing those who left.

Unemployment remained at 4.7% in June, the same as in May.

The ONS, however, continued to advise caution in interpreting changes in the monthly unemployment rate due to concerns over the figures’ reliability.

Read more:

US and China extend tariffs deadline again

Full-time workers relying on food handouts

The exact number of unemployed people is unknown, partly because people do not respond to surveys and answer the phone when the ONS calls.

The worst is yet to come

Wage rises are expected to fall further, and redundancies are anticipated to rise.

“Wage growth is likely to weaken over the course of the year as softening economic conditions, rising redundancies and elevated staffing costs increasingly hinder pay settlements,” said Suren Thiru, the economics director of the Institute of Chartered Accountants in England and Wales (ICAEW).

“The UK jobs market is facing more pain in the coming months with higher labour costs likely to lift unemployment moderately higher, particularly given growing concerns over more tax rises in this autumn’s budget.”

Tax rises playing ’50:50′ role in rising inflation

What does it mean for interest rates?

While wage rises are slowing, the fact that they’re still above inflation means the interest rate setters of the Bank of England could be cautious about further cuts.

Higher pay can cause inflation to rise. The central bank is mandated to bring down inflation to 2%.

But one more interest rate cut this year, in December, is currently expected by investors, according to data from the London Stock Exchange Group (LSEG).

The evidence of a weakening labour market provides justification for the interest rate cut of last week.

Business

Money Problem: ‘My husband is freelance and in hospital – how can I make sure we don’t lose our home?’

Every week, our Money blog team finds the answer to a reader’s financial problem or consumer dispute. Here’s our latest…

My husband is freelance and the breadwinner of the family. He is in hospital for an unknown length of time. Is there any support for us in the short term, so we can keep our home?

Anonymous

Our cost of living specialist Megan Harwood-Baynes tackles this one…

I am so sorry to hear this – I have recently been through something similar with my husband, and it can be really stressful when you add financial worries on top of medical issues.

To help you navigate the next steps, I’ve broken this up into what support you can get with your mortgage specifically, government help and some advice on the rest of your bills.

Help with housing

Your most immediate concern seemed to be housing (understandably). First, try not to panic – it is easy to skip to the thought of losing your home, but the last thing your mortgage lender is going to want to do is go through the hassle of repossession for what could just be a short-term issue.

Start by having a look through your insurance – certain types of insurance can help with mortgage repayments if your income falls due to sickness.

(If you don’t have this, make a note to consider taking it out for next time – you never know when something like this could happen again, and income protection insurance could make a huge difference in the future.)

Assuming you don’t have insurance coverage, the next step is to contact your lender. The sooner you do this, the better, as you’re more likely to have better options available to you before you miss a payment.

Things you can ask for include:

- To lengthen the term of your mortgage;

- To switch to interest-only repayments;

- Ask about a temporary mortgage payment holiday.

More from this series:

‘BA went back on refund promise’

‘Dud car dealer won’t give my money back’

‘Who is right in my delivery dispute with TK Maxx?’

There are pros and cons to all of the above, which you should consider carefully.

For example, a mortgage holiday is only suitable as a temporary fix – remember, you are still racking up interest on your remaining mortgage. It will leave the balance and remaining payments higher than they were before.

If you have already missed a payment, you are now in mortgage arrears. This can damage your credit file, and yes, it could eventually lead to you losing your home. But there is still support to get you back on track. Again, contact your lender and ask them for support.

The UK’s biggest mortgage lenders and the Financial Conduct Authority agreed on a set of standards under Rishi Sunak’s government, known as the Mortgage Charter. Under this, lenders are obligated to offer tailored support to anyone struggling – whatever the right option is will depend on your circumstances – so go into discussions with the mindset that they are there to help you.

Government support

If your husband is freelance, you won’t be eligible for Statutory Sick Pay (SSP), but he will be able to claim Employment Support Allowance. This is for people who are self-employed, unemployed, classed as a student or who are employed but not eligible for SSP.

To apply, you will need to demonstrate that he is unable to work because of his illness or injury. The doctors should be able to provide a sick note and medical evidence for this.

You will need to make sure he has paid enough national insurance contributions. He should be able to check his records for gaps and then voluntarily fill them if need be.

He may also be eligible for a personal independence payment or PIP, which is for people living with disabilities or long-term health conditions.

In some cases, he may also be able to claim universal credit – this would be based on his monthly income before he went off sick.

As well as benefits, you may be entitled to a working-from-home tax rebate, or you could reclaim bank charges if you’ve incurred fees for going beyond your limit.

This seems overwhelming, I realise, so the best bet is to start by looking at the government’s benefits calculator.

You should also reach out to Citizens Advice or a charity such as Turn2us for advice from someone who can look at your situation in more detail.

If you aren’t yet in a debt crisis, I would caution against visiting a debt-counselling agency. They may push you towards declaring bankruptcy or an individual voluntary arrangement, which you may not need at this point. They are serious measures designed for those with few options left.

Pic: iStock

Help with bills and all the rest

Before you start missing payments on your bills, try to contact your utility companies first. Explain the circumstances – they are also obligated to help you.

You can claim support with your energy bills and any other costs. There’s no “one-size-fits-all” approach, so the best thing is to contact each of them individually.

Good luck, and I hope your husband recovers soon.

This feature is not intended as financial advice – the aim is to give an overview of the things you should think about. Submit your dilemma or consumer dispute via:

- WhatsApp here

- Or email moneyblog@sky.uk with the subject line “Money Problem”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike