So what’s the situation with EVs and solid state batteries already?

Electrek spoke with Dr. Greg Hitz, founder and CTO at Beltsville, Maryland-based ION Storage Systems, about what solid state batteries are, why they’re considered the “unicorn” of battery technology, and why they have yet to hit the market, and how his company is working to move the needle.

Electrek: Could you explain what solid state batteries are, what they’re used for, and how they differ from lithium-ion batteries?

Greg Hitz: Solid state batteries replace the flammable liquid electrolyte in a traditional lithium-ion battery with a solid electrolyte that serves the same function. They’re generally accepted as the key to unlocking the safety and energy density required for advanced electric vehicles and electrified flight.

It’s important to note, though, that not all solid state batteries are created equal. The different materials and configurations that underlie solid state battery technologies matter for safety, performance, energy density, and manufacturability.

Electrek: Solid state batteries are often referred to as the “unicorn” of battery technology. Why is that?

Greg Hitz: It’s a great analogy – you’ve never seen a solid state battery just like you’ve never seen a unicorn. Solid state batteries have long had the potential to outperform the batteries you see in most EV’s today; longer range, shorter recharge times, they’re safer. But nobody has yet shown that solid state batteries can deliver on their performance promise without making major sacrifices during battery pack integration like heating or compression requirements and can be produced with scalable manufacturing techniques.

Electrek: Why haven’t solid state batteries taken off yet?

Greg Hitz: No solid state battery manufacturer has yet to offer a 100% solution. Looking across the industry, there are technologies that have incredible rate performance, great energy density, strong safety, scalable manufacturing, and simple pack integration, but no single product offers all of that without significantly compromising one or more of the other aspects.

This is where we think ION differs from other technologies. Our first market customer will get a battery manufactured in the US that offers 40% more energy than their current solution and meets their needs on rate performance, cycle life, and production costs, all while inherently safe.

After our first market release, our second-generation product will incorporate future developments that will hugely extend the reach of the technology: doubling energy density, increased rate performance, order of magnitude decreases in production cost, qualifying long cycle life, and all the other targets required for wider market release such as EV production.

Electrek: How could solid state batteries achieve scale?

Greg Hitz: Scaling is hard and scaling batteries is even harder.

First, you need to design your battery to use plentiful, inexpensive resources. Cobalt and nickel are expensive and hard to source. ION has developed a battery with a lithium-free anode that supports nickel and cobalt-free cathodes.

Second, and perhaps most importantly, you need to design a battery that’s suited for manufacturing. The biggest targets here are energy-per-area – because cost of production is generally a per-area basis and batteries are sold per-energy – and use of highly scaled existing processing techniques.

Third, you need to create a win-win for manufacturing partners in the ecosystem. Solid state battery manufacturing is a whole new industry and there’s no widely scaled product that exists without an industry behind it. Look at the number of component suppliers for electric vehicles or for lithium-ion batteries. Dozens of companies contribute to the production of each unit sold. That complete package doesn’t yet exist in solid state batteries.

Lastly, you have to be in production to improve your production. That’s why we’re rolling out to smaller markets before we scale to EV. The pain of early production focuses the innovation and makes our EV production stronger.

Electrek: Why have cobalt and nickel become a source of pain for battery makers, and what other obstacles are there?

Greg Hitz: The only game in town for high energy density batteries right now is a nickel- and cobalt-based chemistry. There are alternatives, though.

Auto OEMs are switching to plentiful but less energy dense lithium iron phosphate chemistries for their shorter-range vehicles. Advanced nickel- and cobalt-free cathodes – incompatible with lithium-ion – that offer higher energy density without supply chain constraints exist, and have been waiting patiently for a technology to enable them.

ION’s platform technology is uniquely enabling to these plentiful and greater energy density chemistries and has been demonstrated with these cathodes, including sulfur and high voltage spinel chemistries, to name a few.

Electrek: Where are we in sourcing minerals ethically and sustainably for solid state batteries?

Greg Hitz: Solid state batteries unlock completely new chemistries, but that opportunity has to be intentionally harnessed to move to ethical and sustainable supply chains. We’ve worked with suppliers to achieve North American mineral sourcing and are working with recyclers to plan for end-of-life.

Photo: ION Storage Systems

Dr. Greg Hitz led the development of the multilayer garnet structure and co-founded Ion Storage Systems. He brings his experience in Good Manufacturing Practice to the company’s research culture, leading to an efficient transition from lab research to manufacturing operations. Greg received his PhD in materials science & engineering and bachelor’s in chemical engineering from the University of Maryland.

UnderstandSolar is a free service that links you to top-rated solar installers in your region for personalized solar estimates. Tesla now offers price matching, so it’s important to shop for the best quotes. Click here to learn more and get your quotes. — *ad.

FTC: We use income earning auto affiliate links. More.

After a sluggish stretch, US wind is heading into a pivotal moment, with a near-term rebound colliding with rising power demand, tariffs, and stubborn permitting bottlenecks.

US wind power: the next five years

The US is expected to add more than 7 gigawatts (GW) of new wind capacity in 2025, a 36% increase from this year, according to the latest US Wind Energy Monitor report from Wood Mackenzie and the American Clean Power Association (ACP).

That matters now because the US power grid is under mounting pressure, just as new generation has become harder to build. Electricity demand is rising for the first time in years, mainly driven by data centers and other large loads, while wind developers are navigating higher turbine costs, tariff uncertainty, and permitting delays. How quickly projects can move from the pipeline to completion over the next few years will shape whether wind can help keep the lights on and power prices in check.

Over the longer term, the outlook is steady but increasingly back‑loaded. The report still sees 46 GW of new wind capacity coming online between 2025 and 2029. What has changed is timing. More projects are now expected to reach completion in the middle of the decade, with 2026 and 2027 shaping up to be especially busy years at 10.7 GW and 12.7 GW, respectively, as projects move through the development pipeline.

That shift helps explain why installations lagged earlier this year. Wind additions in Q3 came in at 932 megawatts (MW), about 23% below forecasts. But activity is picking up fast. Developers have about 3.8 GW queued for Q4 2025 alone, which would account for 52% of the year’s total expected capacity. That kind of late-year rush is typical for wind projects, which tend to reach completion toward the end of the calendar year.

There are also signs of life on the manufacturing side. US turbine order intake rebounded in Q3 to pre–Trump’s big bill act levels, with more than 2 GW of firm commitments, the strongest quarter in the past nine months, and a 79% jump from the previous quarter. But you wouldn’t know it, because turbine makers are increasingly keeping project details close to their chests, and much of the qualifying “start-of-construction” activity is happening off-site through component manufacturing.

Looking further out, the report flags a noticeable slowdown toward the end of the decade. Capacity additions in 2029 are expected to drop sharply following project cancellations and inactive designations, largely due to permitting challenges and broader development constraints.

Power demand takes off

At the same time, the need for new power is growing fast.

After a decade of mostly flat electricity demand, US power demand is now expected to grow by around 3% per year through 2029, compared to just 0.7% over the previous decade. Data centers alone are expected to drive about 59 GW of the roughly 90 GW increase in peak demand. That kind of round-the-clock load makes more wind power a necessity.

“The US power market is facing mounting strain after a decade of flat demand, with utilities committing to 160 GW of large-load additions,” said Leila Garcia da Fonseca, Wood Mackenzie’s director of research. “This represents a significant opportunity for wind energy, which benefits from strengthened economic fundamentals and a compelling business case driven by its competitively low LCOE.”

But she also warned that higher turbine costs and policy uncertainty could slow down progress in the middle of the decade.

Onshore wind: Western states lead

Onshore wind continues to do the heavy lifting. The five-year onshore outlook remains unchanged at 39.8 GW of new capacity, and the 2025–2027 pipeline already has turbine orders in place for every project. More than 60% of that three-year capacity has either been commissioned or is already under construction.

Western states are leading the charge. Wyoming, New Mexico, and neighboring states are expected to account for about 34% of onshore activity over that period. Big projects are driving the numbers, including Pattern Energy’s 3.5 GW SunZia project in New Mexico, which is set to make the company the top wind installer in 2026, and Invenergy’s 998 MW Towner Energy Center in Colorado, the single largest project expected to come online in 2027.

Wind is also spreading into new territory. Arkansas recently brought its first utility-scale onshore wind farm online with Cordelio’s Crossover Wind (pictured).

Repowering older wind farms remains another bright spot. Wood Mackenzie expects 18 repowering projects to add about 2.5 GW of capacity over the next three years.

Offshore wind: progress, but pressure

Offshore wind is a different story. Wood Mackenzie expects offshore installations to slow in Q4 2025 due to harsh winter weather, pushing some capacity into 2026. Still, projects already under construction are making progress. Vineyard Wind connected 15 turbines in Q3 and delivered 200 gigawatt-hours (GWh) of electricity over the first nine months of the year.

“US offshore wind shows diverging momentum,” Garcia da Fonseca said. “Projects under construction with commercial operation dates in 2026 continue to hit key milestones, but post-2027 developments face potential delays amid constrained wind turbine installation vessel capacity, driving delays and contract terminations.”

The offshore sector is also under growing financial strain – and let’s not forget political attack from the Trump administration – with delays and contract terminations weighing on late-decade projects.

Tariffs are making turbines more expensive

Tariffs remain one of the biggest wild cards for the US wind industry. Wood Mackenzie expects tariffs to push turbine costs higher in 2026 before easing in later years. Overall, US onshore wind capital spending is projected to rise by about 5% through 2029.

“US wind turbine pricing is experiencing unprecedented uncertainty as conflicting market and regulatory forces interact,” said Garcia da Fonseca. While domestic manufacturing capacity could eventually bring prices down, tariffs on raw materials and key components are expected to keep costs elevated in the near term.

Read more: Federal judge rules Trump’s offshore wind ban illegal

If you’re looking to replace your old HVAC equipment, it’s always a good idea to get quotes from a few installers. To make sure you’re finding a trusted, reliable HVAC installer near you that offers competitive pricing on heat pumps, check out EnergySage. EnergySage is a free service that makes it easy for you to get a heat pump. They have pre-vetted heat pump installers competing for your business, ensuring you get high quality solutions. Plus, it’s free to use!

Your personalized heat pump quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here. – *ad

FTC: We use income earning auto affiliate links. More.

reassures investors on growth plans after its stock hits a new low")

After Lucid Group’s (LCID) stock price reached a new all-time low this week, the company’s communication boss is out to set the record straight.

Lucid stock hits a new low as investors wait

Lucid is facing new headwinds in the US at a critical time as the EV maker looks to enter its next growth phase. It’s ramping up output of its first electric SUV, the Gravity, and is set to launch its midsize platform in late 2026.

Like all automakers, the company is facing new headwinds in the US under the Trump administration, but that isn’t stopping Lucid from continuing on its mission of “changing the world through innovation and efficiency.”

Lucid’s head of communications, Nick Twork, reassured investors on Thursday that while others are pulling back, the company is still plowing ahead.

“We know it’s been a challenging period for our long-term holders,” Twork said, adding, “We are focused on execution and being transparent.” Twork reaffirmed investors that Lucid has “a strong liquidity runway,” including a $2 billion PIF credit facility, and another $2 billion in refinanced convertible notes that now mature in 2030/31.

$LCID investors: we know it’s been a challenging period for our long-term holders. We are focused on execution and being transparent. As our CFO Taoufiq has said, we have a strong liquidity runway, including an undrawn $2B PIF credit facility, and we refinanced $2B of converts… pic.twitter.com/4gvzFqmpLj

— Nick Twork (@ntwork) December 18, 2025

While other automakers are scaling back EV plans, including Ford most recently, “we’re building through it and ramping,” Lucid’s communications boss said.

After a magnet shortage and other supply chain constraints hampered Gravity production early on, Lucid now expects the electric SUV to make up the majority of production and deliveries in the fourth quarter.

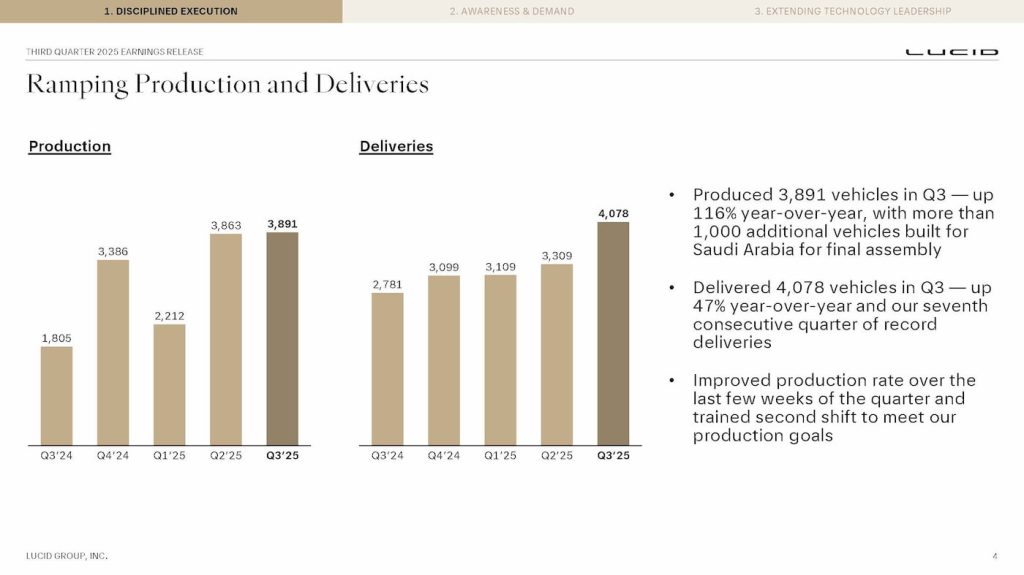

Speaking at the 53rd Annual Nasdaq Investor Conference last week, Lucid’s interim CEO, Marc Winterhoff, said the company “is on track” to hit its guidance of producing 18,000 vehicles this year. That’s at the lower end of its initial 20,000 to 18,000 target, but Winterhoff said output is picking up and Lucid now has “weeks where we are producing 1,000 vehicles” in a single week.”

Hitting that 18,000 target won’t be easy. Through the third quarter, Lucid produced 9,966 EVs, meaning it will need to build over 8,000 more in Q4. That’s more than double the 3,891 it made in the third quarter.

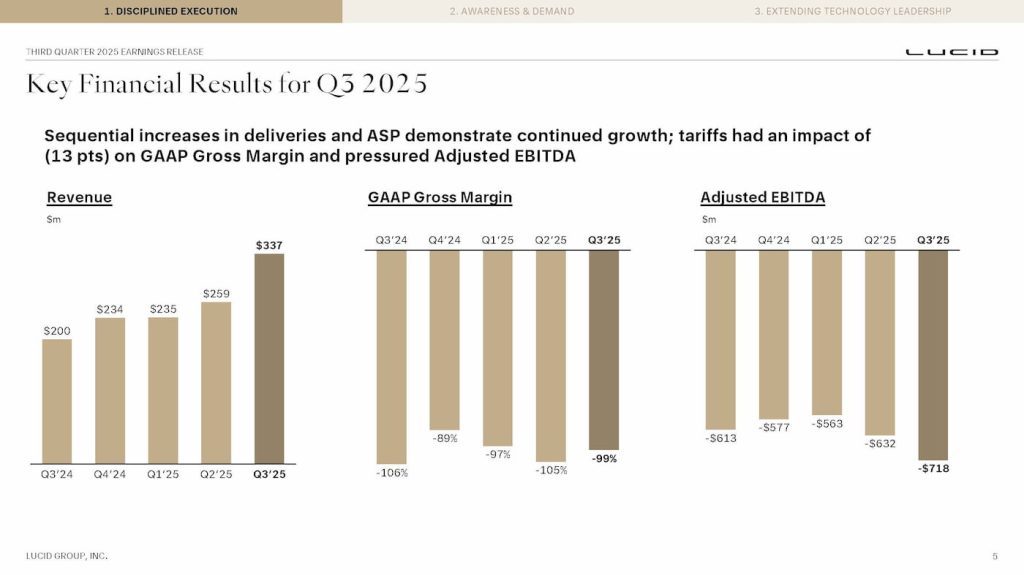

Lucid had about $4.2 billion in liquidity at the end of Q3, but after agreeing with PIF to increase the delayed draw term loan credit facility (DDTL), the company said total liquidity would have been around $5.5 billion.

The capital is enough to fund it through the first half of 2027, Lucid said. Later next year, Lucid will begin production of its midsize platform, which will underpin at least three new vehicles priced around $50,000.

Lucid’s first midsize model will be an electric crossover SUV, followed by a more rugged version inspired by the Gravity X concept. The third is rumoured to be a midsize sedan that will compete with the Tesla Model 3.

During a fireside chat at the UBS Global Industrials and Transportation Conference earlier this month, Lucid’s CFO, Taoufiq Boussaid, said the midsize EVs will be positioned in “the heart of the market,” starting at around $50,000.

While Rivian (RIVN) and Tesla (TSLA) shares are trading up by over 50% and 27%, respectively, since the beginning of 2025, Lucid’s stock price has fallen by over 60%. Earlier this week, Lucid’s stock touched an all-time low of $11.09 per share.

Twork said Lucid will share more information about its growth plans during its Capital Market Day in the first quarter.

FTC: We use income earning auto affiliate links. More.

Like a 90s “gifted” kid that was supposed to be a lot of things, the electric Jeep Wagoneer S was supposed to be sporty, luxurious, and appeal to a whole new Jeep buyer. Despite being a decent vehicle, it never really found its place — but now that Jeep is offering nearly $17,000 off select models, it might be time to give the go-fast Wagoneer S a second look.

Whether we’re talking about Mercedes-Benz, Cerberus, Fiat, or even Enzo Ferrari, there have been no shortage of corporate outsiders have labeled Jeep as a potentially premium brand that could, “if managed properly,” command luxury-level prices all over the globe. That hasn’t happened, and Stellantis is just the latest in a long line of companies to sink massive capital into the brand only to realize that people will not, in fact, spend Mercedes money on a Jeep.

“Stellantis bet big on electric versions of iconic American brands like Jeep and Dodge, but consumers aren’t buying the premise,” wrote CDG’s Marcus Amick, back in June. “(Stellantis’ dealer body) is now stuck with expensive EVs that need huge discounts to move, eating into already thin margins while competitors focus on [more] profitable gas-powered vehicles.”

To get its prices back in line with the market’s expectations, Jeep is slashing prices with lots of cash on the hood. That includes a hefty $15,250 incentive on select Wagoneer S trims listed as a “2025 National EV Credit Select Inventory Retail Bonus Cash” offer by Greenville Chrysler in Greenville, Texas — which seems like it would be stackable with $1,500 in National Stellantis Loyalty Retail Bonus Cash as well, for a total of $16,750 in incentives before any additional dealer discounts come into play.

All of which is to say: if you’ve found yourself drawn to the Jeep Wagoneer S, but couldn’t quite stomach the $70,000+ window stickers, you might want to check in with your local Jeep dealer and see how you feel about it at a JCPenneys-like 30% off!

Original content from Electrek.

If you’re considering going solar, it’s always a good idea to get quotes from a few installers. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024