Google, Meta, Amazon and other tech companies have laid off more than 95,000 employees in the last year

Sundar Pichai, CEO, Alphabet

Lluis Gene | AFP | Getty Images

The job cuts in tech land are piling up, as companies that led the 10-year bull market adapt to a new reality.

In January, Google announced plans to lay off 12,000 people from its workforce, while Microsoft said it’s letting go of 10,000 employees. Amazon also began a fresh round of job cuts that are expected to eliminate more than 18,000 employees and become the largest workforce reduction in the e-retailer’s 28-year history.

related investing news

On Tuesday, Meta announced plans to lay off 10,000 workers, adding to the 11,000 cuts it made in November.

The layoffs come in a period of slowing growth, higher interest rates to battle inflation, and fears of a possible recession next year.

Here are some of the major cuts in the tech industry so far. All numbers are approximations based on filings, public statements and media reports:

Alphabet: 12,000 jobs cut

Google, owned by parent company Alphabet, said Friday it will lay off 12,000 people from its workforce.

Sundar Pichai, Google’s CEO, said in an email sent to the company’s staff that the firm will begin making layoffs in the U.S. immediately. In other countries, the process “will take longer due to local laws and practices,” he said. CNBC reported in November that Google employees had been fearing layoffs as its counterparts made cuts and as employees saw changes to the company’s performance ratings system.

Alphabet had largely avoided layoffs until January, when it cut about 240 employees from Verily, its health sciences division.

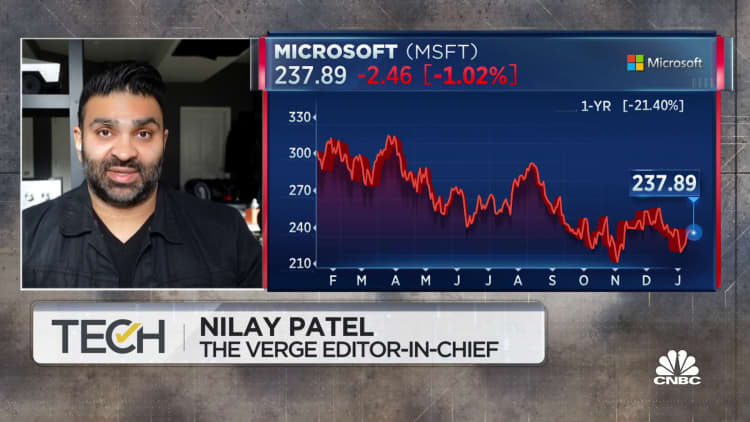

Microsoft: 10,000 jobs cut

Microsoft is reducing 10,000 workers through March 31 as the software maker braces for slower revenue growth. The company also is taking a $1.2 billion charge.

“I’m confident that Microsoft will emerge from this stronger and more competitive,” CEO Satya Nadella announced in a memo to employees that was posted on the company website Wednesday. Some employees will find out this week if they’re losing their jobs, he wrote.

Amazon: 18,000 jobs cut

Earlier this month, Amazon CEO Andy Jassy said the company was planning to lay off more than 18,000 employees, primarily in its human resources and stores divisions. It came after Amazon said in November it was looking to cut staff, including in its devices and recruiting organizations. CNBC reported at the time that the company was looking to lay off about 10,000 employees.

Amazon went on a hiring spree during the Covid-19 pandemic. The company’s global workforce swelled to more than 1.6 million by the end of 2021, up from 798,000 in the fourth quarter of 2019.

Crypto.com: 500 jobs cut

Crypto.com announced plans to lay off 20% of its workforce Jan. 13. The company had 2,450 employees, according to PitchBook data, suggesting around 490 employees were laid off.

CEO Kris Marszalek said in a blog post that the crypto exchange grew “ambitiously” but was unable to weather the collapse of Sam Bankman-Fried’s crypto empire FTX without the further cuts.

“All impacted personnel have already been notified,” Marszalek said in a post.

Coinbase: 2,000 jobs cut

On Jan. 10, Coinbase announced plans to cut about a fifth of its workforce as it looks to preserve cash during the crypto market downturn.

The exchange plans to cut 950 jobs, according to a blog post. Coinbase, which had roughly 4,700 employees as of the end of September, had already slashed 18% of its workforce in June saying it needed to manage costs after growing “too quickly” during the bull market.

“With perfect hindsight, looking back, we should have done more,” CEO Brian Armstrong told CNBC in a phone interview at the time. “The best you can do is react quickly once information becomes available, and that’s what we’re doing in this case.”

Dell: 6,650 jobs cut

Dell announced it would lay off 5% of its workforce, or about 6,650 employees, in early February. The company began the year with more than 130,000 employees, but said that the cuts were made to “stay ahead of downturn impacts.”

Slowing demand for PCs hit Dell harder than its competitors.

eBay: 500 jobs cut

eBay announced it would lay off 500 workers, or 4% of its headcount, in February. Like many executives, eBay CEO Jamie Iannone said that the cuts came as a result of the global macroeconomic environment.

Salesforce: 7,000 jobs cut

Salesforce is cutting 10% of its personnel and reducing some office space as part of a restructuring plan, the company announced Jan. 4. It employed more than 79,000 workers as of December.

In a letter to employees, co-CEO Marc Benioff said customers have been more “measured” in their purchasing decisions given the challenging macroeconomic environment, which led Salesforce to make the “very difficult decision” to lay off workers.

Salesforce said it will record charges of $1 billion to $1.4 billion related to the headcount reductions, and $450 million to $650 million related to the office space reductions.

Meta: 21,000 jobs cut

Facebook parent Meta announced its most significant round of layoffs ever in November. The company said it plans to eliminate 13% of its staff, which amounts to more than 11,000 employees.

Just four months later, CEO Mark Zuckerberg said the company would lay off an additional 10,000 employees and close hiring for 5,000 positions in a March message to employees.

Meta‘s disappointing guidance for the fourth quarter of 2022 wiped out one-fourth of the company’s market cap and pushed the stock to its lowest level since 2016.

The tech giant’s cuts come after it expanded headcount by about 60% during the pandemic. The business has been hurt by competition from rivals such as TikTok, a broad slowdown in online ad spending and challenges from Apple’s iOS changes.

Twilio: 1,500 jobs cut

In February, Twilio said it would lay off 17% of its workforce, or around 1,500 employees. The company reported nearly 9,000 employees in Sep. 2022. and had already laid off 11% of its workforce that same month.

“These changes hurt,” Twilio CEO Jeff Lawson said at the time.

Twitter: 3,700 jobs cut

Lyft: 700 jobs cut

Lyft announced in November that it cut 13% of its staff, or about 700 jobs. In a letter to employees, CEO Logan Green and President John Zimmer pointed to “a probable recession sometime in the next year” and rising ride-share insurance costs.

For laid-off workers, the ride-hailing company promised 10 weeks of pay, health care coverage through the end of April, accelerated equity vesting for the Nov. 20 vesting date and recruiting assistance. Workers who had been at the company for more than four years will get an extra four weeks of pay, they added.

Stripe: 1,100 jobs cut

Online payments giant Stripe announced plans to lay off roughly 14% of its staff, which amounts to about 1,100 employees, in November.

CEO Patrick Collison wrote in a memo to staff that the cuts were necessary amid rising inflation, fears of a looming recession, higher interest rates, energy shocks, tighter investment budgets and sparser startup funding. Taken together, these factors signal “that 2022 represents the beginning of a different economic climate,” he said.

Stripe was valued at $95 billion last year, and reportedly lowered its internal valuation to $74 billion in July.

Shopify: 1,000 jobs cut

In July, Shopify announced it laid off 1,000 employees, which equals 10% of its global workforce.

In a memo to staff, CEO Tobi Lutke acknowledged he had misjudged how long the pandemic-driven e-commerce boom would last, and said the company is being hit by a broader pullback in online spending. Its stock price is down 78% in 2022.

Netflix: 450 jobs cut

Netflix announced two rounds of layoffs. In May, the streaming service eliminated 150 jobs after the company reported its first subscriber loss in a decade. In late June, it announced another 300 layoffs.

In a statement to employees, Netflix said, “While we continue to invest significantly in the business, we made these adjustments so that our costs are growing in line with our slower revenue growth.”

Snap: 1,000 jobs cut

In late August, Snap announced it laid off 20% of its workforce, which equates to more than 1,000 employees.

Snap CEO Evan Spiegel told employees in a memo that the company needs to restructure its business to deal with its financial challenges. He said the company’s quarterly year-over-year revenue growth rate of 8% “is well below what we were expecting earlier this year.”

Robinhood: 1,100 jobs cut

Retail brokerage firm Robinhood slashed 23% of its staff in August, after cutting 9% of its workforce in April. Based on public filings and reports, that amounts to more than 1,100 employees.

Robinhood CEO Vlad Tenev blamed “deterioration of the macro environment, with inflation at 40-year highs accompanied by a broad crypto market crash.”

Tesla: 6,000 jobs cut

In June, Tesla CEO Elon Musk wrote in an email to all employees that the company was cutting 10% of salaried workers. The Wall Street Journal estimated the reductions would affect about 6,000 employees, based on public filings.

“Tesla will be reducing salaried headcount by 10% as we have become overstaffed in many areas,” Musk wrote. “Note this does not apply to anyone actually building cars, battery packs or installing solar. Hourly headcount will increase.”

Zoom: 1,300 jobs cut

Video conferencing provider Zoom said in February it would cut 15% of its workforce, laying off 1,300 workers. “We didn’t take as much time as we should have to thoroughly analyze our teams or assess if we were growing sustainably,” Zoom CEO Eric Yuan said at the time.

Zoom’s explosive growth was fuelled by Covid-19 lockdowns, but the company has suffered as life has largely returned to normal for many.

Technology

Microsoft to invest $17.5 billion in India’s AI infra as Big Tech queues up for the Asian market

Justin McLeod speaks during the Fast Company Innovation Festival 2025 on Sept. 18, 2025 in New York City.

Eugene Gologursky | Getty Images

Hinge founder Justin McLeod is stepping down as CEO of the dating app to launch a dating service powered by artificial intelligence.

McLeod will be replaced by Jackie Jantos, the dating app’s president and chief marketing officer, Hinge parent company Match Group announced on Tuesday.

“The company’s momentum, including being on track to reach $1 billion in revenue by 2027, gives me full confidence in where Hinge is headed,” said McLeod in a statement. He created the dating app in 2011.

McLeod will remain as an advisor to Hinge through March. Overtone, his new venture, will use AI and voice tools to “help people connect in a more thoughtful and personal way,” according to the announcement.

Along with a dedicated team, McLeod spent much of this year developing the startup with support from Match Group, which said it plans to lead Overtone’s initial funding round in early 2026.

Match Group, which also owns Tinder and various other dating apps, will hold a significant ownership position in Overtone. Match Group CEO Spencer Rascoff will join Overtone’s board.

“We’re proud to have incubated Overtone within Hinge and to now lead its funding round as he builds his next venture,” Rascoff said in a statement.

WATCH: Software could start benefitting from AI in 2026, says Intelligent Alpha CEO Doug Clinton

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024