Budget 2023: UK economy will avoid recession in 2023 and inflation set to plummet, says chancellor

Jeremy Hunt said the British economy is “proving the doubters wrong” and will avoid recession, as he delivered his first full budget speech to Parliament.

The chancellor said the government’s plan for the economy was “working” as he announced what he called a “budget for growth”.

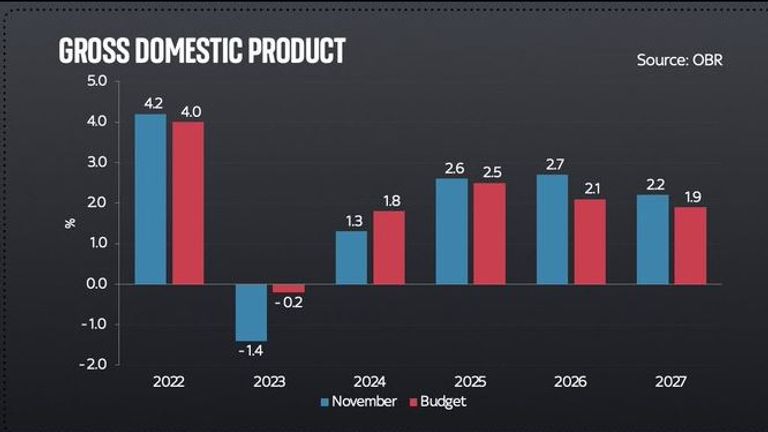

He said forecasts from the Office for Budget Responsibility (OBR) showed the UK would avoid recession – two-quarters of negative growth – in 2023, despite previous predictions.

But the economy will still contract overall this year by 0.2%, and the OBR has warned living standards are still expected to fall by the largest amount since records began – although the decline is not as bad as had been forecast in November.

Budget 2023 – read more:

Politics live: The budget as it happened and reaction

The key points of the budget at a glance

The OBR forecasts also said inflation in the UK would fall from 10.7% in the final quarter of last year to 2.9% by the end of 2023.

Mr Hunt said it showed Rishi Sunak’s goal of halving inflation this year would be met, but he added: “We remain vigilant and will not hesitate to take whatever steps are necessary for economic stability”.

However, Labour leader Sir Keir Starmer said the chancellor’s “boasts” about lower inflation were “ridiculous”, adding: “The idea that it’s a tax cut, British people can see through that.

“They see their tax burden at its highest level for 70 years and they know it’s not the government that’s lowering inflation.

“It’s working people, earning less, enjoying less. It’s their sacrifice that is helping to bring inflation down and they deserve better than another cheap trick from the government of gimmicks, making them pay whilst trying to claim the credit.”

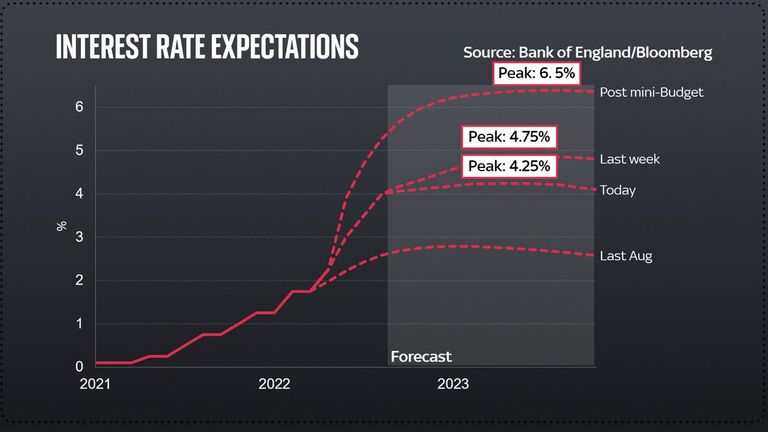

Interest Rate Expectations

A number of other plans were unveiled by Mr Hunt, including:

• Bringing charges for prepayment meters in line with direct debit charges, impacting over four million households and saving them an average of £45 per year

• Making duty on draught products in pubs up to 11p lower than supermarkets

• Maintaining the freeze in fuel duty

The chancellor also said £11bn will be added to the defence budget over the next five years – following an announcement earlier this week – saying it would be nearly 2.25% of GDP by 2025. The government’s ambition is for it to reach 2.5%, he added.

And after reports he would increase the pensions lifetime allowance to £1.8m in an attempt to encourage doctors and other high earners back to work, Mr Hunt decided to scrap the limit entirely, as well as increasing the pensions annual tax-free allowance from £40,000 to £60,000.

He told the Commons: “In the face of enormous challenges I report today on a British economy which is proving the doubters wrong.

“In the autumn we took difficult decisions to deliver stability and sound money. Since mid-October, 10-year gilt rates have fallen, debt servicing costs are down, mortgage rates are lower and inflation has peaked.

“The International Monetary Fund says our approach means the UK economy is on the right track.”

But Sir Keir said the only permanent tax cut in the budget was for “the richest 1%”, adding: “How can that possibly be a priority for this government?”

‘This a failure you can measure not just in the figures but in the empty pockets of working people,’ says the Labour leader.

The Labour leader continued: “Again we see a failure to grip the long-term challenges. No determination to create growth that unlocks the potential of the many – working people being made to pay for Tory choices and Tory mistakes.”

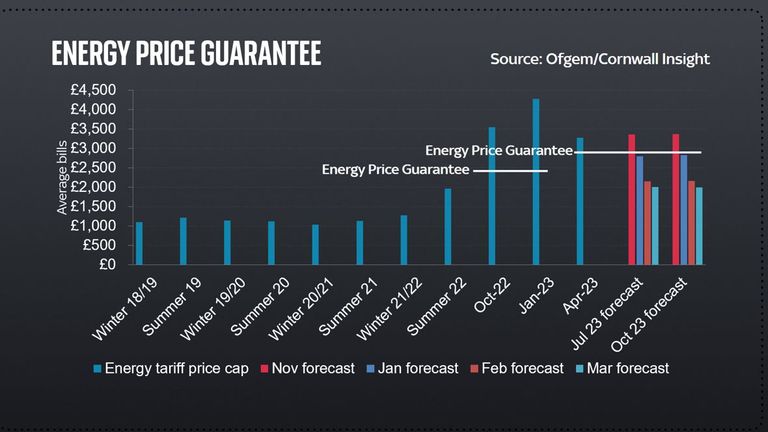

Some policies were revealed ahead of the chancellor’s speech, including keeping the cap on energy prices at £2,500 for a further three months, despite a planned rise to £3,000 in April, and 12 new investment zones.

Sky News also reported last night his promise to provide 30 hours of childcare a week to parents of one and two-year-olds, and to give a further cash injection to the sector to increase the availability of existing free childcare for three to four-year-olds.

But Mr Hunt went further on this measure, saying the care would be available from September 2024 when a child reaches nine months, as well as promising to increase funding for nurseries and pay those on Universal Credit upfront for the childcare they need to get.

However, he also confirmed the ratio for how many children each staff member looks after can be raised from one per four to one per five – though he said it was optional for both providers and parents.

There were more announcements to fit with Mr Hunt’s “three E’s” philosophy – enterprise, employment and education.

They included:

• Incentive payments of up to £1,200 for childminders who sign up to the profession

• Enhanced credit for small and medium businesses, and creative firms

• An extension to relief for theatres, orchestras and museums

• Tax relief on energy efficient measures in firms

• £900m investment into supercomputing

The chancellor also confirmed widely reported plans to abolish the Work Capability Assessment for disabled people to “separate benefit entitlement from an individual’s ability to work”.

Mr Hunt promised a new programme called Universal Support, describing it as “a new, voluntary employment scheme for disabled people where the government will spend up to £4,000 per person to help them find appropriate jobs and put in place the support they need”.

And he said there would be a £400m fund to help those who are forced to leave work because of a health condition to get support in the workplace.

Chancellor Jeremy Hunt MP has announced that the energy price guarantee will remain at £2,500 until the end of June.

Mr Hunt confirmed he would keep the incoming rise in corporation tax – from 19% to 25% – despite anger from some of his own backbenchers.

But in a bid to keep businesses happy, he introduced a new benefit where every pound a company invests in equipment can be deducted in full and immediately from taxable profits – “a corporation tax cut worth an average of £9bn a year for every year it is in place”.

In what appeared to echo recent Labour policy, the chancellor announced continued state-financed investment in nuclear power and the launch of Great British Nuclear, saying the public body will “bring down costs and provide opportunities across the nuclear supply chain to help provide up to one quarter of our electricity by 2050”.

And he said nuclear energy would be reclassified as “environmentally sustainable” to give it the same access to investment incentives as renewables.

Today’s statement was Mr Hunt’s first full budget as chancellor – having been brought in by Liz Truss to reverse a number of measures from her disastrous mini-budget last October and kept on by Rishi Sunak after he took over as prime minister.

It came against a backdrop of mass industrial action, with hundreds of thousands of workers today staging what is believed to be the biggest walkout since the current wave of unrest began.

Teachers, university lecturers, civil servants, junior doctors, London Underground drivers and BBC journalists are among those taking to picket lines around the country amid widespread anger over pay, job security, pensions and conditions.

Labour’s shadow chancellor, Rachel Reeves, said ahead of the budget that it was “an opportunity for the government to get us off their path of managed decline”.

She added, if her party were in power, their focus would be on securing the highest growth in the G7.

“Our plan will help us lead the pack again, by creating good jobs and productivity growth across every part of our country, so everyone, not just a few, feel better off,” she added.

Our politics, business and finance reporters will be hosting a Q&A after the budget statement. To submit a question, click here.

Business

Post Office scandal: Victims say government’s control of redress schemes should be taken away

Post Office scandal victims are calling for redress schemes to be taken away from the government completely, ahead of the public inquiry publishing its first findings.

Phase 1, which is due back on Tuesday, will report on the human impact of what happened as well as compensation schemes.

“Take (them) off the government completely,” says Jo Hamilton OBE, a high-profile campaigner and former sub-postmistress, who was convicted of stealing from her branch in 2008.

“It’s like the fox in charge of the hen house,” she adds, “because they were the only shareholders of Post Office“.

“So they’re in it up to their necks… So why should they be in charge of giving us financial redress?”

Nearly a third of Ms Hamilton’s life has been dominated by the scandal

Jo and others are hoping Sir Wyn Williams, chairman of the public statutory inquiry, will make recommendations for an independent body to take control of redress schemes.

The inquiry has been examining the Post Office scandal which saw more than 700 people wrongfully convicted between 1999 and 2015.

Sub-postmasters were forced to pay back false accounting shortfalls because of the faulty IT system, Horizon.

At the moment, the Department for Business and Trade administers most of the redress schemes including the Horizon Conviction Redress Scheme and the Group Litigation Order (GLO) Scheme.

The Post Office is still responsible for the Horizon Shortfall scheme.

Lee Castleton OBE

Lee Castleton OBE, another victim of the scandal, was bankrupted in 2007 when he lost his case in the civil courts representing himself against the Post Office.

The civil judgment against him, however, still stands.

“It’s the oddest thing in the world to be an OBE, fighting for justice, while still having the original case standing against me,” he tells Sky News.

While he has received an interim payment he has not applied to a redress scheme.

“The GLO scheme – that’s there on the table for me to do,” he says, “but I know that they would use my original case, still standing against me, in any form of redress.

“So they would still tell me repeatedly that the court found me to be liable and therefore they only acted on the court’s outcome.”

He agrees with other victims who want the inquiry this week to recommend “taking the bad piece out” of redress schemes.

“The bad piece is the company – Post Office Limited,” he continues, “and the government – they need to be outside.

“When somebody goes to court, even if it’s a case against the Department for Business and Trade (DBT), when they go to court DBT do not decide what the outcome is.

“A judge decides, a third party decides, a right-minded individual a fair individual, that’s what needs to happen.”

Pic: AP

Mr Castleton is also taking legal action against the Post Office and Fujitsu – the first individual victim to sue the organisations for compensation and “vindication” in court.

“I want to hear why it happened, to hear what I believe to be the truth, to hear what they believe to be the truth and let the judge decide.”

Neil Hudgell, a lawyer for victims, said he expects the first inquiry report this week may be “really rather damning” of the redress claim process describing “inconsistencies”, “bureaucracy” and “delays”.

“The over-lawyeringness of it,” he adds, “the minute analysis, micro-analysis of detail, the inability to give people fully the benefit of doubt.

“All those things I think are going to be part and parcel of what Sir Wynn says about compensation.

“And we would hope, not going to say expect because history’s not great, we would hope it’s a springboard to an acceleration, a meaningful acceleration of that process.”

June: Post Office knew about faulty IT system

A Department for Business and Trade spokesperson said they were “grateful” for the inquiry’s work describing “the immeasurable suffering” victims endured.

Their statement continued: “This government has quadrupled the total amount paid to affected postmasters to provide them with full and fair redress, with more than £1bn having now been paid to thousands of claimants.

“We will also continue to work with the Post Office, who have already written to over 24,000 postmasters, to ensure that everyone who may be eligible for redress is given the opportunity to apply for it.”

Octopus Energy Group, Britain’s largest residential gas and electricity supplier, is plotting a £10bn demerger of its technology arm that would reinforce its status as one of the country’s most valuable private companies.

Sky News can exclusively reveal that Octopus Energy is close to hiring investment bankers to help formally separate Kraken Technologies from the rest of the group.

The demerger, which would be expected to take place in the next 12 months, would see Octopus Energy’s existing investors given shares in the newly independent Kraken business.

A minority stake in Kraken of up to 20% is expected to be sold to external shareholders in order to help validate the technology platform’s valuation, according to insiders.

One banking source said that Kraken could be valued at as much as $14bn (£10.25bn) in a forthcoming demerger.

Citi, Goldman Sachs, JP Morgan and Morgan Stanley are among the investment banks invited to pitch for the demerger mandate in recent weeks.

A deal will augment Octopus Energy chief executive Greg Jackson’s paper fortune, and underline his success at building a globally significant British-based company over the last decade.

Octopus Energy now has 7.5m retail customers in Britain, following its 2022 rescue of the collapsed energy supplier Bulb, and the subsequent acquisition of Shell’s home energy business.

In January, it announced that it had become the country’s biggest supplier – surpassing Centrica-owned British Gas – with a 24% market share.

It also has a further 2.5m customers outside the UK.

Kraken is an operating system licensed to other energy providers, water companies and telecoms suppliers. Pic: Octopus

Sources said a £10bn valuation of Kraken would now imply that the whole group, including the retail supply business, was worth in the region of £15bn or more.

That would be double its valuation of just over a year ago, when the company announced that it had secured new backing from funds Galvanize Climate Solutions and Lightrock.

Shortly before that, former US vice president Al Gore’s firm, Generation Investment Management, and the Canada Pension Plan Investment Board increased their stakes in Octopus Energy in a transaction valuing the company at $9bn (£7.2bn).

Kraken is an operating system which is licensed to other energy providers, water companies and telecoms suppliers.

It connects all parts of the energy system, including customer billing and the flexible management of renewable generation and energy devices such as heat pumps and electric vehicle batteries.

The business also unlocks smart grids which enable people to use more renewable energy when there is an abundant supply of it.

In the UK, its platform is licensed to Octopus Energy’s rivals EON and EDF Energy, as well as the water company Severn Trent and broadband provider Cuckoo.

Overseas, Kraken serves Origin Energy in Australia, Japan’s Tokyo Gas and Plentitude in countries including France and Greece.

Its biggest coup came recently, when it struck a deal with National Grid in the US to serve 6.5m customers in New York and Massachusetts.

Sources said other major licensing agreements in the US were expected to be struck in the coming months.

Kraken, which is chaired by Gavin Patterson, the former BT Group chief executive, is now contracted to more than 70m customer accounts globally – putting it easily on track to hit a target of 100m by 2027.

Earlier this year, Mr Jackson said that target now risked being seen as “embarrassingly unambitious”.

Last July, Kraken recruited Amir Orad, a former boss of NICE Actimize, a US-listed provider of enterprise software to global banks and Fortune 500 companies, as its first chief executive.

A demerger of Kraken will trigger speculation about an eventual public market listing of the business.

Its growth in the US, and the relative public market valuations of technology companies in New York and London, may put the UK at a disadvantage when Kraken eventually considers where to list.

One key advantage of demerging Kraken from the rest of Octopus Energy Group would be to remove the perception of a conflict of interest among potential customers of the technology platform.

A source said the unified corporate ownership of both businesses had acted as a deterrent to some energy suppliers.

Kraken has also diversified beyond the energy sector, and earlier this year joined a consortium which was exploring a takeover bid for stricken Thames Water.

This weekend, Octopus Energy declined to comment.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike