We’re revising price targets on 5 Club stocks, adding a U.S. retailer to the bullpen and sticking with a key bank

Georgia BRIGHT, a statewide initiative to deliver affordable solar, kicked off its “No-Cost Solar Plan” in Atlanta yesterday, giving qualified homeowners a shot at roughly 400 fully prepaid rooftop-solar systems with zero upfront or maintenance costs. However, Georgia Bright’s No-Cost Solar Plan may lose its $156 million in grant money if the EPA steals back the Solar for All program’s entire $7 billion, which funded it.

On Earth Day (April 22) 2024, the Georgia BRIGHT Communities Coalition, including lead applicant Capital Good Fund, along with coalition member cities, Atlanta, Savannah, and Decatur, and dozens of other Georgia stakeholders, was allocated $156 million from Solar for All to bring solar to thousands of households statewide between now and mid-2029.

Families that earn 80% or less of their county’s Area Median Income can enter a drawing for the No-Cost Solar Plan now; a second drawing for another 400 systems is set for spring 2026.

“As the cost of living increases across our most vulnerable communities, this program will deliver significant savings to the households that need it most,” said Alicia Brown, director of Georgia BRIGHT.

Those savings are already showing up. Pilot participant Christine Difeliciantonio saw her power bill plunge on her Columbus home from $224 in June 2024 to $50 in June 2025 after her panels came online, and she says the added resilience eases her mind during storms.

Nonprofits are benefiting, too. Trees Atlanta had 140 panels installed on their headquarters last November in the pilot program; the rooftop array went live in March and is on track to save about $3,000 a year, the carbon equivalent of planting 28,000 trees over 25 years.

What’s next for Georgia BRIGHT …

Georgia BRIGHT’s other programs in the works include its Residential Solar Savings Plan, offering custom rooftop installs with no upfront cost and guaranteeing households at least 20% savings on day one after factoring in the modest monthly payments. Georgia BRIGHT is also developing Community Benefit Solar, which lets businesses, houses of worship, and apartment buildings go solar so long as they share part of the financial benefits – think grocery gift cards, help with utility bills, discounted daycare, or rent relief – with eligible neighbors for five years. Finally, a Utility-Led Community Solar initiative will send grants to local utilities so they can run shared-solar programs designed specifically for low-income customers.

These programs really make a difference in a state like Georgia, which doesn’t offer any other solar incentives.

… if the EPA doesn’t steal its money

The New York Times reported today that the Trump-led EPA is drafting letters to claw back the entire $7 billion Solar for All pot from 49 states, plus 11 nonprofit groups and Native American tribes. The grant money was awarded under President Biden’s 2022 Inflation Reduction Act. According to the Times‘ sources, the EPA plans to send termination notices this week, effectively erasing solar savings for nearly a million low-income families before the panels ever land on their roofs.

Legal groups are already gearing up for the fight. “If leaders in the Trump administration move forward with this unlawful attempt to strip critical funding from communities across the United States, we will see them in court,” Kym Meyer of the Southern Environmental Law Center told the Times.

If the EPA pulls the trigger on this cruel, senseless plan to steal solar from lower-income communities, it wouldn’t just kneecap Georgia’s new program – it would pull the rug out from under low-income solar projects nationwide. The fight over Solar for All is officially on. How about that energy emergency that Trump declared, eh?

Read more: This metro Atlanta factory roof is now a solar record-breaker

The 30% federal solar tax credit is ending this year. If you’ve ever considered going solar, now’s the time to act. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

Tesla is in trouble, facing down hundreds of millions in fines on a single Autopilot wrongful death claim, accusations of covering up evidence, and plummeting sales in Europe, China, and the US. But, hey – that’s no reason to NOT give Elon a $29 billion bonus, right? Find out more on today’s troubling episode of Quick Charge!

We’re also helping Costco celebrate the first half-birthday of its EV marketplace, where you can get a great deal on a new Chevy Silverado EV capable of going more than one thousand miles on a single charge [insert 400 pages of fine print and disclaimers here –Ed.].

Today’s episode is brought to you by Retrospec, the makers of sleek, powerful e-bikes and outdoor gear built for everyday adventure. Quick Charge listeners can get an extra 10% off their next ride until August 14 with the exclusive code ELECTREK10, only at retrospec.com.

Source Links

Prefer listening to your podcasts? Audio-only versions of Quick Charge are now available on Apple Podcasts, Spotify, TuneIn, and our RSS feed for Overcast and other podcast players.

New episodes of Quick Charge are recorded, usually, Monday through Thursday (most weeks, anyway). We’ll be posting bonus audio content from time to time as well, so be sure to follow and subscribe so you don’t miss a minute of Electrek’s high-voltage daily news.

Got news? Let us know!

Drop us a line at tips@electrek.co. You can also rate us on Apple Podcasts and Spotify, or recommend us in Overcast to help more people discover the show.

BLUETTI portable power stations offer enough capacity to run power tools, appliances, or even serve as a full-home backup during outages. For extended outages, BLUETTI offers modular systems can keep your fridge, lights, or Wi-Fi going for days. And, if you’re traveling light, the new Handsfree line of backpack power stations offer plug-and-play energy on the go — perfect for remote work, camping, or emergencies.

FTC: We use income earning auto affiliate links. More.

cuts production target for 2025, but there's more to it")

Lucid Group (LCID) lowered its production goal for 2025, citing a changing market environment. Despite missing second-quarter expectations, the EV maker still has ambitious growth plans.

Why is Lucid lowering its 2025 production guidance?

After reporting Q2 earnings on Tuesday, Lucid said it now expects to produce around 18,000 to 20,000 vehicles, down from the previous 20,000 it had previously maintained.

The company said the updated production target reflects “the potential impact of continuously changing market environment and external factors.”

Despite reporting record revenue of $259.4 million, it missed Wall Street’s expectations of around $280 million. Lucid posted a net loss of $790 million, or 0.34 per share. With an adjusted loss per share of 0.24, the company also missed bottom-line estimates of a 0.21 loss per share.

Lucid ended the quarter with $4.86 billion in total liquidity, including $3.63 billion in cash, cash equivalents, and investments.

The reserve provides “ample flexibility,” according to Lucid, to fund operations, scale Gravity production, and invest in future platforms.

Lucid confirmed that it believes the liquidity is sufficient to fund it through the second half of 2026, when it will begin production of its midsize platform. The platform will have at least three “top hats,” including an expected midsize SUV and sedan. With prices starting at around $50,000, Lucid’s midsize models are expected to compete with the Tesla Model Y and Model 3.

Last month, Lucid announced a partnership with Uber and Nuro to deploy 20,000 electric robotaxis over the next six years. Uber will invest $300 million in Lucid as part of the collaboration.

It’s also expanding awareness with the addition of a new brand ambassador, Timothée Chalamet. The multi-year partnership will launch with a new advertising campaign this fall.

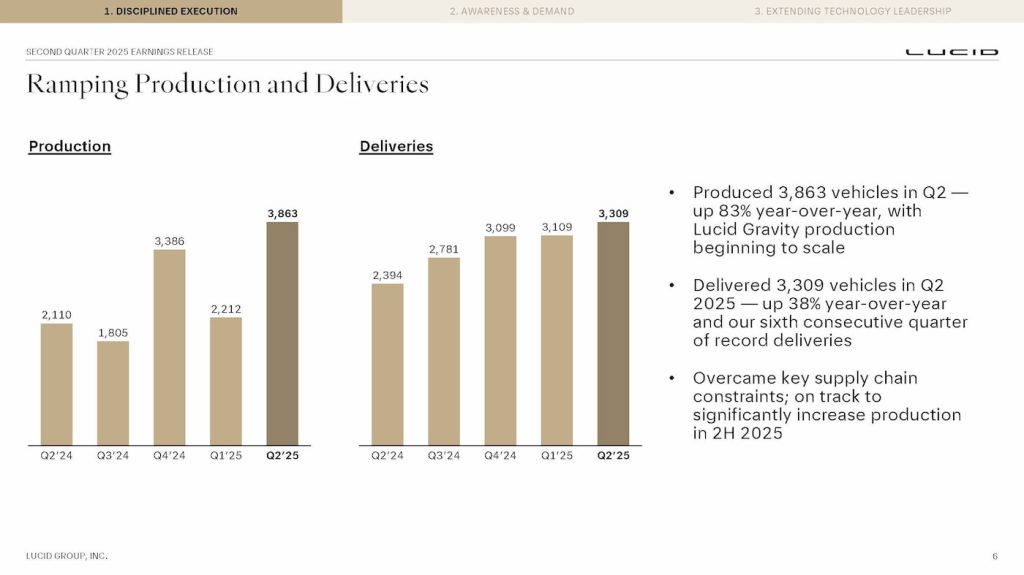

Despite lowering its full-year production goal, Lucid achieved its sixth consecutive quarter of record deliveries. Lucid delivered 3,309 vehicles in Q2 and produced 3,863 at its Casa Grande, Arizona, plant.

Despite the lower forecast, Lucid said it’s still “on track to significantly increase production” in the second half of 2025.

Like most auto brands, Lucid is preparing for a shakeup under the Trump Administration. However, Lucid already builds most components in the US, including the battery and powertrain. It’s also expanding its supply chain with new partnerships for domestic EV resources such as Graphite.

FTC: We use income earning auto affiliate links. More.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike