Google reshuffles virtual assistant unit with focus on Bard A.I. technology

Google CEO Sundar Pichai speaks on stage during the annual Google I/O developers conference in Mountain View, California, May 8, 2018.

Stephen Lam | Reuters

Google is reshuffling the reporting structure of its virtual assistant unit — called Assistant — to focus more on Bard, the company’s new artificial intelligence chat technology.

In a memo to employees on Wednesday, titled “Changes to Assistant and Bard teams,” Sissie Hsiao, vice president and lead of Google Assistant’s business unit, announced changes to the organization that show the unit heavily prioritizing Bard.

Jianchang “JC” Mao, who reported directly to Hsiao, will be leaving the company for personal reasons, according to the memo, which was viewed by CNBC. Mao held the position of vice president of engineering for Google Assistant and “helped shape the Assistant we have today,” Hsiao wrote.

Taking Mao’s place will be 16-year Google veteran Peeyush Ranjan, who most recently held the title of vice president in Google’s commerce organization, overseeing payments.

“As the Bard teams continue this work, we want to ensure we continue to support and execute on the opportunities ahead,” Hsiao said in the email. “This year, more than ever, we have been focused on delivery with impact to our users.”

Google Assistant is an AI-powered virtual assistant software application and language-processing software similar to Apple’s Siri or Amazon’s Alexa. Often in the form of speech recognition, Assistant is used on mobile and home devices, including its Pixel smartphone and in Nest smart speakers and devices. It’s also used in smart watches, smart displays, TVs and in vehicles through the Android Auto platform.

The new leadership changes suggest that the Assistant organization may be planning on integrating Bard technology into similar products in the future.

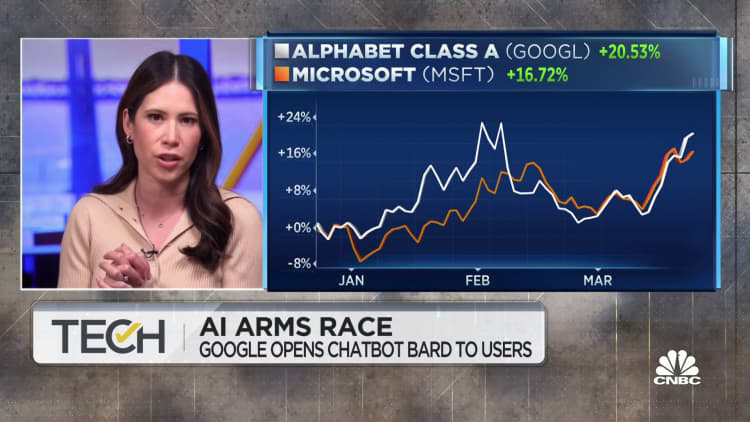

Last week, Google launched its ChatGPT competitor Bard to the public, calling it “an experiment,” starting with tests in the U.S. and the U.K. after CNBC reported the product testing in January. CNBC previously reported that the company pulled team members from various areas around the company to focus on Bard as a part of a “code red” effort.

As part of Wednesday’s change, Google Assistant engineering vice president Amar Subramanya will now lead engineering for the Bard team, the email said. Trevor Strohman, who previously led engineering efforts for Bard, will continue as an “Area Tech Lead” for Bard, reporting to Hsiao.

However, there’s still a big question regarding how the technology can be used to generate revenue.

Executives have hinted at using it as a search product but Bard leads more recently tried to play down that use case to employees even as the company scrambled to respond to Microsoft’s Bing Chat-GPT integration.

Google didn’t immediately respond to a request for comment.

WATCH: AI arms race

Technology

Amazon CEO Jassy says AI will lead to ‘fewer people doing some of the jobs’ that get automated

Amazon CEO Andy Jassy said the rapid rollout of generative artificial intelligence means the company will one day require fewer employees to do some of the work that computers can handle.

“Like with every technical transformation, there will be fewer people doing some of the jobs that the technology actually starts to automate,” Jassy told CNBC’s Jim Cramer in an interview on Monday. “But there’s going to be other jobs.”

Even as AI eliminates the need for some roles, Amazon will continue to hire more employees in AI, robotics and elsewhere, Jassy said.

Earlier this month, Jassy admitted that he expects the company’s workforce to decline in the next few years as Amazon embraces generative AI and AI-powered software agents. He told staffers in a memo that it will be “hard to know exactly where this nets out over time” but that the corporate workforce will shrink as Amazon wrings more efficiencies out of the technology.

It’s a message that’s making its way across the tech sector. Salesforce CEO Marc Benioff last week claimed AI is doing 30% to 50% of the work at his software vendor. Other companies such as Shopify and Microsoft have urged employees to adopt the technology in their daily work. The CEO of Klarna said in May that the online lender has managed to shrink its headcount by about 40%, in part due to investments in AI and natural attrition in its workforce.

Jassy said on Monday that AI will free employees from “rote work” and “make all our jobs more interesting,” while enabling staffers to invent better services more quickly than before.

Amazon and other tech companies have also been shrinking their workforces through rolling layoffs over the past several years. Amazon has cut more than 27,000 jobs since the start of 2022, and it’s announced smaller, more targeted layoffs in its retail and devices units in recent months.

Amazon shares are flat so far this year, underperforming the Nasdaq, which has gained 5.5%. The stock is about 10% below its record reached in February, while fellow megacaps Meta, Microsoft and Nvidia are all trading at or very near record highs.

WATCH: Jassy says robots that will eventually do delivery and transportation

Mark Zuckerberg, chief executive officer of Meta Platforms Inc., during the Meta Connect event on Wednesday, Sept. 25, 2024.

Bloomberg | Bloomberg | Getty Images

Meta shares hit a record high on Monday, underscoring investor interest in the company’s new AI superintelligence group.

The company’s shares reached $747.90 during midday trading, topping Meta’s previous stock market record in February when it began laying off the 5% of its workforce that it deemed “low performers.”

Meta joins Microsoft and Nvidia among tech megacaps that have reached new highs of late, all closing at records Monday. Apple, Amazon, Alphabet and Tesla remain below their all-time highs reached late last year or early this year.

Meta CEO Mark Zuckerberg has been on an AI hiring blitz amid fierce competition with rivals such as OpenAI and Google parent Alphabet. Earlier in June, Meta said it would hire Scale AI CEO Alexandr Wang and some of his colleagues as part of a $14.3 billion investment into the executive’s data labeling and annotation startup.

The social media company also hired Nat Friedman and his business partner, Daniel Gross, the chief of Safe Superintelligence, an AI startup with a valuation of $32 billion, CNBC reported on June 19. Meta’s attempts to buy Safe Superintelligence were rebuffed by the startup’s founder and AI expert Ilya Sutskever, the report noted.

Wang and Friedman are the leaders of Meta’s new Superintelligence Labs, tasked with overseeing the company’s artificial intelligence foundation models, projects and research, a person familiar with the matter told CNBC. The term superintelligence refers to technology that exceeds human capability.

Bloomberg News first reported about the new superintelligence unit.

Meta has also snatched AI researchers from OpenAI. Sam Altman, OpenAI’s CEO, said during a podcast that Meta was offering signing bonuses as high as $100 million.

Andrew Bosworth, Meta’s technology chief, spoke about the social media company’s AI hiring spree during a June 20 interview with CNBC’s “Closing Bell Overtime,” saying that the talent market is “really incredible and kind of unprecedented in my 20-year career as a technology executive.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike