Q1 2023 earnings preview: What to expect today")

Tesla (TSLA) Q1 2023 earnings preview: What to expect today

Tesla (TSLA) is about to release Q1 2023 financial results today, Wednesday, April 19, after the markets close. As usual, a conference call and Q&A with Tesla’s management are scheduled after the results.

Here we’ll take a look at what both the street and retail investors are expecting for the quarterly results.

Tesla Q1 2023 deliveries

As usual, Tesla already disclosed its Q1 vehicle delivery and production numbers, which drive the vast majority of the company’s revenue.

Earlier this month, Tesla confirmed that it delivered a new record of over 422,000 electric vehicles during the first quarter of the year.

Tesla also confirmed having produced 440,000 vehicles during the quarter – also a new record.

Delivery and production numbers are always slightly adjusted during earning results.

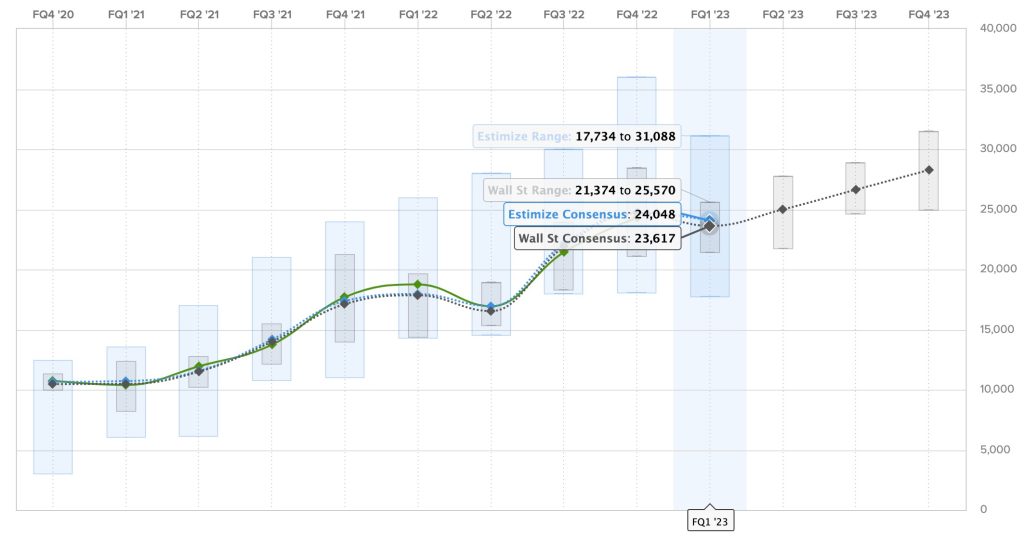

Tesla Q1 2023 revenue

For revenue, analysts generally have a pretty good idea of what to expect, thanks to the delivery numbers.

The Wall Street consensus for this quarter is $23.617 billion, and Estimize, the financial estimate crowdsourcing website, predicts a higher revenue of $24.048 billion.

Despite the new record number of deliveries, these estimates would represent a quarter-to-quarter decrease in revenue due to Tesla’s implementing large price cuts during the first quarter.

Nonetheless, it would be a massive year-over-year increase from $18 billion in revenue in Q1 2022.

Here are the predictions for Tesla’s revenue over the past two years, where Estimize predictions are in blue, Wall Street consensus is in gray, and actual results are in green:

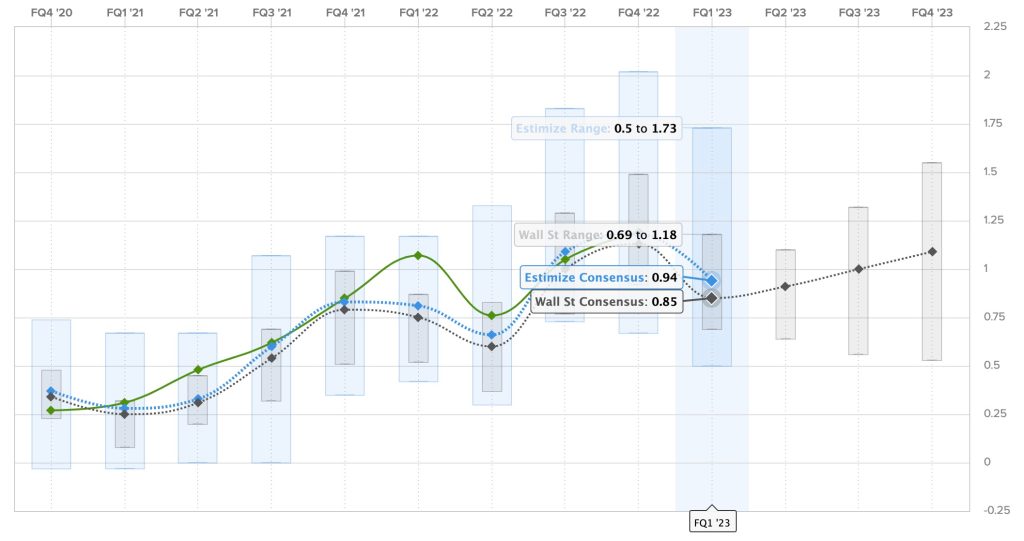

Tesla Q1 2023 earnings

Tesla always attempts to be marginally profitable every quarter as it invests most of its money into growth, and it has been successful in doing so over the last two years now.

For Q1 2023, the Wall Street consensus is a gain of $0.85 per share, while Estimize’s prediction is higher with a profit of $0.94 per share.

The estimates have a wide range this quarter because of the price cuts Tesla implemented during the quarter. Analysts and investors are looking to see how badly it is going to affect Tesla’s margins and, ultimately, its profits.

Unsurprisingly, Tesla achieving the Wall Street consensus would be a big drop in earnings quarter-to-quarter, and the automaker would be flat on earnings year-over-year.

Here are the earnings per share over the last two years, where Estimize predictions are in blue, Wall Street consensus is in gray, and actual results are in green:

Other expectations for the TSLA shareholder’s letter and analyst call

The obvious thing is the gross margin. Investors are going to be looking for that number first. They want to know by how much it dropped and how much room there is since Tesla continued to drop prices after the end of the quarter.

If Tesla can stay in the mid to high teens, I think investors will be happy, but if it dips lower than that, they might have a problem.

Investors will also be looking at insights from management about the pricing strategy, which seems to be changing fast.

Tesla shareholders will also be looking on an update on Cybertruck production as the start of production gets closer, but knowing Tesla management, I wouldn’t expect much more than it being on track for a start of production this summer and volume production next year.

Cybertruck should not have a material impact on Tesla’s revenue in 2023.

I assume that amid margins going down, Tesla investors are going to want to have an update on Tesla’s self-driving program, which has helped margins in the past, but the program has been stalling for a while now.

According to the Say website, where investors can ask and upvote questions for the meeting, shareholders are particularly interested in Tesla Energy this quarter and its potential future impact on Tesla’s financials.

It has been a growing business for Tesla and with a ramp-up in Megapack production, it should be bigger in Q1, but I wouldn’t expect a massive jump in deployment until the second half of the year.

We will see what Tesla has to say about that.

You can join us live on Electrek this evening for intensive coverage of Tesla’s Q1 2023 financial results starting at around 4 p.m. ET for the results and through the evening for news coming out of the conference call and results.

FTC: We use income earning auto affiliate links. More.

Chevy is celebrating America’s 250th anniversary with a patriotic lineup of special edition Stars & Steel models, including the electric Silverado EV pickup.

Meet the Chevy Silverado EV Stars & Steel edition

The new Stars & Steel collection is “a curated lineup of uniquely designed vehicles that embody purpose-driven patriotism and American craftsmanship,” Chevy said

Chevy is releasing five special-edition vehicles for 2026, including the Silverado EV, Corvette, Silverado LD, Silverado HD, and Colorado, in celebration of the country’s 250th anniversary.

Each vehicle is assembled in the US and will feature exclusive interior and exterior design elements, including American-flag-inspired graphics on the hood, as well as other premium options that “underscore patriotism,” according to Chevy.

The Silverado EV Stars & Steel Special Edition will be available on the RST Crew Cab trim. Buyers can choose from Summit White or Black exterior colors, while a Sky Cool Gray interior with bucket seats offers “a bold electric interpretation” of the Stars & Steel theme.

Every 2026 Chevy Silverado special edition model includes American Flag-inspired stripes in Satin Silver or Satin Black and “250” flag graphics.

Chevy also added 24″ high-gloss black wheels, black nameplates, and a new Brembo heavy-duty brake system with red-piston front calipers, and larger 15.7″ brake discs.

For every Stars & Steel vehicle sold, Chevy will donate $250 to nonprofits that support veterans. Be on the lookout as the collection will make its first public appearance this weekend during the Army-Navy game on Saturday, December 13, 2025.

A tribute to the roads that built us. Introducing the Stars & Steel Collection. pic.twitter.com/rKrz1NckpE

— Chevrolet (@chevrolet) December 10, 2025

Chevy said production of the new lineup is expected to begin in early spring 2026, and prices will be announced at a later date.

The 2026 Chevy Silverado EV offers an impressive driving range of up to 494 miles and can tow up to 12,500 lbs. It’s available in three trims: Custom, LT, and Trail Boss, starting at $55,895.

If you’re interested in test-driving the electric pickup, we can help you get started. You can use our link to find available 2026 Chevy Silverado EVs in your area.

FTC: We use income earning auto affiliate links. More.

Tesla CEO Elon Musk took to X (formerly Twitter) this morning to dismiss Waymo’s progress in autonomous driving, claiming that the Alphabet-owned company “never really had a chance against Tesla” and that this will be “obvious in hindsight.”

The comment came as a direct response to a discussion about Waymo’s newly released safety data—a level of transparency that Tesla has yet to match.

The exchange started when Google DeepMind Chief Scientist Jeff Dean pointed out the massive disparity in validated autonomous mileage between the two companies. Dean noted that Tesla doesn’t have “anywhere near the volume of rider-only autonomous miles that Waymo has,” citing Waymo’s fresh milestone of 100 million rider-only miles.

Musk, who has promised a fleet of “1 million robotaxis” by the end of 2020 (a deadline that passed five years ago), responded with his usual bravado:

“Waymo never really had a chance against Tesla. This will be obvious in hindsight.”

In fact, Tesla has zero Robotaxi miles with rider-only as its service still has in-car safety supervisors. Despite the safety drivers preventing an untold number of accidents, Tesla has a much higher accident rate with its supervised robotaxis than Waymo or average human drivers.

Even with this worrying situation, Musk said yesterday that Tesla plans to remove the safety drivers in the Austin Robotaxi within 3 weeks.

Musk’s comment is particularly ill-timed given the context. Waymo just released a massive tranche of safety data covering its operations across San Francisco, Phoenix, Los Angeles, and Austin.

The data show that Waymo’s Driver avoids crashes at a rate significantly better than human drivers, with a 91% reduction in serious injury-causing crashes compared to human benchmarks.

Meanwhile, Tesla has yet to deploy a single vehicle without supervision for a commercial ride or even share anywhere near the amount of data Waymo shares..

While Tesla regularly releases a “safety report”, it was widely criticized by safety experts for being an “apples-to-oranges” comparison. Tesla’s report relied on airbag deployments as a proxy for crashes and lacked the granular injury data that Waymo provided. Furthermore, Tesla’s data covers a system that is supervised by a human 100% of the time, making it impossible to isolate the safety performance of the software itself.

Tesla frames the data as proving “FSD is better than human drivers”, but in truth, if you take the data, it faces value; it only compares “FSD with human supervision to human drivers.”

Electrek’s Take

I find it increasingly difficult to reconcile Elon’s statements with reality. Waymo is currently operating fully driverless commercial services in multiple major cities. Tesla is still testing a Level 2 driver-assist system that requires constant human attention.

Apple and oranges.

We are looking at two companies. One has nearly 100 million miles of documented, driverless driving with specific, published safety data showing it is safer than humans. The other has zero driverless miles, vague safety reports that rely on proxies like airbag deployments, and a CEO who has been promising “next year” for a decade.

For Elon to look at Waymo, which is currently operating the exact service Tesla has been trying to build for years, and say they “never had a chance” is baffling.

To put it in terms that a racing enthusiast like Elon might understand: He thinks Tesla is leading the race because he can see Waymo in his rear-view mirror. What he doesn’t realize is that he isn’t ahead; he’s actually being lapped.

When a car is a full lap ahead of you, it appears behind you on the track. But that doesn’t mean you are winning.

I understand that he believes that Tesla’s cheaper system will enable it to scale faster once it solves unsupervised self-driving, but there’s simply no evidence of that.

If Tesla removes the safety drivers from its fleet in three weeks, as Musk claims, which is a big if, it will officially be about 5 years behind Waymo and will still need to prove safety without a supervisor and then scale.

FTC: We use income earning auto affiliate links. More.

I’ve ridden a lot of electric scooters over the years. Most blur together – two wheels, a deck, a motor, and a series of compromises. But every now and then, one stands out. And after a couple of weeks riding the Bo M2 electric scooter, I can confidently say: this one’s different.

The Bo M2 is not your average e-scooter. It’s a purpose-built, premium commuter with some seriously refined features – and a price tag to match. At $2,490, it’s firmly in high-end territory. But for riders who want a serious transportation tool, not a toy, there’s a lot to like here.

Bo M2 scooter review

To see what I mean, check out my ride review video below. Then keep reading for even more details on this innovative electric scooter!

What makes the Bo M2 stand out?

Let’s start with the construction. The M2 is built around a single-piece aluminum unibody frame, which the company calls the Monocurve chassis, and it’s beautiful. No welds, no hinges, no rattling folding mechanisms. Just one sweeping curve of aluminum that feels solid as a rock and helps explain the scooter’s clean, futuristic aesthetic.

This thing looks more like a design concept from a European mobility expo than something you’d expect to lock up outside a coffee shop. But it’s not just for looks (even if it does look beautiful). The rigid frame gives the whole scooter a planted, roadworthy feel. It doesn’t flex, wobble, or creak, even when you’re riding aggressively or hitting uneven pavement.

Even the most rigid of folding scooters will always have a bit of play in the folding area, but the Bo M2 just feels like a solid frame throughout – more like a motorcycle frame than a standing scooter frame.

And speaking of stability, let’s talk about the real magic trick here: the steering system.

The best handling I’ve ever felt on a scooter

The Bo M2 uses a proprietary feature the company calls Safesteer, which is essentially a built-in steering damper. Think of it as power steering for a scooter – but in reverse. Instead of making the steering looser or twitchier, it actually adds some light resistance and dampens those small, unwanted wobbles you often get when riding one-handed or over rough terrain. The result is that the bars don’t wiggle and they also naturally have a slight return pull towards the neutral position.

The effect is genuinely impressive. You can feel it from the first few feet of riding. At slow speeds, the front end feels calm and composed, not fidgety or loose. At high speeds, it tracks in a straight line with an almost eerie smoothness. I can even ride the scooter no-handed like a bicycle or motorcycle, though it just feels wrong to do so because I’ve spent my entire life knowing that you can’t ride a scooter no-handed… at least until now.

It’s one of those features you don’t realize you need until you experience it – and now I wish every scooter had it.

For newer riders or anyone who’s ever felt nervous about steering on a scooter, Safesteer is a game changer. And for experienced riders, it just makes the whole ride feel more premium.

Performance and range

The Bo M2 uses a 400W-rated motor with an actual peak output of 1,270W, and it delivers a top speed of 22 mph (35 km/h). That’s fast enough for most urban commuting in the bike lane and likely more than enough to keep pace with bike traffic.

It’s not going to pace a Class 3 e-bike in the US, but it’s still pretty fast for riding along on 10×2.5″ tires.

Acceleration is strong but not jerky, especially in Sport mode, which gives you full power. There’s also an Eco mode if you want to conserve battery or ride more gently. I mostly stuck with Sport mode, since it’s fun without feeling twitchy.

Range is rated at up to 26.2 miles (42 km), or one marathon, and while that’s best-case scenario, I could get over 20 miles (32 km) per charge riding at mixed speeds in the city. I’d call that sufficient for most daily commuters, and the 672 Wh battery charges in about 4.5 hours with the included fast charger.

Braking and control

Bo takes a slightly different approach to braking than most scooters. Up front, you get a sealed mechanical drum brake. Out back, there’s a regenerative electronic brakes with e-ABS that activates when you pull the left lever. The regenerative braking can pull as much as 1,000W of power, helping to (briefly) recharge the battery during each stop.

Braking is smooth and progressive, and the regen system is particularly satisfying. It slows the scooter down quickly and recaptures a bit of energy while doing it. Plus, there’s less maintenance to worry about with sealed drums and electronic brakes.

And of course, having the Safesteer system means you can brake hard without worrying about wobble or oversteer. Everything feels composed, like it was designed by automotive engineers… since it was.

Ride quality, comfort, and details

The ride comfort on the Bo M2 is among the best I’ve experienced on a scooter without full suspension. Part of that is due to the Airdeck system, which is a layer of EVA foam that adds vibration damping to the standing deck. Combined with the 10-inch tubeless pneumatic tires and ergonomic silicone grips, it smooths out a surprising amount of road chatter.

It’s not a plush, bouncy ride as you’d get with spring suspension, but it feels deliberate and connected to the road, like riding a high-quality urban bicycle. This will absolutely not make up for big pot holes, but it will feel better on normal rough roads then a typical rigid scooter. You’re giving up the advantages of long travel suspension for the benefit of rigidity, and the Airdeck system helps make swallowing that compromise a bit easier.

There are also a lot of thoughtful features that make the M2 feel like a real vehicle. The 800-lumen headlight is excellent, and the 270° daytime running light ring makes the scooter more visible from all angles. The rear light includes a brake alert, and everything is IP66-rated, so riding in the rain is no problem. Or at least it’s not a problem for the scooter. I’d still recommend you not ride in the rain unless you have to since its harder to be seen by cars and you do have to worry about loosing traction on slick surfaces like wet leaves, smooth pavement, etc.

The scooter comes with a MOUS Intralock phone mount (which I didn’t use because I’m married to the Peak Design phone lock system, but they do include an adapter if you want to stick it to the back of your own phone case). There’s also lockable anchor points for a U-lock and a built-in motor immobilizer that you can activate via the Bo smartphone app, giving you a bit more peace of mind in terms of theft prevention.

Is it worth the price?

At $2,490, the Bo M2 is definitely not cheap. You can get solid e-scooters for less than half that price. And so I will immediately tell you that this is not the scooter for everyone, or even most people. This is not a bang-for-your-buck scooter. This is something fancy for those who want to pay more for fancier features like steering dampers and a design that speaks to things no other scooter ever has.

This is a commuter-grade vehicle for someone who wants to ditch the car or bus and ride something premium, daily. And it genuinely delivers on that promise.

If you’re looking to spend less, Bo also offers the Bo M1, which shares much of the same design DNA but has lower power and a slightly reduced spec sheet. It starts at $1,990, saving around $500 compared to this higher spec version. But after riding the M2, I’d say the upgrade is worth it if you want the best experience.

And if you’re considering a Bo scooter at all, let’s just say that money probably isn’t your first concern. A scooter that was brought to you by former engineers at outfits like Jaguar and Land Rover was never going to be designed to compete on price, but rather on premium features and design.

Final thoughts

The Bo M2 is one of the most refined electric scooters I’ve ever tested. It’s beautifully built, thoughtfully engineered, and loaded with features that actually make a difference in day-to-day riding.

The steering damper alone puts it in a league of its own for ride stability, and the unibody aluminum frame gives it a level of build quality that most folding scooters can’t touch.

No, it’s not for everyone. If you just need a cheap ride for a few blocks, this is 100% overkill. But if you’re serious about getting something premium, you definitely want the standing ride of an e-scooter, and you want a daily commuter that feels more like a transportation appliance than a toy, the Bo M2 is worth every penny.

And with a scooter that rides this smoothly, you might actually look forward to your commute.

FTC: We use income earning auto affiliate links. More.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024