‘Misleading’ Shell adverts about low-carbon products banned

Three adverts for Shell that publicise its climate-friendly products have been banned for glossing over its “large scale” investments in oil and gas.

The Advertising Standards Authority (ASA) ruled the ads created the impression that a “significant proportion of Shell’s business” comprised “low carbon energy products”.

The company misleadingly “omitted” information that oil and gas made up the “vast majority” of its operations, the ASA said.

Shell said it strongly disagreed with the watchdog’s decision and claimed the finding could slow the UK’s move towards renewable energy.

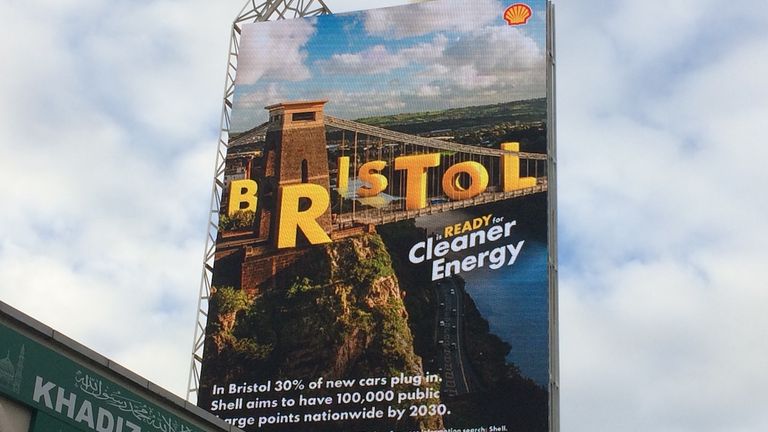

The three adverts in question showcased the renewable power that Shell provides and its clean energy services, including electric vehicle charging.

A TV ad from last June stated 1.4 million households in the UK used 100% renewable electricity from Shell. It also mentioned that the firm was working on a wind project that could power six million homes and aimed to fit 50,000 electric car chargers nationwide by 2025.

A video on Shell’s YouTube channel was captioned: “From electric vehicle charging to renewable electricity for your home, Shell is giving customers more low-carbon choices and helping drive the UK’s energy transition. The UK is ready for cleaner energy.”

Shell UK said it wanted the ads to raise consumer awareness about its range of energy products that were better for the environment than fossil fuels, and increase demand for them.

It cited research suggesting that 83% of consumers primarily associated the brand with the sale of petrol, arguing they would be “unlikely to assume that the ads’ content covered the full range of its business activities”.

One of the adverts banned by the ASA

A screenshot of one of the adverts banned by the ASA. Pic: Shell via ASA

In 2022, Shell spent 17% (£3.5bn) of its total capital expenditure (£20bn) on “low-carbon energy solutions”, which include renewable wind and solar power as well as things like electric vehicle charging, biofuels, carbon credits and hydrogen filling stations.

Why the ASA upheld the complaint

The ASA acknowledged that many people would associate Shell with petrol sales, as well as oil and gas production.

It said they would also be aware that many companies in carbon-intensive industries, including the oil and gas sector, aimed to dramatically reduce their emissions in response to the climate crisis.

Burning coal, oil and gas is the biggest driver of climate change, responsible for 75% of global greenhouse gas emissions.

The ASA said: “We understood that large-scale oil and gas investment and extraction comprised the vast majority of the company’s business model in 2022 and would continue to do so in the near future.

“We therefore considered that, because (the ads) gave the overall impression that a significant proportion of Shell’s business comprised lower-carbon energy products, further information about the proportion of Shell’s overall business model that comprised lower-carbon energy products was material information that should have been included.

“Because the ads did not include such information, we concluded that they omitted material information and were likely to mislead.”

It ruled that the ads must not appear again.

Read more:

Protesters try to storm stage at Shell AGM

Shell announces record annual profits

‘Climate criminals!’ – oil firm protest

A Shell spokesman said: “We strongly disagree with the ASA’s decision, which could slow the UK’s drive towards renewable energy.

“People are already well aware that Shell produces the oil and gas they depend on today. When customers fill up at our petrol stations across the UK, it’s under the instantly recognisable Shell logo.”

Shell claimed that many people do not know about its investment in more eco-friendly options, such as its vast public networks of EV charge-points.

It added: “No energy transition can be successful if people are not aware of the alternatives available to them. That is what our adverts set out to show, and that is why we’re concerned by this short-sighted decision.”

Veronica Wignall, from activist network Adfree Cities, which raised the complaint with the ASA, said: “Today’s official ban on Shell’s adverts marks the end of the line for fossil fuel greenwashing in the UK.

“The world’s biggest polluters will not be permitted to advertise that they are ‘green’ while they build new pipelines, refineries and rigs.”

Fossil fuel companies should be banned from advertising at all given their role in the climate crisis, she added.

Watch The Climate Show with Tom Heap on Saturday and Sunday at 3pm and 7.30pm on Sky News, on the Sky News website and app, and on YouTube and Twitter.

The show investigates how global warming is changing our landscape and highlights solutions to the crisis.

The UK has come a “step closer” to having direct, high-speed rail connections to Germany, the Department for Transport has said.

A partnership between international train operator Eurostar and German national rail company Deutsche Bahn (DB) has “set the foundation” for a fast rail connection between Britain and Europe’s largest economy, the businesses announced on Thursday.

It means the companies are exploring options to offer direct services between London and Cologne and Frankfurt.

Money blog: Major airport increasing drop-off charge

Such direct services would mean reaching Cologne in four hours, and Frankfurt in less than five from the capital city.

At present, rail passengers have to change trains in Brussels to reach those cities. It takes at least five-and-a-half hours to reach Frankfurt, and four-and-a-quarter hours to arrive in Cologne.

Cologne Central Station could soon be served by trains from the UK. Pic: AP

The proposed services would use existing lines and infrastructure. Passengers would board a double-decker Eurostar in London, and be spared a change of trains on the continent.

The ambition to create such links had already been announced, as had a plan to allow direct rail travel from London to Geneva, but the partnership between DB and Eurostar had not.

Will it definitely happen?

Details and technicalities are yet to be worked out, with the German train company highlighting that any services are contingent upon “the necessary technical, operational, and legal prerequisites being met”.

“Implementation by individual railway companies is considered extremely difficult,” DB said.

“Joint partnerships are therefore crucial.”

What about Berlin?

Nothing was announced for a direct service to Berlin on Thursday, despite Transport Secretary Heidi Alexander singling out the benefits and prospect of journeys from London to the German capital in July.

“The Brandenburg Gate, the Berlin Wall and Checkpoint Charlie – in just a matter of years, rail passengers in the UK could be able to visit these iconic sights direct from the comfort of a train, thanks to a direct connection linking London and Berlin,” she said at the time.

A high-speed Eurostar train heading towards France. File pic: PA

Shorter journeys, like those to Frankfurt and Cologne, are seen as more commercially viable than the current 10-hour train journey time to Berlin.

Market studies conducted by Eurostar found travellers are comfortable with international rail journeys of up to six hours.

“Our research indicates that many would choose rail over air for trips within this timeframe,” Eurostar told Sky News. “This, combined with strong business and leisure demand on this route, is why we have prioritised London to Frankfurt.”

Read more from Sky News:

Petrofac administrators eye North Sea sale by Christmas

Submarine hunting pact signed by UK amid Russian threat

The Department for Transport said the focus on the two German cities was a commercial decision by Eurostar and DB, and the UK-Germany rail taskforce, established over the summer, could pave the way for further route announcements.

The energy regulator has confirmed plans for a massive upgrade to the UK’s energy grids, adding £108 to customer bills by 2031.

Ofgem said on Thursday that the £28bn investment over the next five years would bolster resilience in the transition to a renewable energy future and that much of the bill would be offset by increased efficiency.

It pointed to estimated savings for households of around £80 because of the planned investment in gas and power infrastructure, leaving a net additional contribution of £28.

Money latest: Is property still a good investment?

Ofgem said the £28bn sum formed part of an estimated £90bn to be invested in the energy networks by 2031, with “adaptive” funding arrangements helping to shield customers from volatility in the market.

Most of the funding announced on Thursday will go towards maintaining gas networks, which will remain a key source of energy as green power capacity is built up further.

“Investing now to maintain world-class resilience and expand grid capacity is the most cost-effective way to harness clean power, support economic growth and protect the country from gas price shocks like the one seen in 2022”, Ofgem said.

What’s driving energy prices higher?

Then, Russia’s invasion of Ukraine and Europe’s refusal to buy Russian gas in response, meant that energy bills hit unprecedented levels and gave birth to the wider cost-of-living crisis as higher energy costs were passed on across the economy.

Read more: Paying up front for energy future should lead to tangible savings

Ofgem made its announcement as costs of government energy policy and other upgrades make the biggest upwards contributions to household bills. However, the budget moved to take away some costs from April next year.

Ofgem boss Jonathan Brearley said: “The funding announced today will keep Britain’s energy network among the safest, most secure and resilient in the world. The investment will support the transition to new forms of energy and support new industrial customers to help drive economic growth and insulate us from volatile gas prices.

“But this is not investment at any price. Every pound must deliver value for consumers. Ofgem will hold network companies accountable for delivering on time and on budget, and we make no apologies for the efficiency challenge we’re setting as the industry scales up investment.

“We’ve built strong consumer protections into these contracts, meaning funds will only be released when needed and clawed back if not used. Households and businesses must get value for money, and we will ensure they do.”

‘It’s either keep warm or eat’

A Department for Energy Security and Net Zero spokesperson said: “This government is taking action to bring down energy bills for families, with the budget taking an average £150 of costs off bills in April, and expanding our £150 Warm Home Discount to over six million families.

“Upgrading our gas and electricity networks after years of underinvestment is essential to keep the lights on and ensure energy security for our country. Without these plans, which were first set out under the previous government, costs would spiral and our security would be compromised.

“The only way to bring down bills for good and get off the fossil fuel rollercoaster is with this government’s mission to deliver clean homegrown that we control.”

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024