Eurozone officially entered recession after Eurostat revises figures

The 20 countries using the euro were officially in recession over the winter, latest statistics show.

Revised data from the European statistics office, Eurostat, showed the eurozone economy contracted 0.1% in the first three months of this year and the final three months of 2022.

The group of countries therefore met the definition of a technical recession: two-quarters of negative economic growth.

Not since the COVID pandemic has there been a six-month period where the economy shrank.

Previous estimates from Eurostat had shown a stagnant economy but these have since been revised downwards. The European Central Bank (ECB) was expecting no growth but did not forecast contraction.

Today’s figures also show Ireland and Greece had winter recessions. Ireland had the worst gross domestic product (GDP) contraction – the economy is reported to have shrunk 4.6% from January to March.

GDP measures the sum total of everything produced in the economy.

At the same time Ireland has a record budget surplus of billions of euro – mostly derived from tax from a handful of multinationals – casting doubt over the figures.

Germany was declared as being in recession earlier this month and no growth has been recorded in Lithuania since 2021.

Whether the countries and the eurozone are still in recession is not known as second-quarter figures for 2023 have yet to be published.

Read more business

First-time crypto investors to be offered ‘cooling-off’ period under new rules

WhatsApp adding Twitter-like ability to follow with new ‘channels’ feature

The 20 countries all struggled with high energy costs, particularly over winter, as they attempted to reduce reliance on Russian oil and gas, following the invasion of Ukraine.

Prices reached new highs as the West scrambled to find alternative sources of gas, which most European countries depend on to produce electricity and heat homes.

Those high energy costs filtered into food production, pushing up the cost of household food bills.

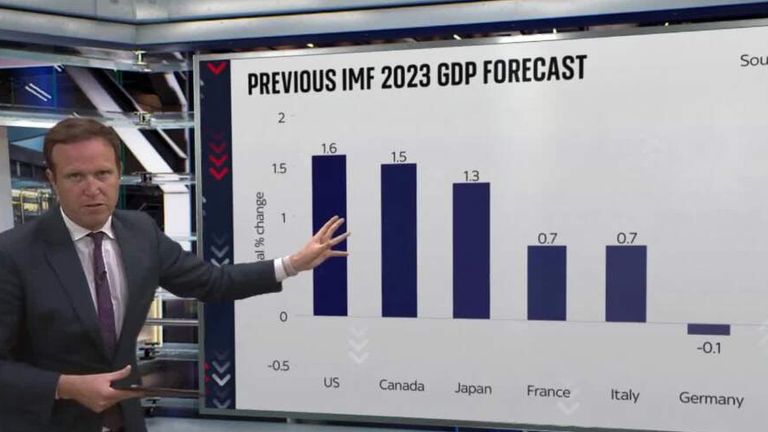

Economics and data editor Ed Conway explains the IMF’s latest projections.

The UK economy has also shrunk, according to latest official figures. Despite slight growth in the first three months of the year there was a 0.3% contraction in March.

Growth of 0.1% was recorded by the Office of National Statistics (ONS) in the three months of the year, the lowest amount possible to still be classed as growth as IT and construction sector activity offset the impact of strikes.

Thousands of job cuts at the NHS will go ahead after the £1bn needed to fund the redundancies was approved by the Treasury.

The government had already announced its intention to slash the headcount across both NHS England and the Department of Health by around 18,000 administrative staff and managers, including on local health boards.

The move is designed to remove “unnecessary bureaucracy” and raise £1bn a year by the end of the parliament to improve services for patients by freeing up more cash for operations.

NHS England, the Department of Health and Social Care, and the Treasury had been in talks over how to pay for the £1bn one-off bill for redundancies.

It is understood the Treasury has not granted additional funding for the departures over and above the NHS’s current cash settlement, but the NHS will be permitted to overspend its budget this year to pay for redundancies, recouping the costs further down the line.

‘Every penny will be spent wisely’

Chancellor Rachel Reeves is set to make further announcements regarding the health service in the budget on 26 November.

And addressing the NHS providers’ annual conference in Manchester today, Mr Streeting is expected to say the government will be “protecting investment in the NHS”.

He will add: “I want to reassure taxpayers that every penny they are being asked to pay will be spent wisely.

“Our investment to offer more services at evenings and weekends, arm staff with modern technology, and improving staff retention is working.

“At the same time, cuts to wasteful spending on things like recruitment agencies saw productivity grow by 2.4% in the most recent figures – we are getting better bang for our buck.”

Health Secretary Wes Streeting during a visit to the NHS National Operations Centre in London earlier this year. Pic: PA

Mr Streeting’s speech is due to be given just hours after he became entrenched in rumours of a possible coup attempt against Sir Keir Starmer, whose poll ratings have plummeted ahead of what’s set to be a tough budget.

Mr Streeting’s spokesperson was forced to deny he was doing anything other than concentrating on the health service.

Read more from Sky News:

Russian troops in Mad Max-style video

Shamima Begum ‘should be repatriated’

He is also expected on Wednesday to give NHS leaders the go-ahead for a 50% cut to headcounts in Integrated Care Boards, which plan health services for specific regions.

They have been tasked with transforming the NHS into a neighbourhood health service – as set down in the government’s long-term plans for the NHS.

Those include abolishing NHS England, which will be brought back into the health department within two years.

Watch Wes Streeting on Mornings With Ridge And Frost from 7am on Sky News.

The UK’s jobless rate has risen to a level not seen since late 2020, according to official figures released ahead of the budget.

The Office for National Statistics (ONS) reported a figure of 5% covering the three months to September – up from 4.8% reported last month. It was a larger leap than economists had predicted, and the ONS said that men were worst affected by the shift.

It leaves the jobless rate at its highest level since December 2020-February 2021.

It had stood at 4.1% when Labour took office last year.

Money latest: How private pensions are treated in divorce

There was no better news for Chancellor Rachel Reeves in wider, experimental, HMRC data released by the ONS, which showed a 32,000 decline in payrolled employment during October.

That suggested a pause to a more recent trend of declines slowing since sharp falls first witnessed in the spring of this year.

It was April when measures introduced in Ms Reeves’s first budget came into effect, with hikes in minimum pay and employer national insurance contributions hammering employment and investment sentiment in the private sector.

It also coincided with peak US trade war uncertainty as Donald Trump ramped up his tariffs.

Where Reeves stands on tax rises

ONS director of economic statistics Liz McKeown said of the data: “Taken together these figures point to a weakening labour market.

“The number of people on payroll is falling, with revised tax data now showing falls in most of the last 12 months.

“Meanwhile the unemployment rate is up in the latest quarter to a post pandemic high. The number of job vacancies, however, remains broadly unchanged.

“Wage growth in the private sector slowed further, but we continue to see stronger public sector pay growth, reflecting some pay rises being awarded earlier than they were last year.”

In good news, the overall slowing in the pace of wage growth and weakening jobs market should help bolster the case for an interest rate cut by the Bank of England next month, assuming inflationary pressures continue to ease after last week’s rate hold.

The ONS figures were released as the clock ticks down to the chancellor’s second budget due on 26 November.

The state of UK economy ahead of budget

Ms Reeves used an event in Downing Street last week to prepare the ground for a painful series of measures that are expected to be only partly offset by some announcements to keep Labour MPs onside, as she stares down a black hole in the public finances believed to be in the region of £30bn.

She has signalled a break from Labour’s manifesto tax pledge not to raise income tax, national insurance or VAT, on the grounds that the world has changed since that promise was made.

The chancellor’s gripes include Brexit and the effects of the US trade war.

Nevertheless, a spending priority would appear to be the lifting of the two-child benefit cap. That would take an estimated 350,000 children out of poverty, according to the Child Poverty Action Group.

Liberal Democrat Treasury spokesperson, Daisy Cooper, said of the employment data: “Surely the writing is on the wall now for the chancellor’s jobs tax.

“Everyone except Rachel Reeves seems to have woken up to the fact that forcing small businesses to pay more in tax for giving people jobs would damage job opportunities. Now the proof is staring her in the face.

“The government must reverse their damaging national insurance hike at the budget, and commit to saving the small businesses who employ millions in Britain and are at risk of collapse, if they’re to have any hope of reversing today’s concerning trend.”

The Conservatives accused Ms Reeves of presiding over a “high-tax, anti-business” agenda.

Secretary of State for Work and Pensions, Pat McFadden, said: “Over 329,000 more people have moved into work this year already, but today’s figures are exactly why we’re stepping up our plan to Get Britain Working.

“We’ve introduced the most ambitious employment reforms in a generation to modernise jobcentres, expand youth hubs and tackle ill-health through stronger partnerships with employers.

“And this week we’re going further by launching an independent investigation that will bolster our drive to ensure all young people are earning or learning.

“We’re backing businesses to grow and create jobs by cutting red tape, signing trade deals and securing hundreds of billions in investment, which helped make the UK the fastest growing economy in the G7 in the first half of this year.”

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024