Here’s what’s hot — and what’s not — in fintech right now

Fintech executives descend on Amsterdam for the annual Money2020 conference.

MacKenzie Sigalos

AMSTERDAM, Netherlands — At last year’s Money 20/20 — Europe’s marquee event for the financial technology industry — investors and industry insiders were abuzz with talk about embedded finance, open banking, and banking-as-a-service.

As nebulous as these terms may be, they reflected a very real push from tech startups, including the biggest names in the business such as Stripe and Starling Bank, to allow businesses of all stripes to develop their own financial services, or integrate other firms’ products into their platforms.

This year, with fintechs and their mainly venture capital and private-equity backers reeling from a dire slump in technology valuations and softer consumer spending, the narrative around what’s “hot” in fintech hasn’t changed an awful lot.

Investors still love companies offering services to enterprises rather than consumers. In some cases, they’ve been willing to write checks for firms at valuations unchanged from their last funding round. But there are a few key differences — not least the thing of curiosity that is generative artificial intelligence.

So what’s hot in fintech right now? And what’s not? CNBC spoke to some of the top industry insiders at Money 20/20 in Amsterdam. Here’s what they had to say.

What’s hot?

Looking around Money 20/20 this week, it was easy to see a clear trend going on. Business-facing or business-to-business companies like Airwallex, Payoneer, and ClearBank, dominated the show floor, while consumer apps such as Revolut, Starling, and N26 were nowhere to be found.

“I think many fintechs have pivoted to enterprise sales having found consumer hard to make sufficient unit economics — plus it’s pretty expensive to get a stand and attend M2020 so you need to be selling to other attendees to justify the outlay,” Richard Davies, CEO of U.K. startup lender Allica Bank, told CNBC.

“B2B is definitely in good shape — both SME and enterprise SaaS [software-as-a-service] — providing you can demonstrate your products and services, have proven customer demand, and good unit economics. Embedded finance certainly is part of this and has a long way to run as it is in its infancy in most cases,” Davies said.

B2B fintechs are startups that develop digital financial products tailored to businesses. SaaS is software that tech firms sell to their customers as a subscription. Embedded finance refers to the idea of third-party financial services like bank accounts, brokerage accounts and insurance policies being integrated into other businesses’ platforms.

Niklas Guske, who runs operations at Taktile — a fintech start-up focused on streamlining underwriting decisions for enterprise clients — describes the sector as being in the middle of a renaissance for B2B payments and financing.

“There is a huge opportunity to take lessons from B2C fintechs to uplevel the B2B user experience and deliver far better solutions for customers,” said Guske. “This is particularly true in SME finance, which is traditionally underserved because it has historically been difficult to accurately assess the performance of younger or smaller companies.”

One area fintech companies are getting excited by is an improvement to online checkout tools. Payments technology company Stripe, for instance, says a newer version of its checkout surfaces has helped customers increase revenue by 10.5%.

“That is kind of incredible,” David Singleton, chief technology officer of Stripe, told CNBC. “There are not a lot of things you can do in a business that increase your revenue by 10%.”

Meanwhile, companies tightening their belts at the event is also a theme.

One employee of a major firm that usually attends the event said they have cut down on the number of people they have sent to Money 20/20 and have not even bought a stand. The employee was not authorized to speak to the media.

Indeed, as companies look to scale as they cut back on spending, many say a key priority is adequately managing risk.

“When funds were readily available, many fintechs could subsidize poor risk assessments with investor money,” Guske said of the sector, adding that in today’s climate, fintechs are only profitable if they can identify and secure the right customers.

“This is another moment where the proliferation of new data sources and the adoption of sophisticated risk modeling enables fintechs to better target their ideal customers better than ever before,” said Guske, who raised more than $24 million from the likes of Y Combinator and Tiger Global.

Generative AI

The main area that drew the most hype from Money 20/20 attendees, however, was artificial intelligence.

That’s as ChatGPT, the popular generative AI software from OpenAI which produces human-like responses to user queries, dazzled fintech and banking leaders looking to understand its potential.

In a closed-door session on the application of fintech in AI Wednesday, one startup boss pitched how they’re using the technology to be more creative in communications with their customers by incorporating memes into the chat function and allowing its chatbot, Cleo, to “roast” users about poor spending decisions.

Callan Carvey, global head of operations at Cleo, said the firm’s AI connects to a customer’s bank account to get a better understanding of their financial behavior.

“It powers our transaction understanding and that deeply personalized financial advice,” Carvey said during her talk. “It also allows us to leverage AI and have predictive measures to help you avoid future financial mistakes,” such as avoiding punchy bank fees you could otherwise avoid.

Teo Blidarus, CEO and co-founder of financial infrastructure firm FintechOS, said generative AI has been a boon to platforms like his, where companies can build their own financial services with little technical experience.

“AI, and particularly generative AI, it’s a big enabler for fintech enablement infrastructure, because if you’re looking at what are the barriers that low code, no code on one side and generative AI on the other are trying to solve if the complexity of the overall infrastructure,” he told CNBC.

“A job that typically would take around one or two weeks can now be completed in 30 minutes, right. Granted, you still need to polish it a little bit, but fundamentally I think it allows you know to spend your time on more productive stuff — creative stuff, rather than integration work.”

As businesses hyper-focus on how they can do more with less, both tech-forward and traditional businesses say they have been turning to revenue and finance automation products that handle back-office operations to try to optimize efficiency.

Indeed, Taktile’s Guske notes that the current demand to continue scaling rapidly while simultaneously reducing costs has driven many fintechs to reduce operational expenses and improve efficiency through an increase in automation and reducing manual processes, especially in onboarding and underwriting.

“I see the biggest, actual application of generative AI in using it to create signals out of raw transaction or accounting data,” said Guske.

What’s not?

One thing’s for sure: consumer-oriented services aren’t the ones getting the love from investors.

This year has seen major digital banking groups and payment groups suffer steep drops in their valuations as shareholders reevaluated their business models in the face of climbing inflation and higher interest rates.

Revolut, the British foreign exchange services giant, had its valuation cut by shareholder Schroders Capital by 46%, implying a $15 billion markdown in its valuation from $33 billion, according to a filing. Atom Bank, a U.K. challenger bank, had its valuation marked down 31% by Schroders.

It comes as investment into European tech startups is on track to fall another 39% this year, from $83 billion in 2022 to $51 billion in 2023, according to venture capital firm Atomico.

“No one comes to these events to open like a new bank account, right?” Hiroki Takeuchi, CEO of GoCardless, told CNBC. “So if I’m Revolut, or something like that, then I’m much more focused on how I get my customers and how I make them happy. How do I get more of them? How do I grow them?”

“I don’t think Money 20/20 really helps with that. So that doesn’t surprise me that there’s more of a shift towards B2B stuff,” said Takeuchi.

Layoffs have also been a massive source of pain for the industry, with Zepz, the U.K. money transfer firm, cutting 26% of its workforce last month.

Even once richly valued business-focused fintechs have suffered, with Stripe announcing a $6.5 billion fundraise at a $50 billion valuation — a 50% discount to its last round — and Checkout.com experiencing a 15% drop in its internal valuation to $9 billion, according to startup news site Sifted.

Fintechs cooling on crypto

It comes after a turbulent year for the crypto industry which has seen failed projects and companies go bankrupt — likely a big part of why few crypto firms made an appearance in Amsterdam this year.

During the height of the most recent bull run, digital asset companies and know-your-customer providers dominated a lot of the Money 20/20 expo hall, but conference organizers tell CNBC that just 6% of revenue came from companies with a crypto affiliation.

Plunging liquidity in the crypto market, paired with a regulatory crackdown in the U.S. on firms and banks doing business with the crypto sector, have altered the value proposition for investing in digital asset integrations. Several fintech executives CNBC interviewed spoke of how they’re not interested in launching products tailored to crypto as the demand from their customers isn’t there.

Airwallex, a cross-border payments start-up, partners with banks and is regulated in various countries. Jack Zhang, the CEO of Airwallex, said the company will not be introducing support for cryptocurrencies in the near future, especially with the regulatory uncertainty.

“It’s very important for us to maintain the high standard of compliance and regulation … it is a real challenge right now to deal with crypto, especially with these global banks,” Zhang told CNBC in an interview on Tuesday.

Prajit Nanu, CEO of Nium, a fintech company that has a product that allows financial institutions to support cryptocurrencies, said interest in that service has “fallen off.”

“Banks who we power today have become very skeptical about crypto … as we see the overall ecosystem going through this … difficult time … we are looking at it much more carefully than what we would have looked at last year,” Nanu told CNBC in an interview Tuesday.

Blockchain is also no longer the buzzword it once was in fintech.

A few years ago, the trendy thing to talk about was blockchain technology. Big banks used to say that they weren’t keen on the cryptocurrency bitcoin but instead were optimistic about the underlying tech known as blockchain.

Banks praised the way the ledger technology could improve efficiency. But blockchain has barely been mentioned at Money 20/20.

One exception was JPMorgan, which is continuing to develop blockchain applications with its Onyx arm. Onyx uses the technology to create new products, platforms and marketplaces — including the bank’s JPM Coin, which it uses to transfer funds between some of its institutional clients.

However, Basak Toprak, executive director of EMEA and head of coin systems at JPMorgan, gave attendees a reality check about how limited practical use of the technology is in banking at the moment.

“I think we’ve seen a lot of POCs, proof of concepts, which are great at doing what it says on the tin, proving the concept. But I think, what we need to do is make sure we create commercially viable products for solving specific problems, sustain customer confidence, solving issues, and then launching a product or a way of doing things that is commercially viable, and working with the regulators.”

“Sometimes I think the role of the regulators is also quite important for industry as well.”

The Datadog stand is being displayed on day one of the AWS Summit Seoul 2024 at the COEX Convention and Exhibition Center in Seoul, South Korea, on May 16, 2024.

Chris Jung | Nurphoto | Getty Images

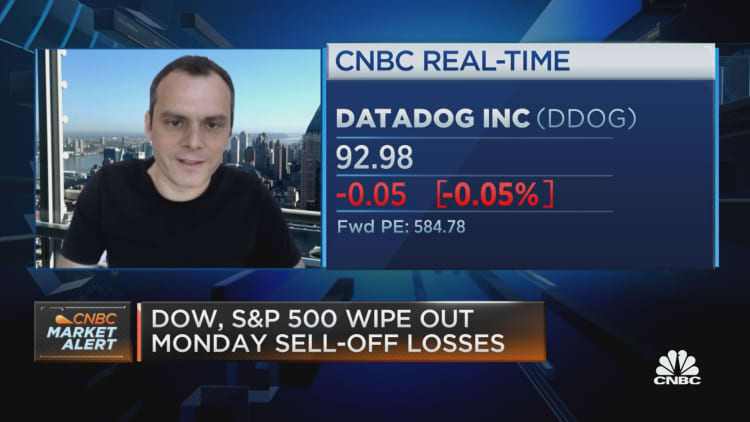

Datadog shares were up 10% in extended trading on Wednesday after S&P Global said the monitoring software provider will replace Juniper Networks in the S&P 500 U.S. stock index.

S&P Global is making the change effective before the beginning of trading on July 9, according to a statement.

Computer server maker Hewlett Packard Enterprise, also a constituent of the index, said earlier on Wednesday that it had completed its acquisition of Juniper, which makes data center networking hardware. HPE disclosed in a filing that it paid $13.4 billion to Juniper shareholders.

Over the weekend, the two companies reached a settlement with the U.S. Justice Department, which had sued in opposition to the deal. As part of the settlement, HPE agreed to divest its global Instant On campus and branch business.

While tech already makes up an outsized portion of the S&P 500, the index has has been continuously lifting its exposure as the industry expands into more areas of society.

DoorDash was the latest tech company to join during the last rebalancing in March. Cloud software vendor Workday was added in December, and that was preceded earlier in 2024 with the additions of Palantir, Dell, CrowdStrike, GoDaddy and Super Micro Computer.

Stocks often rally when they’re added to a major index, as fund managers need to rebalance their portfolios to reflect the changes.

New York-based Datadog went public in 2019. The company generated $24.6 million in net income on $761.6 million in revenue in the first quarter of 2025, according to a statement. Competitors include Cisco, which bought Splunk last year, as well as Elastic and cloud infrastructure providers such as Amazon and Microsoft.

Datadog has underperformed the broader tech sector so far this year. The stock was down 5.5% as of Wednesday’s close, while the Nasdaq was up 5.6%. Still, with a market cap of $46.6 billion, Datadog’s valuation is significantly higher than the median for that index.

— CNBC’s Ari Levy contributed to this report.

CNBC: Datadog CEO Olivier Pomel on the cloud computing outlook

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike