‘Risky’ for government to intervene as mortgage costs surge, ex-Bank of England deputy warns

It would be “risky” for the government to protect mortgage holders against rising interest rates, according to a former Bank of England deputy governor.

Speaking to Sophy Ridge on Sky News, Sir Charlie Bean said trying to help those paying off home loans could force the bank to raise the base rate even further.

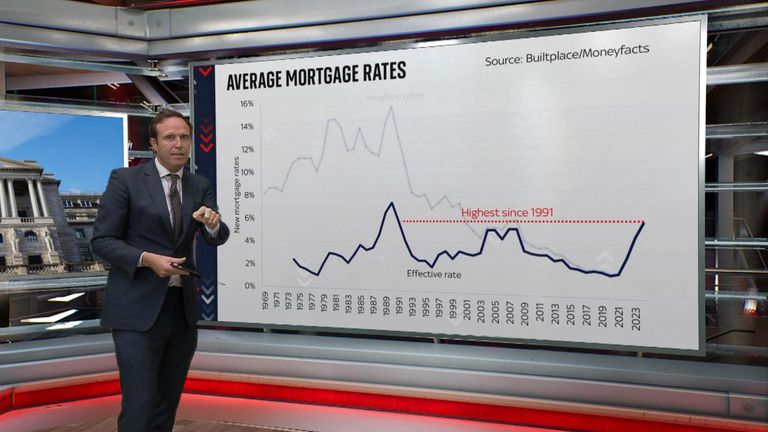

His warning follows a report from the Resolution Foundation think tank that says average annual mortgage repayments are set to rise by £2,900 for those renewing next year.

Total annual mortgage repayments could rise by £15.8bn by 2026, the report added.

Politics live: Cabinet minister reacts to ‘indefensible’ lockdown party video

Sir Charlie said: “There’s not a lot [government] can do to influence the overall macro environment in a favourable way.

“There may be things it wants to do to alleviate pain on particular parts of the population, poor households or whatever.

“There obviously have been some calls for protecting those with mortgages.

“I think that’s risky territory to get into because of course, if you do that and reduce the pressures on those with mortgages, that reduces the extent to which the economy slows and just means the bank has to raise interest rates even more.”

An extended period of inflation led the Bank of England to raise interest rates, pushing up the cost of borrowing.

These increases are now expected to continue until the middle of next year, with the base rate forecast to peak at nearly 6%.

Read more:

Explained: What is causing the mortgage crunch

Ed Conway: Mortgage payers face largest home loan squeeze since early 90s

Sunak insists he won’t pass the buck if he misses key inflation pledge

Homeowners warned of mortgage pain

With an election expected in 2024, interest rates continuing to rise ahead of the vote would cause headaches for Rishi Sunak and campaigners for the Conservative Party.

The uncertainty has led to TSB pulling all its 10-year fixed-rate deals from the market – and Santander withdrew its offers for new borrowers this week.

Michael Gove, the housing secretary, was asked by Sophy Ridge whether he was “frightened” by the situation.

He said he was “concerned of course”, saying the government’s target of getting inflation down would allow the bank to reduce interest rates.

The cabinet minister revealed he does not have a mortgage, but acknowledged the situation is “very difficult for hundreds of thousands of people”.

He added: “As a minister who is responsible for housing, I do take a close interest in what’s happening in the mortgage market.

“It only reinforces the importance of doing everything else that we can to support homeowners and indeed, specifically, to help those in the rental sector as well who have faced the prospect of increasing rents and that’s why we are bringing forward legislation, the Private Rented Sector Reform Bill, in order to help them.”

The bill is aimed at removing no-fault evictions and holding landlords to higher standards, while also allowing homeowners to have an easier time recovering properties from disruptive tenants.

‘No alternative’ to interest rate rise

Criticisms have been made of the Bank of England for not raising interest rates fast enough, allowing inflation to rise.

Sir Charlie admitted that his old employer was “a little behind the curve” in its actions – but added most of the inflationary pressure was coming from external factors like “the war in Ukraine, rising gas prices, global food prices, also supply chain pressures as economies reopened after the pandemic”.

In the upstairs bar of a slick new brewery, the cheese-lovers of Halifax are paying “homage to fromage”.

It is one of the first events in the historic West Yorkshire town’s further monthly cheese club and there is a decent turn-out.

Sky News visited Halifax’s clubs, bars and restaurants to get an insight into people’s priorities

The night-time economy in Halifax is a useful measure of how the landscapes of our town and cities have changed

Discussion of Wednesday’s budget is not as popular as an accompaniment to the cheese as the selection of wines. But no one holds back on what is required of the chancellor.

Natalie Rogers, who runs her own small business with her partner, said there needs to be focus.

Small business owner Natalie Rogers wants to see more investment in local industries

“I think investing in small businesses, investing in these northern towns, where at one time we were making all the money for the country, can we not get back to that? We’re not investing in local industries.”

At the next table, with a group of friends, Ali Fletcher said there needs to be bigger targets.

“I think wealth inequality is a major problem. The divide is getting wider. For me, a wealth tax is absolutely critical. We need to address this question of ‘Is there any money left?’. There’s plenty of money, it’s all about choices that government make.”

At this monthly cheese club, people told us about their priorities ahead of the budget

The evening’s cheese tasting was being marshalled by Lisa Kempster. “The impression I get from talking to people is there’s a lot of uncertainty, but when you ask them what they’re uncertain about, they’re not really sure, there’s just a general feeling of uncertainty and being cautious.”

Ali Fletcher reckons wealth inequality is a major problem

Read more:

Budget will be big – and Starmer has some serious convincing to do

Reeves vows to ‘grip the cost of living’

What tax rises could chancellor announce?

This corner of Halifax, close to the town’s historic Piece Hall, is buzzing with clubs, bars and restaurants, trying hard to defy the crunch in the night-time economy. It is a useful measure of how the landscapes of our town and cities has changed.

“Whenever there’s a budget, for a few days afterwards, there’s a drop off in trade,” said Michael Ainsworth, owner of the Graystone Unity, a bar and music venue in the town.

“I accept the government needs to raise money but, in this day and age, there’s better ways to go about doing that, like closing tax loopholes for the huge businesses to operate up with banking arrangements outside the UK.”

Michael Ainsworth owns a bar and music venue and thinks the chancellor needs to close tax loopholes

In the bar, a folk singer is going through a quirky and caustic set. In the basement, a punk band called Edward Molby is considerably louder.

On a sofa in the main bar, recent graduates Josh Kinsella and Ruby Firth, newly arrived in Halifax because of its more affordable housing, pinpoint what they want on Wednesday.

“Can we stop triple-locking the pensions, please? Stop giving pensioners everything. For God’s sake, I know they have hard times in the 70s and the 80s, but it just feels like we’re now paying for everyone else.”

Josh Kinsella and Ruby Firth feel there’s too much focus on pensioners

Ben Randm is a familiar face at the bar and well known on the music scene with his band, Silver Tongued Rascals.

“Everyday people are seen as statistics, we’re always the afterthought. When the cuts are done, we’re always impeded and the ramifications that has for people’s livelihoods, for people’s mental health, for people’s passion and drive… it’s such a struggle.”

He, like many in the night-time economy sector, wants extra help for hospitality and venues that, he says, provide a vital community link.

Ben Randm who has his own band reckons everyday people are ‘always the afterthought’

David Van Gestel chose Halifax to open the third branch of MAMIL, a bar in jokey honour of those cycling “middle-aged men in Lycra”. On a busy quiz night, he said venues had to provide something different to get people out of their homes.

“I think the government needs to start putting some initiatives in place. They talk about growth but the reality is that the only thing we’re seeing grow is our costs.”

Rachel Reeves is expected to announce a higher-than-inflation rise for 13 million pensioners in her upcoming budget.

People on the full rate of the new state pension will benefit with more than £550 a year more.

“Whether it’s our commitment to the triple lock or to rebuilding our NHS to cut waiting lists, we’re supporting pensioners to give them the security in retirement they deserve,” the chancellor said.

Wednesday’s long-trailed budget is expected to be big and speculation has persisted on whether it will include tax rises – and who those rises will affect.

And while she is expected to reaffirm the government’s commitment to the triple lock, she is believed to be considering limiting how much workers can put in their pension pots under sacrifice schemes before paying national insurance.

Sky News goes inside the room where the budget happens

Read more:

Starmer refuses to rule out manifesto-breaking tax rises

Reeves hints at more welfare cuts after previous rebellion

Craig Beaumont, external affairs director at the Federation of Small Business, said in comments reported by the Financial Times: “The chancellor promised not to come back for more but attacking salary sacrifice, which has been in place for 40 years to help employers help their staff, will impact business and their staff.”

In another move, the chancellor is expected to extend a crackdown on benefit fraud in an effort to raise £1.2bn.

This would include extending targeted case reviews, which root out inaccuracies in universal credit claims.

Budget: Own-goal or winner?

Ms Reeves is also thought to be considering bringing in a pay-per-mile tax for electric vehicle drivers.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024