Fresh pain for borrowers as Bank of England set to increase interest rate for the 13th time in a row

An interest rate rise by the Bank of England at midday is a nailed-on certainty – though opinions are split on the level of additional pain that could be imposed as efforts to curb the country’s inflation problem stumble.

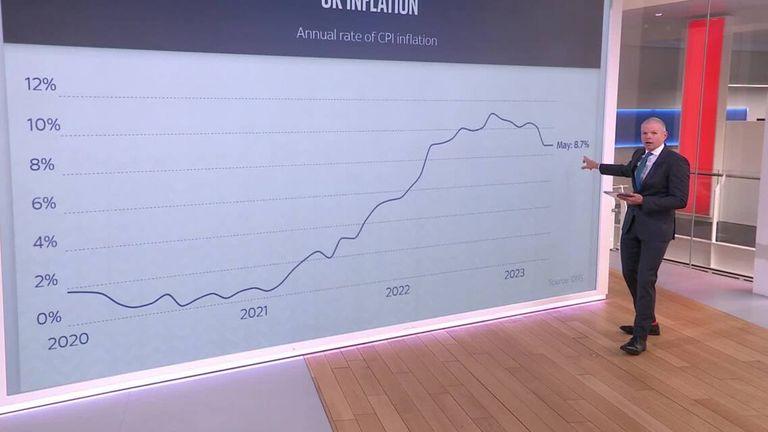

At the start of this week, policymakers were widely tipped to raise the base rate by a quarter of a percentage point to 4.75% – a record 13th consecutive increase – maintaining a slower path for hikes since March.

But the latest inflation figures, published yesterday, prompted financial market participants to anticipate a greater, almost even, chance of a half percentage point hike to 5%.

While there were already concerns about the stubborn pace of price rises, the inflation data came as a shock.

It showed price growth was becoming more engrained in the economy while the main consumer prices index (CPI) also failed to budge lower as most experts had predicted.

The Bank had also previously expressed concerns about the pace of wage rises which, it argues, contributes to demand and further inflation ahead.

Inflation is proving more difficult to cool than had been anticipated, and Chancellor Jeremy Hunt told Sky News last month he would even be comfortable with a recession if it brought inflation to heel.

The only tool the Bank has to do that, rate rises, will mean more pain for borrowers whatever today’s rate decision brings.

Read more: PM and chancellor face conundrum as mortgages rise – and there’s no silver bullet to end the crisis

Growing interest rate expectations over recent weeks have forced up funding costs for lenders, with data from Moneyfacts this week showing average rates for two-year fixed mortgage deals rising above 6%.

They have continued to rise each day this week having stood just above 2.5% in March last year.

With the financial markets now seeing the Bank rate potentially rising to 6% by early next year, such a level, if realised, would mean mortgage rates have far further to rise.

Read more:

The solution to bringing down inflation is a political nightmare for the Tories

Mortgage misery: What is causing the crunch, will it get worse and what can you do if you are struggling?

‘Eyewatering’ hit to 1.4 million, mainly young, mortgage customers ahead, IFS warns

In making its rate decision today, the Monetary Policy Committee could face a big split in voting – though the majority of opinion among commentators is that a quarter-point rise will be the result.

After all, the Bank has consistently steered markets away from their peak rate scenarios this year and even signalled that a pause in the rate cycle was close.

But the core function of the MPC is to keep inflation around a target rate of 2% – and there are signs of frustration in Whitehall that the independent Bank of England is lagging behind the curve.

So at a sticky 8.7% – and with wage growth and so-called core inflation (which strips out volatile elements such as energy and food) ticking up last month – some might be forgiven for thinking there was every justification for a 0.5 percentage point rate hike.

‘Sticky’ inflation explained

The other side of the argument suggests a smaller rise would be sufficient as there is evidence that the 12 rate hikes to date, along with a natural easing in many costs, were starting to have an effect.

Samuel Tombs, chief UK economist at Pantheon Macroeconomics, said wider data suggested wage growth pressures would start to reduce and that energy-linked inflation would fall sharply, allowing an easing of price growth more widely.

He said of the MPC’s dilemma: “The headline rate of CPI inflation still looks set to fall sharply over the remainder of this year, probably to about 4.5% by December and to around 2% in the second half of 2024.”

He added: “We continue to think that the MPC will not raise Bank rate all the way to the near 6% level priced-in by markets before today’s data; for now, our base case remains Bank rate peaks at 5%.”

The government will underwrite a £1.5bn loan guarantee to Jaguar Land Rover (JLR) after a mass cyber attack forced a shutdown.

JLR suspended production at its UK factories following the cyber attack on 31 August. The shutdown is expected to last until 1 October, leaving the largest UK carmaker’s suppliers in limbo.

The loan is expected to give suppliers some certainty amid the continued shutdown, as the £1.5bn will help bolster JLR’s cash reserves as it pays back companies in its supply chain.

The government will give its backing to the loan through the Export Development Guarantee (EDG), a financial support mechanism aimed at helping British companies that sell their goods overseas.

JLR shutdown extended

The £1.5bn loan, from a commercial bank, will be paid back over five years.

“Following our decisive action, this loan guarantee will help support the supply chain and protect skilled jobs in the West Midlands, Merseyside and throughout the UK,” Business Secretary Peter Kyle said.

Chancellor Rachel Reeves added: “Jaguar Land Rover is an iconic British company which employs tens of thousands of people – a jewel in the crown of our economy.

“Today we are protecting thousands of those jobs with up to £1.5bn in additional private finance, helping them support their supply chain and protect a vital part of the British car industry.”

Rachel Reeves, during a visit to Jaguar Land Rover in Birmingham with Prime Minister Sir Keir Starmer. File pic: PA

As a result of the attack, production was halted across the car-making supply chain, with thousands of staff off work.

More than 33,000 people work directly for JLR in the UK, many of them on assembly lines in the West Midlands, the largest of which is in Solihull, and a plant at Halewood on Merseyside.

An estimated 200,000 more are employed by several hundred companies in the supply chain, who have faced business interruption with their largest client out of action.

Inside factory affected by Jaguar Land Rover shutdown

Ministers have had daily contact with JLR and cyber experts following the attack as the company attempts to restart production at its UK factories.

Unions and politicians have warned that small suppliers producing parts for JLR could collapse as a result of the shutdown unless they receive urgent financial support.

This week, Mr Kyle met workers and bosses at Webasto, which makes sunroofs for JLR.

Read more:

Small firms reliant on JLR have ‘weeks left’ before damage ‘untenable’

Harrods customers’ details stolen in IT systems breach

Hackers claim to have stolen pictures, names and addresses of children in nursery firm cyber attack

Peter Kyle visits the JRL supplier Webasto in Sutton Coldfield in the West Midlands. Pic: PA

The brand has the largest supply chain in the UK automotive sector, which employs around 120,000 people and is largely made up of small and medium-sized businesses.

The government’s promise of underwriting the JLR loan has been praised by the Unite union, whose general secretary Sharon Graham said the loan was “an important first step and demonstrates that the government has listened to the concerns raised in meetings with Unite over recent days”.

Are we in a cyber attack ‘epidemic’?

She added: “This is exactly what the government should be doing, taking action to protect jobs.

“The money provided must now be used to ensure job guarantees and to also protect skills and pay in JLR and its supply chain.”

Labour MPs are gathering in Liverpool for the annual party conference as Sir Keir Starmer attempts to mount a fightback against dire polling and threats to his leadership.

The prime minister said he will use the four-day event to show Labour can be an alternative to the “toxic divide and decline” offered by Reform UK, describing this as “the fight of our times”.

Sir Keir is under pressure after two separate polls predicted Nigel Farage’s party will win the next general election as voters turn their backs on mainstream politics.

It is the latest bit of bad news for the embattled prime minister, who has faced a month of scandals surrounding his top team alongside speculation Greater Manchester Mayor Andy Burnham could mount a leadership challenge.

Sir Keir Starmer and his wife arriving ahead of the Labour Party Conference. Pic:PA

Speaking from the conference venue on Saturday night, Sir Keir said the next few days are a “really big opportunity to make our case to the country, make it absolutely clear that patriotic national renewal is the way forward, not the toxic divide and decline that we get with Reform”.

He later insisted he could “pull things around”, telling The Sunday Times: “It is the fight of our times and we’ve all got to be in it together. We don’t have time for introspection, we don’t have time for navel-gazing.

“You’ll always get a bit of that at a Labour Party conference, but that is not going to solve the problems that face this country.

“Once you appreciate the change – in the sense of the division that Reform would bring to our country and the shattering of what we are as a patriotic country – then you realise this is a fight which in the end is bigger than the Labour Party.”

Much of the next four days is likely to be dominated by discussions on how exactly Labour could beat Reform – and whether Sir Keir is the man for the job.

PM’s future in doubt

There has been rampant speculation Mr Burnham could mount a leadership challenge after he made a series of high-profile interventions this week, criticising the direction of the government and claiming Labour MPs had asked him to stand.

The so-called “King of the North” has many hurdles to overcome before that could be a possibility – he would have to win a seat in Westminster through a by-election if one became available, then get 80 colleagues to back him.

One MP told Sky News that lots of backbenchers are “reluctantly coming to the conclusion” that Sir Keir’s downfall is a “not a matter of if, but when” – citing Mr Burnham or Health Secretary Wes Streeting as possible replacements

However they stressed that they did not want to see the prime minister go and hope he can turn things around ahead of the local elections in May.

Can Andy Burnham take on the bond markets?

Two-child benefit cap speculation

Many MPs want the prime minister to use the conference to set out a positive vision that offers hope for the future – saying his rhetoric on “tough choices” during the first 12 months backfired with the public.

The boss of Unite, Labour’s biggest union funder, has threatened to break its link with the party unless it changes direction.

In a signal the leadership is listening, there have been hints from senior ministers that the government could use the conference to scrap the controversial two-child benefit cap.

The limit is opposed by over 100 Labour MPs, both of Labour’s deputy leadership candidates and other senior party figures such as Mr Burnham and former prime minister Gordon Brown.

Two MPs who were suspended for rebelling over the measure last year – John McDonnell and Aspana Begum – had the whip reinstated on Friday.

Mr McDonnell, the shadow chancellor under Jeremy Corbyn, said he hopes “this is a signal the government has decided to scrap the cap”.

Key announcements

Sir Keir’s allies rallied round him ahead of the conference, with Business Secretary Peter Kyle claiming the prime minister received a “rapturous reception” at events he has been speaking at on Saturday.

Sir Keir will address the conference on Tuesday but there will be speeches from cabinet ministers throughout the event, with Chancellor Rachel Reeves to speak on Monday.

YouGov: Farage set to be next PM

The opening day will kick off with a pledge from Housing Secretary Steve Reed to construct three new towns before the next election, in Tempsford in Bedfordshire, Leeds South Bank, and Crews Hill, north London.

In one of a number of announcements overnight, the government also said that it will underwrite a £1.5bn loan guarantee to Jaguar Land Rover as it continues to face a shutdown following a mass cyber attack.

Meanwhile, Chancellor Rachel Reeves told The Times she is pushing for a new youth mobility scheme and an improved trading relationship with the European Union in a bid to reduce the need for tax rises in the forthcoming budget.

And Home Secretary Shabana Mahmood signalled a major change in immigration policy, telling The Sun on Sunday she would “reset” immigration laws so foreigners must prove their social worth before being allowed to settle in Britain.

The boss of Unite, Labour’s biggest union funder, has threatened to break its link with the party unless it changes direction.

Sharon Graham, general secretary of the union, told Sky News that, on the eve of a crucial party conference for the prime minister, Unite‘s support for Labour was hanging in the balance.

She told Sunday Morning With Trevor Phillips: “My members, whether it’s public sector workers all the way through to defence, are asking, ‘What is happening here?’

Sharon Graham has been a long-time critic of Sir Keir Starmer. Pic: PA

“Now when that question cannot be answered, when we’re effectively saying, ‘Look, actually we cannot answer why we’re still affiliated’, then absolutely I think our members will choose to disaffiliate and that time is getting close.”

Asked when that decision might be made, she cited the budget, on 26 November, as “an absolutely critical point of us knowing whether direction is going to change”.

Ms Graham, who became leader in 2021, has been a long-time critic of Sir Keir Starmer‘s agenda, accusing him of lacking vision.

The union has campaigned against his decision to cut winter fuel allowance for pensioners – which was later reversed – and has called for more taxes on the wealthy.

But the firm threat to disaffiliate, and a timetable, highlights the acute trouble Sir Keir faces on multiple fronts, after a rocky few months which have seen his popularity plummet in the polls and his administration hit by resignations and scandals.

There is now open discussion about his leadership, with Andy Burnham, the mayor of Greater Manchester, claiming he’s been urged by MPs to mount a challenge.

Burnham: Labour leadership ‘not up to me’

Unite has more than a million members, the second-largest union affiliated to Labour. It donates £1.5m a year from its membership fees to the party.

The union did not make an additional donation to Labour at the last election – as it has done previously – but was the biggest donor to its individual MPs and candidates. It has donated millions to the party in the past.

Any decision to disaffiliate would need to be made at a Unite rules conference; of which the next is scheduled for 2027, but there is the option to convene emergency conferences earlier.

Just 15 months into Sir Keir’s premiership, in which he has promised to champion workers’ rights, Ms Graham’s comments are likely to anger the Labour leadership.

Sir Keir Starmer has seen his popularity plummet in the polls in recent months. Pic: AP

Read more: Now is moment of ‘maximum danger’ for Starmer, Harriet Harman warns

Unite, earlier this year, voted to suspend former deputy prime minister Angela Rayner of her union membership because of the government’s handling of a long-running bin strike in Birmingham.

Ms Graham has described the left-wing party being launched by Jeremy Corbyn as a “sideshow” and has brushed off speculation of a leadership challenge by Mr Burnham.

This summer, she said if Unite dropped support from Labour it would “focus on building a strong, independent workers’ union that was the true, authentic voice for workers”.

The annual Labour Party conference kicks off in Liverpool from Sunday.

As a union affiliated with Labour, Unite has seats on the party’s ruling national executive committee and can send delegates to its annual conference.

Watch the full interview with Sharon Graham on Sunday Morning With Trevor Phillips from 8.30am on Sky News

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment12 months ago

Environment12 months agoHere are the best electric bikes you can buy at every price level in October 2024