The UK’s Supreme Court is set to deliver a landmark ruling today that could have billion-pound consequences for banks and impact millions of motorists.

The essential question that the country’s top court has been asked to answer is this: should customers be fully informed about the commission dealers earn on their purchase?

However, the Supreme Court is only considering one of two cases running in parallel regarding the mis-selling of car finance.

Here is everything you need to know about both cases, and how the ruling this afternoon may (or may not) affect any future compensation scheme.

PA file pic

What is the Supreme Court considering?

The Supreme Court case concerns complaints related to the non-disclosure of commission. This applies to 99% of car finance cases.

When you buy a car on finance, you are effectively loaned the money, which you pay off in monthly instalments. These loans carry interest, organised by the brokers (the people who sell you the finance plan).

These brokers earn money in the form of a commission (which is a percentage of the interest payments).

Last year, the Court of Appeal ruled in favour of three motorists who were not informed that the car dealerships they agreed finance deals with were also being paid 25% commission, which was then added to their bills.

The ruling said it was unlawful for the car dealers to receive a commission from lenders without obtaining the customer’s informed consent to the payment.

However, British lender Close Brothers and South Africa’s FirstRand appealed the decision, landing it in the Supreme Court.

Pic: iStock

What does the second case involve?

The second case is being driven by the Financial Conduct Authority (FCA) and involves discretionary commission arrangements (DCAs).

Under these arrangements, brokers and dealers increased the amount of interest they earned without telling buyers and received more commission for it. This is said to have incentivised sellers to maximise interest rates.

The FCA banned this practice in 2021. However, a high number of consumers have complained they were overcharged before the ban came into force. The Financial Ombudsman Service (FOS) said in May that they were dealing with 20,000 complaints.

In January 2024, the FCA announced a review into whether motor finance customers had been overcharged because of past use of DCAs. It is using its powers to review historical motor finance commission arrangements across multiple firms – all of whom deny acting inappropriately.

The FCA also said it is looking into a “consumer redress scheme” that means firms would need to offer appropriate compensation to customers affected by the issue.

An estimated 40% of car finance deals are likely to be eligible for compensation over motor finance deals taken out between 2007 and 2021, when the DCAs were banned.

To find out how you can tell if you’ve been mis-sold car finance, read the following explainer from our reporter Megan Harwood-Baynes.

Read more from the Sky News Money blog

Pic: iStock

How does the ruling affect potential compensation?

In short, the Supreme Court ruling could impact the scale and reach that a compensation scheme is likely to have.

The FCA said in March that it will consider the court’s decision and if it concludes motor finance customers have lost out from widespread failings by firms, it is “likely [to] consult on an industry-wide redress scheme”.

This would mean affected individuals wouldn’t need to complain, but they would be paid out an amount dictated by the FCA.

However, no matter what the court decides, the FCA could go ahead with a redress scheme.

The regulator said it will confirm if it is proposing a scheme within six weeks of the Supreme Court’s decision.

Read more:

The scale of cheap Chinese imports flown into UK

Water firm faces £63m penalty over ‘excessive’ sewage spills

What impact could this have on lenders?

Analysts at HSBC said last year the controversy could be estimated to cost up to £44bn.

Alongside Close Brothers, firms that could be affected include Barclays, Santander and the UK’s largest motor finance provider Lloyds Banking Group – which organises loans through its Black Horse finance arm.

Lloyds has already set aside £1.2bn to be used for potential compensation.

The potential impact on the lending market and the wider economy could be so great that Chancellor Rachel Reeves is considering intervening to overrule the Supreme Court, according to The Guardian.

Treasury officials have been looking at the potential of passing new legislation alongside the Department for Business and Trade that could slash the potential compensation bill.

The Treasury said in response to the claim that it does not “comment on speculation” but hopes to see a “balanced judgment”.

Heathrow Airport has said it can build a third runway for £21bn within the next decade.

Europe’s busiest travel hub has submitted its plans to the government – with opponents raising concerns about carbon emissions, noise pollution and environmental impacts.

The west London airport wants permission to create a 3,500m (11,400ft) runway, but insists it is open to considering a shorter one instead.

January: Third runway ‘badly needed’

In January, Chancellor Rachel Reeves announced that the government supports a “badly needed” expansion to connect the UK to the world and open up new growth opportunities.

But London mayor Sir Sadiq Khan is still against a new runway because of “the severe impact” it will have on the capital’s residents.

Under Heathrow’s proposal, the runway would be constructed to the northwest of its existing location – allowing for an additional 276,000 flights per year.

The airport also wants to create new terminal capacity for 150 million annual passengers – up from 84 million – with plans involving a new terminal complex named T5XW and T5XN.

Terminal 2 would be extended, while Terminal 3 and the old Terminal 1 would be demolished.

The runway would be privately funded, with the total plan costing about £49bn, but some airlines have expressed concern that the airport will hike its passenger charges to pay for the project.

EasyJet chief executive Kenton Jarvis said an expansion would “represent a unique opportunity for easyJet to operate from the airport at scale for the first time and bring with it lower fares for consumers”.

Read more:

Who’s behind these Heathrow leaflets?

A long history of Heathrow’s third runway plans

Thomas Woldbye, the airport’s chief executive, said in a statement that “it has never been more important or urgent to expand Heathrow”.

“We are effectively operating at capacity to the detriment of trade and connectivity,” he added.

“With a green light from government and the correct policy support underpinned by a fit-for-purpose, regulatory model, we are ready to mobilise and start investing this year in our supply chain across the country.

“We are uniquely placed to do this for the country. It is time to clear the way for take-off.”

The M25 motorway would need to be moved into a tunnel under the new runway under the airport’s proposal.

Pic: Reuters

London mayor still opposed

Sir Sadiq says City Hall will “carefully scrutinise” the proposals, adding: “I’ll be keeping all options on the table in how we respond.”

Tony Bosworth, climate campaigner at Friends of the Earth, also said that if Sir Keir Starmer wants to be “seen as a climate leader”, then backing Heathrow expansion is “the wrong move”.

Earlier this year, Longford resident Christian Hughes told Sky News that his village and others nearby would be “decimated” if an expansion were to go ahead.

January: Village to be levelled for new runway

It comes after hotel tycoon Surinder Arora published a rival Heathrow expansion plan, which involves a shorter runway to avoid the need to divert the M25 motorway.

The billionaire’s Arora Group said a 2,800m (9,200ft) runway would result in “reduced risk” and avoid “spiralling cost”.

Transport Secretary Heidi Alexander will consider all plans over the summer so that a review of the Airports National Policy Statement can begin later this year.

Read more from Sky News:

US doctor in Gaza dares Trump’s envoy to witness hunger crisis

Conor McGregor loses appeal in civil sexual assault case

Scotland approves wind project days after Trump called them ‘con-job’

It also comes after Sky News reported on a Heathrow Airport-funded group sending leaflets supporting a third runway to thousands of homes across west London.

The group, called Back Heathrow, sent leaflets to people living near the airport, claiming expansion could be the route to a “greener” airport and suggesting it would mean only the “cleanest and quietest aircraft” fly there.

Who’s behind these Heathrow leaflets?

Opponents of the airport’s expansion said the information provided by the group is “incredibly misleading”.

Back Heathrow told Sky News it had “always been open” about the support it receives from the airport. The funding is not disclosed on Back Heathrow’s newsletter or website.

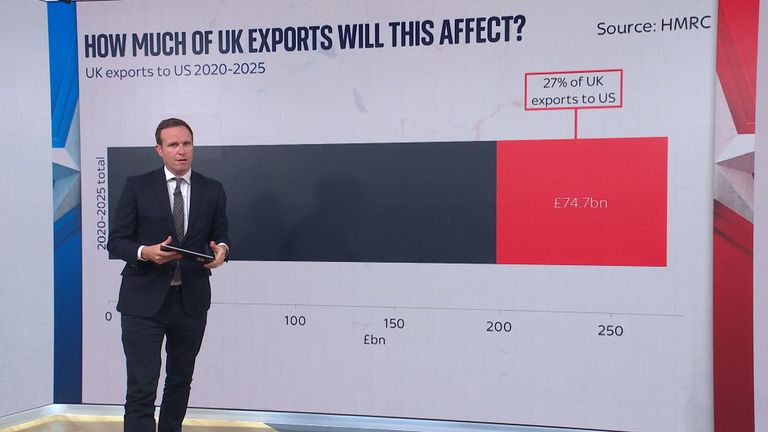

It is “Liberation Day” III – the third tariff deadline set by Donald Trump.

From today, countries without bilateral trade agreements face reciprocal tariffs – ranging from 25% to 50% – with a baseline of 15% to 20% for any not making a deal.

He has delayed twice, from April to July and from July to August, but hammered this date home in his trademark caps-on style: “THE AUGUST FIRST DEADLINE STANDS STRONG, AND WILL NOT BE EXTENDED. A BIG DAY FOR AMERICA!!!”

“Will not be extended” for anyone but Mexico, it seems. The country secured a 90-day extension at the last minute, with Mr Trump citing the “complexities” of the border.

Explained: The US-UK trade deal

By close of business on the eve of deadline, he had a handful of framework deals – some significant – including the UK (10%), the EU, Japan and South Korea (15%), Indonesia and the Philippines (19%), Vietnam (20%).

On the EU agreement, which he struck in Scotland, the president said: “It’s a very powerful deal, it’s a big deal, it’s the biggest of all the deals.”

But what happened to the “90 deals in 90 days” touted by the White House earlier this year?

The short answer is they were replaced by letters of instruction to pay a tariff set by the US.

How Trump 2.0 changed the world

Amid of flurry of late activity, the US played hardball with major trading partners like Canada.

“For the rest of the world, we’re going to have things done by Friday,” said US Commerce Secretary Howard Lutnick – the “rest of the world” meaning everyone but China.

There is, apparently, the “framework of a deal” between the world’s two largest economies, but talks between Washington and Beijing are continuing.

Read more US news:

Top Trump officials to visit Gaza

Heavy rain and flash floods batter east coast

Worker begs America for help

In terms of wins, he can claim some significant deals and point to his tariffs having generated an impressive $27bn (£20.4bn) in June, not bad for a single month.

But the legality of the approach is under siege – with the US Court of International Trade ruling that the “Liberation Day” tariffs exceeded the president’s authority, with enforcement paused pending appeal.

The deadline has stirred the pot, forcing a handful of deals onto the table. Whether they stick or survive legal scrutiny is far from settled.

But the playbook remains the same – threaten the world with trade chaos, whittle it down, celebrate the wins, and pray no one checks what’s legal.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike