Pension reforms could improve financial outcomes in decades – but there’s no feel good factor any time soon

There are many areas where the British economy struggles to compete with its counterparts, but in one sector it is up there with the best in the world: finance.

And when it comes to finance, there is perhaps one event above all others which are developed to celebrating the City of London: the Mansion House banquet in the middle of summer.

This is when the great and good of the square mile mingle with some of the policymakers, central bankers and regulators discussing the issues of the day.

There have been plenty of controversies in the past.

A few years ago the event was gatecrashed by a Greenpeace protestor who was manhandled quite roughly out of the event by the then City minister Mark Field.

The banquet was occasionally a place of tension during the financial crisis, when questions raged about the conduct of the banking system and, for that matter, their overseers in the UK authorities.

And given there are questions growing about the UK’s economic policies – the Bank of England‘s in the face of a cost of living crisis and the government’s plans in the face of major green investments by the US – this is relatively safe territory for the chancellor.

He and the prime minister like the City of London – they believe it is part of the answer to how the UK economy can thrive in the coming years. They see it as an answer to their problems rather than a problem in and of itself.

So it’s perhaps fitting that Jeremy Hunt has chosen this as the forum to announce some quite technical but also quite important changes to the way the pensions system works.

How will UK pensions change?

In brief, the plan is to encourage UK pension funds to put a bit more of their money into private companies.

At the moment only about a percentage point or so of pension funds’ money (and we’re talking here about the defined contribution schemes most people are now members of) goes into private, unlisted funds.

The vast, vast majority is instead invested in government bonds and in funds that shadow share prices in the UK and around the world.

By contrast, pension funds in Canada, Australia and Japan put far more of their money into private companies; indeed there are many UK private companies which have big stakes from overseas pension funds.

Chancellor on inflation: ‘We need to be patient’

The question is: why not UK pension funds? Part of the explanation comes down to various regulations which deter funds from anything but the very safest and cheapest investments.

The government’s argument is that by encouraging pension funds to put more of their cash into private firms, which often tend to see faster growth than unlisted firms, that should benefit those who have their money in UK pensions.

They think it could amount to an average increase in pensions (by the time you retire) of around £1,000 a year – though much of that depends on the future performance of these funds.

Read more:

Severe money market shift signals worse to come for finances

UK now the only G7 country with rising inflation

Average five-year mortgage rates above 6%

Thames Water faces uncertain future

There are some question marks over the policy. For an illustration of one of them, consider a certain private company which seems to fulfil the government’s criteria: it’s private, it’s unlisted, and its main owner is a Canadian pension fund. That company is Thames Water.

Some would say that by encouraging pension funds to invest in private equity and unlisted firms – many of which don’t have the same scrutiny as those on UK stock markets – pension funds may be taking on more risk than at present.

The Canadian pensioners with much of their money invested in Thames Water may have mixed feelings about the regulations allowing their funds to put their cash there. That being said, the second biggest owner of Thames is a UK pension fund – the Universities Superannuation Scheme.

‘UK in financial distress’

But the deeper issue is that while these changes to financial regulation could well improve outcomes in the following decades (they’re slow moving shifts in ownership that won’t have fully materialised until 2030) the government faces a more immediate set of crises.

Click to subscribe to The Ian King Business Podcast wherever you get your podcasts

The cost of living burden is falling heavily right now. Its popularity is flagging. And the room for a pre-election giveaway is diminishing with every week.

The chancellor signalled in his speech that fighting inflation will come before any plans for a tax cut. In other words, none of the above will help improve the feel good factor any time soon.

The Bank of England has signalled that a weakening labour market could yet trump rising global challenges to allow for more interest rate cuts in the near term.

Policymakers on the nine-member monetary policy committee (MPC) voted 7-3 to maintain Bank rate at 4.25%.

There was greater support than was expected for a cut.

The Bank had previously signalled that a majority on the committee were cautious about the effects of global instability – especially the on-off US trade war.

Money latest: What interest rate decision means for your money

But the minutes of the Bank’s meeting showed there was a greater focus on a rising jobless rate and evidence that employers are shedding jobs – indicating it had dominated the meeting.

It acknowledged, however, that there were potential challenges from the on-off US trade war and as a result of the Israel-Iran conflict.

The barrage of warheads has already resulted in double-digit percentage spikes to oil and natural gas prices in the space of a week.

“Interest rates remain on a gradual downward path,” governor Andrew Bailey said while adding that there was no pre-set path.

“The world is highly unpredictable. In the UK we are seeing signs of softening in the labour market. We will be looking carefully at the extent to which those signs feed through to consumer price inflation,” he added.

The Bank maintained its core message that it would take a “gradual” and “careful” approach.

“Energy prices had risen owing to an escalation of the conflict in the Middle East. The committee would remain vigilant about these developments and their potential impact on the UK economy,” the Bank said.

The rise in the UK’s jobless rate, along with recent data on payrolled employment, has been linked to a business backlash against budget measures, which kicked in in April, that saw employer national insurance contributions and minimum pay demands rise.

While a weaker labour market, including a fall in vacancies, could allow room for the Bank to react through further interest rate cuts, the spectre of war in the Middle East is now clouding its rate judgements.

The last thing borrowers need is an inflation spike.

The UK’s core measure of inflation peaked above 11% in the wake of Russa’s invasion of Ukraine – giving birth to what became known as the cost of living crisis.

Businesses facing fresh energy cost threat

Inflation across the economy was driven by unprecedented spikes in natural gas costs, which pushed up not only household energy bills to record levels but those for businesses too – with the cost of goods and services reflecting those extra costs.

Borrowing costs have eased, through interest rate cuts, as the pace of price growth has come down.

The rate of inflation currently stands at 3.4% but was already forecast to rise in the second half of the year before the aerial bombardments between Israel and Iran had begun.

LSEG data shortly after the Bank of England minutes were published showed that financial markets were expecting a quarter point cut at the Bank’s next meeting in August and at least one more by the year’s end.

Read more:

Why Middle East conflict poses new cost of living threat

Commenting on the Bank’s remarks Nicholas Hyett, investment manager at Wealth Club, said: “Conflict in the Middle East risks higher energy prices potentially pushing inflation higher – though calling the course of events there is almost certainly a mugs game, and the Bank has said that under current conditions it expects inflation to remain broadly at current levels for the rest of the year.

“The risk is that all the uncertainty leaves the Bank paralysed, with rates stuck at their current level,” he concluded.

A damning report into the faulty Post Office IT system that preceded Horizon has been unearthed after nearly 30 years – and it could help overturn criminal convictions.

The document, known about by the Post Office in 1998, is described as “hugely significant” and a “fundamental piece of evidence” and was found in a garage by a retired computer expert.

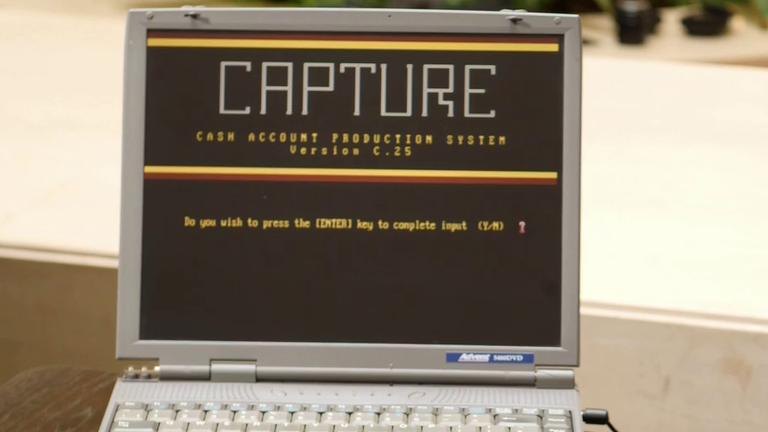

Capture was a piece of accounting software, likely to have caused errors, used in more than 2,000 branches between 1992 and 1999.

It came before the infamous faulty Horizon software scandal, which saw hundreds of sub-postmasters wrongfully convicted between 1999 and 2015.

What is the Capture scandal?

The “lost long” Capture documents were discovered in a garage by a retired computer expert who came forward after a Sky News report into the case of Patricia Owen, a convicted sub-postmistress who used the software.

Adrian Montagu was supposed to be a key witness for Pat’s defence at her trial in 1998 but her family always believed he had never turned up, despite his computer “just sitting there” in court.

Mr Montagu, however, insists he did attend.

He describes being in the courtroom and adds that “at some point into the trial” he was stood down by the barrister for Mrs Owen with “no reason” given.

Adrian Montagu was supposed to be a key witness for Pat’s defence

Sky News has seen contemporaneous notes proving Mr Montagu did go to Canterbury Crown Court for the first one or two days of the trial in June 1998.

“I went to the court and I set up a computer with a big old screen,” he says.

“I remember being there, I remember the judge introducing everybody very properly…but the barrister in question for the defence, he went along and said ‘I am not going to need you so you don’t need to be here any more’.

“I wasn’t asked back.”

The ‘lost long’ Capture documents were discovered in a garage

Sky News has reached out to the barrister in Pat Owen’s case who said he had no recollection of it.

‘An accident waiting to happen’

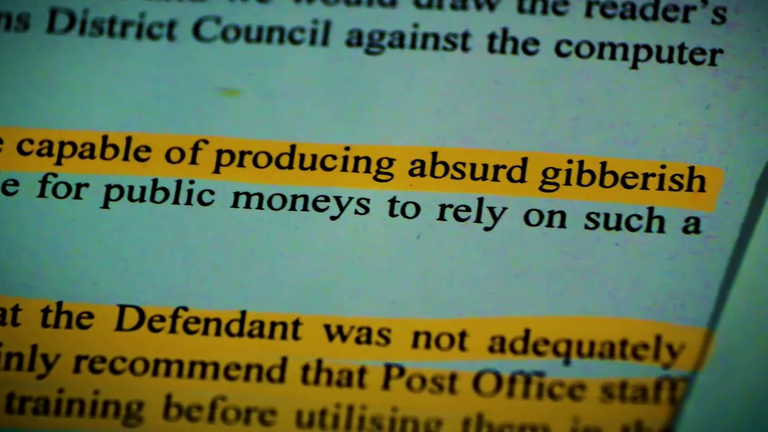

The report, commissioned by the defence and written by Adrian Montagu and his colleague, describes Capture as “an accident waiting to happen”, and “totally discredited”.

It concludes that “reasonable doubt exists as to whether any criminal offence has taken place”.

It also states that the software “is quite capable of producing absurd gibberish”, and describes “several insidious faults…which would not be necessarily apparent to the user”.

All of which produced “arithmetical or accounting errors”.

Sky News has also seen documents suggesting the jury in Pat Owen’s case may never have seen the report.

What is clear is that they did not hear evidence from its author including his planned “demonstration” of how Capture could produce accounting errors.

But flaws were found within it

Pat Owen was convicted of stealing from her Post Office branch in 1998 and given a suspended prison sentence.

Her family describe how it “wrecked” her life, contributing towards her ill health, and she died in 2003 before the wider Post Office scandal came to light.

Her daughter Juliet said her mother fought with “everything she could”.

“To know that in the background there was Adrian with this (report) that would have changed everything, not just for mum but for every Capture victim after that, I think is shocking and really upsetting – really, really upsetting.”

Pat died before the contents of the report came to light

The report itself was served on the Post Office lawyers – who continued to prosecute sub-postmasters in the months and years after Pat Owen’s trial.

‘My blood is boiling’

‘They knew software was faulty’

Steve Marston, who used the Capture software in his branch, was one of them – he was convicted of stealing nearly £80,000 in September 1998.

His prosecution took place four months after the Capture report had been served on the Post Office.

Steve says he was persuaded to plead guilty with the “threat of jail” hanging over him and received a suspended sentence.

He describes the discovery of the report as “incredible” and says his “blood is boiling” and he feels “betrayed”.

“So they knew that the software was faulty?,” he says. “It’s in black and white isn’t it? And yet they still pressed on doing what they did.

“They used Capture evidence … as the evidence to get me to plead guilty to avoid jail.

“They kept telling us it was safe…They knew the software should never have been used in 1998, didn’t they?”

Steve says his family’s lives were destroyed and the knowledge of this report could have “changed everything”.

He says he would have fought the case “instead of giving in”.

“How dare they. And no doubt I certainly wasn’t the last one…And yet they knew they were convicting people with faulty software, faulty computers.”

Steve’s prosecution took place four months after the Capture report had been served on the Post Office

The report is now with the Criminal Cases Review Commission, the body investigating potential miscarriages of justice, which is currently looking into 28 Capture cases.

A fundamental piece of evidence

Neil Hudgell, the lawyer representing more than 100 victims, describes the report as “hugely significant”, “seismic” and a “fundamental piece of evidence”.

“I’m as confident as I can be that this is a good day for families like Steve Marston and Mrs Owen’s family,” he says.

“I think (the documents) could be very pivotal in delivering the exoneration that they very badly deserve.”

He also added that “there’s absolutely no doubt” that the “entire contents” of the “damning” report “was under the noses of the Post Office at a very early stage”.

Pat Owen

He describes it as a “massive missed opportunity” and “early red flag” for the Post Office which went on to prosecute hundreds who used Horizon in the years that followed.

Read more from Sky News:

Sir Alan Bates attacks ‘kangaroo court’ Post Office scheme

Widow received compensation letter days after his death

“It is a continuation of a theme that obviously has rolled out over the subsequent 20 plus years in relation to Horizon,” he says.

“…if this had seen the light of day in its proper sense, and poor Mrs Owen had not been convicted, the domino effect of what followed may not have happened.”

What the Post Office said

Sky News approached the former Chief Executive of the Post Office during the Capture years, John Roberts, who said: “I can’t recall any discussion at my level, or that of the board, about Capture at any time while I was CEO.”

A statement from the Post Office said: “We have been very concerned about the reported problems relating to the use of the Capture software and are sincerely sorry for past failings that have caused suffering to postmasters.

“We are determined that past wrongs are put right and are continuing to support the government’s work and fully co-operating with the Criminal Cases Review Commission as it investigates several cases which may be Capture related.”

A Department for Business and Trade spokesperson said: “Postmasters including Patricia Owen endured immeasurable suffering, and we continue to listen to those who have been sharing their stories on the Capture system.

“Government officials met with postmasters recently as part of our commitment to develop an effective and fair redress process for those affected by Capture, and we will continue to keep them updated.”

Energy bill discounts of £150 will be extended to another 2.7 million households to help with fuel costs this winter.

It brings the number of households eligible for the Warm Home Discount up to just over 6 million, including 900,000 families with children, the Department for Energy Security and Net Zero (DESNZ) said.

The changes mean every bill payer on means-tested benefits will qualify, removing the high-cost-to-heat threshold in the current regulations.

It follows a government consultation on expanding the one-off payment to more people struggling with fuel poverty.

Prime Minister Keir Starmer said: “I know families are still struggling with the cost of living, and I know the fear that comes with not being able to afford your next bill.

“Providing security and peace of mind for working people is deeply personal to me as prime minister and foundational for the Plan for Change.

“I have no doubt that, like rolling out free school meals, breakfast clubs and childcare support, extending this £150 energy bills support to millions more families will make a real difference.”

The Conservatives criticised the move, saying the announcement will only cut bills for a quarter of households.

Andrew Bowie, the acting shadow energy secretary, criticised Labour’s green energy drive, claiming that it would increase bills for most people.

“Kemi Badenoch and I have been clear that net zero by 2050 is impossible without bankrupting Britain and making hard-working families worse off,” he said.

Read More:

Battle to convince MPs to back benefit cuts to more than three million households

Energy bosses clash over ‘postcode pricing’ proposals

Sky questions PM on winter fuel payment U-turn

Typical yearly energy bills are expected to fall by £129 from July, Ofgem has said.

However typical bills under the July to September 2025 price cap will still be 42% higher than in winter 2021/22, according to a House of Commons research briefing.

The Warm Home Discount scheme was introduced by the coalition government in 2011 to help people on low incomes with their fuel bills.

Adam Scorer, the chief executive of National Energy Action, said today’s announcement is “hugely positive news” but is “far from sturdy”.

“The rebate has only increased by a meagre £10 during a period in which energy bills have gone up by £500 a year and there is no clarity on the programme beyond the end of March next year,” he said.

“This announcement is good news for this winter, but the government needs to come up with a longer-term plan for providing deeper support in future for people who cannot afford a warm and healthy home.”

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike