Europe passes two big laws to make EV charging a whole lot better

The European Parliament adopted a set of rules today to improve the EV charging experience, focusing on easier payments, charging speed, and availability. In a separate move, the UK government is also currently proposing new rules for easier payments and charging station reliability.

Both sets of rules stand to improve the EV charging experience for Europeans and possibly the rest of the world.

Public charging has gotten a lot of attention lately as electric car sales continue to grow rapidly. Charging station operators are rushing to install chargers along major routes, trying to keep up with increasing demand from a ballooning EV fleet.

This has led to some issues in various territories, with confusing payment systems, less-than-desired charger reliability, and a lack of high-speed charging along some routes.

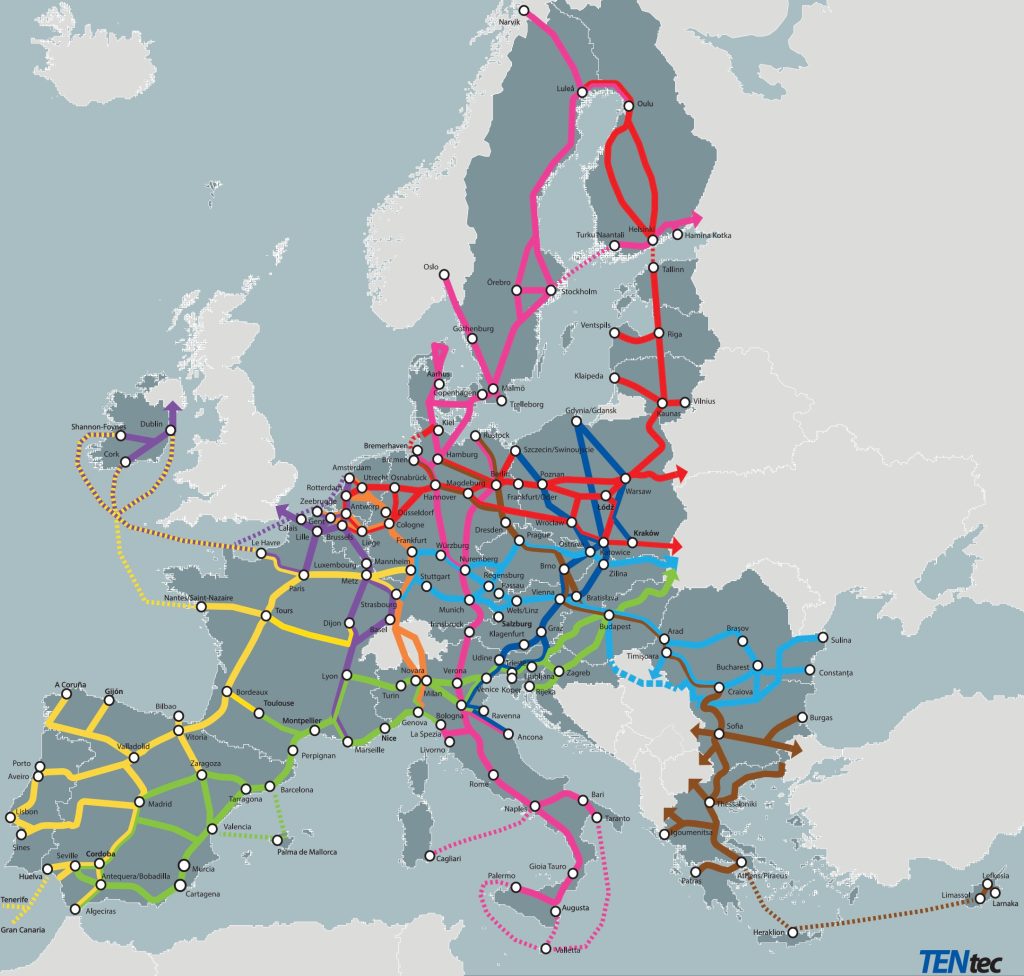

EU will mandate 400-600 kW charging every 60 km

Today, the European Parliament made a big move to improve the experience by approving new rules as part of its “Fit for 55” package, intended to reduce emissions by 55% by 2030. These regulations focus on expanding access to fast EV charging networks by mandating minimum speeds and distances between charging stations.

The rules cover Europe’s “TEN-T core network,” the main arterial road networks that cover all of Europe, comparable to the US interstate highway system.

Europe will mandate that, along these primary routes, chargers with at least 400 kW output must be placed at least every 60 km by 2026. In 2028, the minimum output will increase to 600 kW.

There are additional rules for truck and bus charging, with charging points required every 120 km at an output of 1.4-2.8 MW, depending on the road.

By 2027, Europe will develop a public database of these charging stations with information on availability, wait times, and pricing for different stations, regardless of network.

Beyond these charge station mandates, the new rules also mandate simpler charger payments. As-is, some networks require subscriptions or app downloads. But under these rules, customers must be able to pay with cards or contactless devices, and prices must be displayed to the customer.

Unrelated to EV charging, the EU also mandated cleaner maritime fuels, targeting an 80% reduction in greenhouse gas by 2050 and a requirement to use shore power while in ports. Both rules passed with massive majorities in the European Parliament.

UK wants to mandate 99% charging station reliability

Separately, the UK government has proposed rules focusing on charging experiences within the UK.

The headline feature of these rules is a mandate for 99% charging station reliability in the UK. According to a 2017 survey, 15% of EV charging stations in the UK were out of service, decreasing to 8% in 2019. The UK wants to lower this number to 1%.

Requiring 99% reliability could have benefits outside of the UK, as charging station manufacturers and station operators will have to step up their game and develop protocols for better reliability. The more territories that focus on reliability, the more likely these benefits might also bleed over to the ones that don’t.

The Netherlands has led the way in this respect with a 99% reliability target of its own, and the UK government specifically pointed to the Dutch as a reason for its 99% target.

This reliability focus comes with a requirement that charging station operators must provide a 24-hour helpline for when things go south.

In addition to the reliability mandates, the UK rules would adopt payment and database requirements that are similar to the EU rules, mandating per-kWh pricing, price displays, contactless payments, and live data on charge point availability. However, they only apply to fast chargers of 8 kW or above – slower public AC chargers are exempt.

These UK rules haven’t been officially adopted yet, but once they are, they will take one year to go into force. So the UK might get its rules before the EU if the government moves quickly enough.

Electrek’s Take

This is a good step forward, not just for Europeans but for electric car drivers everywhere. Big moves like this tend to spread, as can be seen with the similarities between EU and UK rules on charging and the UK’s specific callout of the Netherlands in its reliability target. So perhaps some of these requirements will percolate to other areas, and maybe we’ll get a little more charger reliability here in the US as a result.

Europe already has a simpler charging network than the US, as their chargers all rely on the same plug, Mennekes Type 2. Here in the US, we have two competing plugs – SAE CCS and Tesla Supercharger. This is one reason why Tesla could open up Superchargers to other cars in the EU earlier than in the US.

However, that’s changing in the US now that everyone is rushing to adopt Tesla’s NACS standard.

But Tesla has opposed pricing displays in the past. In 2020, California wanted to force manufacturers to display prices on stations, but Tesla’s minimalist Supercharger designs did not include a screen. Thus, the company opposed the idea. Tesla argued that since only its cars used its chargers and it can display all that information on the in-car display, it shouldn’t need to retrofit every charger with a display.

We expect there might be similar wrangling with the EU and UK rules, but the EU government has shown itself to be significantly less interested in tech industry lobbying than the US governments seem to be (see: Apple USB-C charging requirement, Meta GDPR fine, etc.). So Tesla may have its work cut out for it if it wants to convince the EU to let it keep its chargers looking the same.

FTC: We use income earning auto affiliate links. More.

Yes, Virginia, there are still great EV lease deals to be had in December. Hyundai continues to offer EV leases for under $200 a month, and the BMW i4 can be leased for the same price it was when the federal tax credit was still in effect. With 2025 models disappearing fast, this might be your last shot to snag a year-end lease deal on an EV. Check out the standouts below.

2025 Hyundai IONIQ 6 lease from $189/month

The 2025 Hyundai IONIQ 6 remains a fantastic deal: the IONIQ 6 SE Standard Range can be leased from $189 per month for 24 months with a $3,999 due at signing (12,000 miles per year). Its effective cost is just $356, and this month’s IONIQ 6 SE lease includes $13,000 in lease cash that you can’t get elsewhere. The offer is good until January 2.

Our friends at CarsDirect report that the SEL trim is actually a better deal at $239 with $3,999 at signing, with an effective cost of $406. Even though its MSRP is over $7,700 higher than the SE, it’s just $50 more a month to lease. The SE Standard Range has a range of 240 miles, whereas other styles have a range of up to 342.

As usual, offers vary according to location, and this is a regional offer based in California.

Click here to find a local dealer that may have the Hyundai IONIQ 6 in stock. –trusted affiliate link

2025 Hyundai IONIQ 5 lease from $189/month

Believe it or not, the 2025 Hyundai IONIQ 5 SE Standard Range RWD, which starts at $44,200, can still be leased through January 2 for $189 a month for 36 months (10,000 miles per year) with $3,999 due at signing. That works out to an effective monthly cost of about $300.

The IONIQ 5 SE RWD Standard Range offers an EPA-estimated 245 miles of range, and this particular offer is available in the Los Angeles and greater California metro areas (I’ve seen it at dealers in Carlsbad and Santa Monica, for example). And if you’re tempted by an upgrade, the SEL RWD trim is just $50 more per month under the same terms.

Click here to find a local dealer that may have the Hyundai IONIQ 5 in stock. –trusted affiliate link

2026 Subaru Solterra 5 lease from $299/month

In several regions, the 2026 Subaru Solterra Premium can be leased for $299 per month for 36 months, with a down payment of $2,799 due at signing, resulting in an effective monthly cost of $377. That makes it $95 per month cheaper to lease than a 2026 Toyota bZ, which is $472. (These figures are for California.)

A $500 loyalty discount is available to returning lessees. It doesn’t require a trade-in and can be transferred to household members. If you factor in the loyalty discount, the Solterra’s effective cost drops to $363. The offer ends January 2.

Subaru’s advertised lease prices are based on 10,000 miles a year, but that’s changeable. However, a larger mileage allowance will lower the EV’s residual value, making it more expensive.

Click here to find a local dealer that may have the Subaru Solterra in stock. –trusted affiliate link

2025 Ford Mustang Mach-E from $219/month

The 2025 Ford Mustang Mach-E can still be leased for $219 per month for 24 months with a $4,499 due at signing (10,500 miles per year) until January 5. In this configuration, the Mach-E has a range of up to 300 miles.

This is a regional offer for California, but the great deal isn’t limited to just that state. The example includes a total of $8,750 in lease cash; however, the catch is that if you opt for the lease cash, you have to decline the free home charger with installation or Ford’s $2,000 public charging credit.

Click here to find a local dealer that may have the Ford Mustang Mach-E in stock. –trusted affiliate link

2025 BMW i4 from $399/month

Remarkably, the 2025 BMW i4 is still leasing for the same price as it was when the federal tax credit was still in effect. In many regions, the eDrive40 can be leased for $399 for 36 months with $4,999 due at signing (10,000 miles per year). Its effective cost is just $538 per month, which is impressive when you consider that the i4’s retail price is over $60,000.

The offer, available until January 2, includes a $7,500 lease credit, and a $1,000 loyalty discount is also available for returning lessees. With the loyalty bonus, the i4’s effective monthly cost could be as low as $510.

In this configuration, the i4 has an EPA-estimated range of 318 miles. As before, BMW’s lease includes two years or 1,000 kWh of free charging with Electrify America.

Click here to find a local dealer that may have the BMW i4 in stock. –trusted affiliate link

The 30% federal solar tax credit is ending this year. If you’ve ever considered going solar, now’s the time to act. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

Kia now has one of the most affordable electric SUVs in Canada. The EV5 is now on sale, starting at $43,495 CAD.

Kia opens EV5 orders in Canada

The EV5 is the electric SUV we want in the US, but we will likely never see it. After opening online orders on December 4, Kia revealed prices for the entire 2027 EV5 lineup.

Surprisingly, buyers can choose from nine trims, with prices ranging from $43,495 CAD for the base Light model to $61,495 CAD for the flagship AWD GT-Line Limited edition.

Outside of the Light trim, all EV5 variants are offered with front-wheel or all-wheel drive. Upgrading to AWD costs an extra $2,500 CAD.

Likewise, all EV5 trims, except the Light variant, are powered by an 81.4 kWh battery, providing up to 460 km (285 miles) of driving range. The entry-level Light uses a 60.4 kWh battery, good for a driving range of up to 335 km (208 miles).

All EV5 models come with a built-in NACS port, nearly 30″ of screen space in a curved panoramic display, heated front seats, and Kia Connect with OTA updates.

The interior features Kia’s new Connect Car Navigation (CCNC) infotainment system with dual 12.3″ driver display and touchscreen navigation screens, plus a 5″ climate control screen. The setup includes wireless Android Auto and Apple CarPlay capabilities.

Kia grouped the EV5 trims into tiers based on what buyers are looking for. As expected, the Light FWD trim is the best value for your money.

For those looking for a little more driving range, the Wind FWD offers up to 460 km range, while the Wind AWD is built for Canada’s harsh winters. Both include a heat pump as standard.

2027 Kia EV5 prices and range by trim

Kia said the EV5 Land Rover trim is the best option if you’re looking for a little more out of the interior. The Land Rover trim adds a memory function to the driver’s seat, a heated steering wheel, a panoramic sunroof, a smart power tailgate, and 19″ wheels.

And then there’s the EV5 GT-Line, for those looking for added performance, a sporty new look inside and out, and driver-assistance features like lane-change assist.

| 2027 Kia EV5 trim | Starting Price (CAD) (FWD/AWD) | Battery | Target Range (FWD/ AWD) | Selling Points |

| Light traction | $43,495 | 60.4 kWh | 335 km | Entry-level price, standard battery life |

| Wind | $47,495 / $49,995 | 81.4 kWh | 460 km / 415 km | Long-life battery, heat pump |

| Land | $49,995 / $52,495 | 81.4 kWh | 460 km / 415 km | Panoramic roof, smart tailgate, V2L |

| GT-Line | $55,495 / $57,995 | 81.4 kWh | 460 km / 410 km | HDA2, FCA 2, ventilated seats, sporty style |

| GT-Line Limited | $58,995 / $61,495 | 81.4 kWh | 460 km / 410 km | Head-up display, RSPA 2, Harman Kardon, digital key |

The EV5 is now available to order in Canada, outside of the entry-level FWD Light variant, which is scheduled for the fourth quarter of 2026.

Despite the wait, Kia claimed the 2027 EV5 is going on sale as “Canada’s most affordable electric SUV,” starting $43,495.

For those in the US, don’t get your hopes up. Kia said the EV5 will be sold exclusively in Canada for the North American market.

FTC: We use income earning auto affiliate links. More.

Multiple outlets are reporting on Donald Trump’s apparent effort to change US regulations to bring tiny Japanese kei cars to the US, but there’s little reason to think that effort will be serious.

Convicted felon Donald Trump has directed former reality TV contestant Sean Duffy to examine how kei cars, a category of Japanese microcars, could be brought to the US, calling them “cute.”

The statement was made yesterday at the announcement of a fuel efficiency rollback, which will raise your fuel costs by $23 billion and is explicitly intended to make cars bigger and less efficient.

And so, simply by reading the preceding two sentences, you should understand how unserious this effort is. At the same moment that a new proposal was announced to reduce fuel efficiency targets by a third, the same person who is trying to increase your fuel costs and make cars bigger and less efficient apparently also wants tiny efficient vehicles in the US. How does that make sense?

If Trump did know anything about how the auto industry works, he would not speak about making cars smaller at an event to announce rules explicitly intended towards making cars bigger – these are not compatible thoughts, and betray a lack of understanding of the reason he was even in the room to begin with.

Further, in addition to yesterday’s effort to remove CAFE rules, the EPA is currently trying to roll back President Biden’s improved exhaust standards which included a recognition of vehicle sizes becoming too large and a desire to reduce SUV/truck market share, and Mr. Trump is trying to place a 15% tariff on all Japanese goods, meaning higher prices for Americans if these cars were to come to the US.

Thinking more deeply about the reason why Mr. Trump might have mentioned kei cars to begin with, it is likely related to his recent trip to Japan. He went to Japan to negotiate an end to the unwise tariffs that he himself announced on one of America’s closest trading partners (despite that he does not have the Constitutional authority to apply them).

During that trip, he seems to have seen the tiny cars for the first time (or the first time he can remember, given his senility), and been enamored by them. So, he said yesterday (while flanked by Duffy, who showed apparent surprise as the flippant statement came out of his mouth):

“They’re very small, they’re really cute, and I said ‘How would that do in this country?’… But we’re not allowed to make them in this country and I think you’re gonna do very well with those cars, so we’re gonna approve those cars.”

-Donald Trump, upon witnessing a type of vehicle he should have known of by now, having spent 79 years globetrotting around this Earth, so how can he just be seeing this for the first time except if he’s senile.

Now, technically, here he says he wants the US to build the cars here, rather than import them from Japan. Kei cars are very popular in Japan, but rarer in other countries. Some other countries do have their own small cars similar to kei cars (for example, China’s 115-inch Wuling Mini EV), but Japan is where these vehicles have traditionally held the highest share.

There are various reasons for this, but one of them is due to the high density of Japanese cities. Kei cars are very space efficient for cities that are obsessed with space efficiency in a way that simply is not the case in the US.

Japanese cities are also connected by efficient, fast and reasonably-priced bullet trains, so getting from one side of the country to the other is easy to do without having to stuff the whole family into a vehicle that is under 134 inches long. And the regulatory regime in Japan has been built around kei cars, giving them certain advantages to incentivize their use.

Meanwhile, it’s nigh-impossible to convince any manufacturer to even build a sedan, hatchback or small SUV for the US, or to build any small-displacement vehicle. So this would require a massive change in consumer tastes, which of course manufacturers haven’t been particularly interested in leading, given they’ve been pushing SUVs for decades now.

That said, one of the reasons manufacturers have pushed SUVs is due to regulations which treat them more favorably than smaller vehicles. If those regulations were changed – and that’s what Trump and Duffy have floated – it could open the doors for smaller cars.

But there’s little reason to think either of them are serious about this, given the amount of work that would have to be done to change regulations, and given the work they’re currently doing to change the regulations in the exact opposite direction.

At a minimum, Federal Motor Vehicle Safety Standards (FMVSS) would have to change significantly. This is the set of rules governing safety requirements for all motor vehicles, with requirements for various vehicle classes that have been built and tweaked over time. And these requirements are tailored to how we build roads, infrastructure, and signage in this country, which differs from how these things are done in Japan or Europe or China.

While an effort to harmonize FMVSS and infrastructure standards with other countries would be admirable and has been desired for a long time in the auto industry, the enormity of the undertaking is much greater than a single flippant comment (from someone who probably doesn’t even know what FMVSS stands for).

And in fact, US regulations already do allow for exemptions to many regulations for low volume vehicles. So it already is possible to build small cars in the US, at least if you build fewer than 2,500 per year. So a startup focused on tiny cars could already get started here, and could have been selling kei-like cars all along (say, TELO, for example… but even they are offering a 152in truck, a foot and a half longer than a kei car, and with 500hp, about 8x more than a kei car).

But why haven’t manufacturers made these cars already, then?

Again, going back to the above, regulations and manufacturers have both pushed vehicle sizes larger and larger, and consumer tastes have happily followed, with US drivers wasting more and more money and space on larger and more polluting vehicles.

There is a perception that these larger vehicles are safer (even though they aren’t, and we are currently nearing an all-time high in pedestrian fatalities), so if vehicles keep getting bigger as a result of regulations allowing them to, US consumers will be afraid to buy a car that’s even smaller than the smallest available today. And yesterday’s proposed rule explicitly claims, in its third paragraph, that smaller cars are undesirable for this reason (without recognizing that it’s actually the larger cars that are responsible this problem).

Kei cars are also typically less powerful than the average American car, which even Duffy claimed himself, saying “are they going to work on the freeways? Probably not” (even though most vehicles use about ~20hp to sustain highway speeds).

And given that the American consumer has been sold the dream of buying a vehicle not for what it will be used for, but for every conceivable purpose they could ever dream of using any vehicle for, it seems unlikely that many will line up for a car that they have been told can’t even get on the freeway.

After all, Smart cars did exist in the US, as have various other small vehicles, but they’ve always been marginalized, because the whole culture, manufacturing base and regulatory regime around cars and roads has been built to advantage large vehicles, not small ones.

So despite that microcar enthusiasts like myself want to see tiny cars in the US, the idea that manufacturers will suddenly scale up production of these vehicles in the US seems extremely unlikely without a concerted effort to show that they are welcome here and that there will be a market for them.

And I’m not convinced that concerted effort will be undertaken by people who are currently undertaking a concerted effort to do the exact opposite, and by someone who seems to change his mind with whatever stupid nonsense he happened to see 12 seconds ago on fox. Companies don’t build manufacturing facilities based on the whims of an idiot, they do so with clear and consistent policy that they can be certain will last through a vehicle model’s development and sales timeline (typically around ~14 years from start of development to end of production).

So I don’t think this is going to happen. Prove me wrong, I will be happy to eat crow here.

The 30% federal solar tax credit is ending this year. If you’ve ever considered going solar, now’s the time to act. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024