Q2 2023 earnings preview: What to expect today")

Tesla (TSLA) Q2 2023 earnings preview: What to expect today

Tesla (TSLA) is about to release Q2 2023 financial results today, Wednesday, July 19, after the markets close. As usual, a conference call and Q&A with Tesla’s management are scheduled after the results.

Here we’ll take a look at what both the street and retail investors are expecting for the quarterly results.

Tesla Q2 2023 deliveries

As usual, Tesla already disclosed its Q2 vehicle delivery and production numbers, which drive the vast majority of the company’s revenue.

Earlier this month, Tesla confirmed that it delivered a new record of over 422,000 electric vehicles during the first quarter of the year.

Tesla also confirmed that it was able to produce a new record of nearly 480,000 vehicles during the quarter.

Delivery and production numbers are always slightly adjusted during earning results.

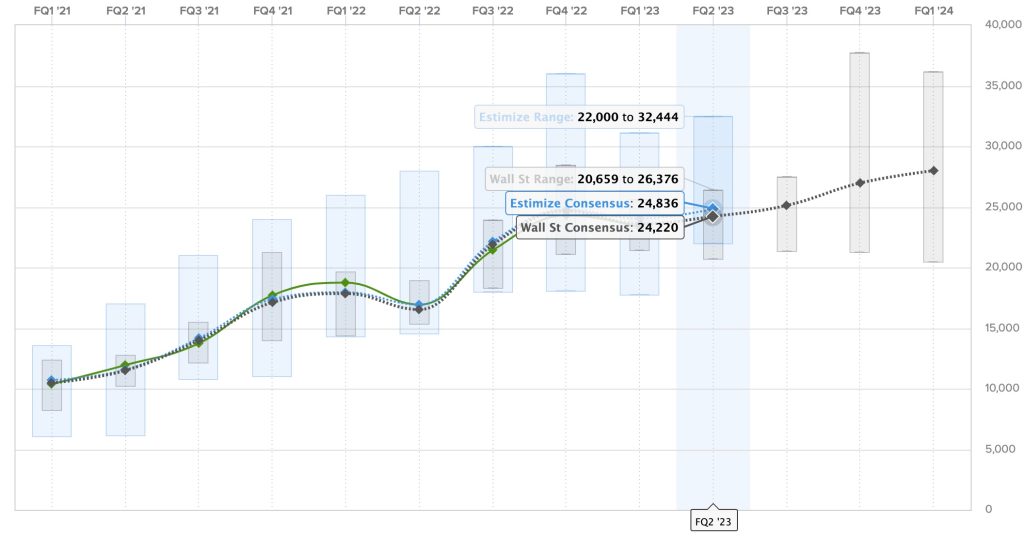

Tesla Q2 2023 revenue

For revenue, analysts generally have a pretty good idea of what to expect, thanks to the delivery numbers.

The Wall Street consensus for this quarter is $24.220 billion, and Estimize, the financial estimate crowdsourcing website, predicts a higher revenue of $24.836 billion.

This would represent a marginal increase over the previous quarter since even though Tesla achieved record deliveries, it had to slash prices to achieve it.

It would be a massive increase in revenue over the same period last year, but that wouldn’t be a great comparison since Tesla had to shut down Giga Shanghai during that time in 2022 temporarily.

Here are the predictions for Tesla’s revenue over the past two years, with Estimize predictions in blue, Wall Street consensus in gray, and actual results are in green:

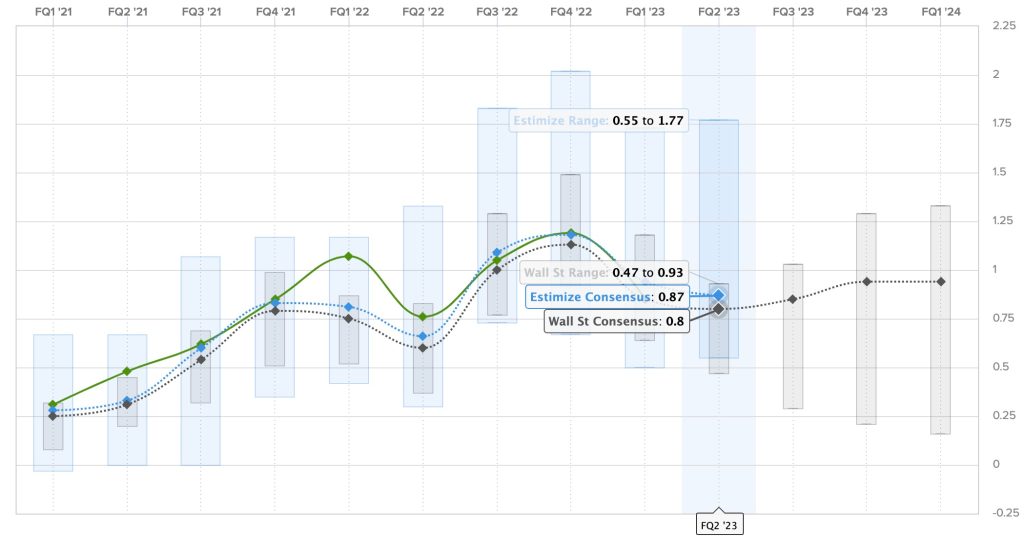

Tesla Q2 2023 earnings

Tesla always attempts to be marginally profitable every quarter as it invests most of its money into growth, and it has been successful in doing so over the last two years now.

For Q2 2023, the Wall Street consensus is a gain of $0.80 per share, while Estimize’s prediction is higher with a profit of $0.87 per share.

Despite anticipating record revenue, Wall Street expects earnings to be down from last quarter because of the previously mentioned price cuts,

Here are the earnings per share over the last two years, where Estimize predictions are in blue, Wall Street consensus is in gray, and actual results are in green:

Other expectations for the TSLA shareholder’s letter and analyst call

Much of the shareholder focus is likely going to be around gross margin and operational profitability at the current price level, which has dropped significantly throughout the year.

With Tesla Energy achieving record quarters that are slowly starting to have a small impact on Tesla’s broader performance, it might be a point of interest again this quarter.

But looking at top-voted shareholders’ questions, it looks like the Tesla shareholder community is more interested in looking into the future.

Here are the top five questions that Tesla is likely going to answer during the conference call:

- Has any automaker approached Tesla to license FSD?

- When will you get more information about our Cybertruck orders? Estimated delivery schedules, pricing, and specifications?

- Have you considered allowing FSD transferability as a lever to allow existing customers to upgrade to a new Tesla instead of being locked in to existing cars due to price of FSD?

- What is the status of the 4680 Cell? How far are you from the specs you laid out on battery day? When do you expect to achieve what you laid out on Battery Day?

- As you open the supercharger network in North America to other EVs, do you plan to accelerate anticipatory investments in supercharger expansion to avoid congestion, and how will you deal with long lead times to upgrade electric T&D services to these areas for multi-megawatt loads?

You can join us live on Electrek this evening for intensive coverage of Tesla’s Q2 2023 financial results starting at around 4 p.m. ET for the results and through the evening for news coming out of the conference call and results.

FTC: We use income earning auto affiliate links. More.

In the Electrek Podcast, we discuss the most popular news in the world of sustainable transport and energy. In this week’s episode, we discuss a big Tesla Robotaxi setback, the new Mercedes-Benz CLA EV, Bollinger is over, and more.

Today’s episode is brought to you by Climate XChange, a nonpartisan nonprofit working to help states pass effective, equitable climate policies. Sales end on Dec. 8th for its 10th annual EV raffle, where participants have multiple opportunities to win their dream model. Visit CarbonRaffle.org/Electrek to learn more.

The show is live every Friday at 4 p.m. ET on Electrek’s YouTube channel.

As a reminder, we’ll have an accompanying post, like this one, on the site with an embedded link to the live stream. Head to the YouTube channel to get your questions and comments in.

After the show ends at around 5 p.m. ET, the video will be archived on YouTube and the audio on all your favorite podcast apps:

We now have a Patreon if you want to help us avoid more ads and invest more in our content. We have some awesome gifts for our Patreons and more coming.

Here are a few of the articles that we will discuss during the podcast:

Here’s the live stream for today’s episode starting at 4:00 p.m. ET (or the video after 5 p.m. ET:

FTC: We use income earning auto affiliate links. More.

Environment

Segway’s latest E3 Pro smart e-scooter hits new $500 low, NIU Black Friday EV sale (47% off), Anker SOLIX, Lectric, Aiper, more

, Anker SOLIX, Lectric, Aiper, more")

Today’s Green Deals is another jam-packed Black Friday edition, with all the ongoing savings we’ve spotted up until today having been collected into our Black Friday Green Deals hub here for your one-stop shopping needs. Our headliner is Segway’s new feature-packed E3 Pro Electric Scooter with Apple Find My that is down at a new $500 low, with NIU’s full Black Friday EV sale following right behind with up to 47% taken off e-scooters and e-bikes starting from $279. There’s also Anker’s SOLIX C300X AC Portable Power Station and a bundle option at new low prices starting from $160, as well as Lectric’s newly launched 40% off e-bike accessory sale + increased 30% off e-bike extra batteries, a smart irrigation system, a battery jumper/power bank combo, and much more waiting for you below. And don’t forget about the hangover deals that are collected together at the bottom of the page (and also in our Black Friday Green Deals hub), like yesterday’s expanded Rad Power Black Friday Sale lineup, the Black Friday savings on Anker eufy smart security devices at new lows, and more.

Head below for other New Green Deals we’ve found today and, of course, Electrek’s best EV buying and leasing deals. Also, check out the new Electrek Tesla Shop for the best deals on Tesla accessories.

Segway’s feature-packed E3 Pro electric scooter with Apple Find My hits new $500 Black Friday low (Save $200)

Segway’s Black Friday Sale is in full gear and currently seeing hundreds in savings and plenty of returning and new low prices on its e-scooters and e-bikes. One such standout is Segway’s latest E3 Pro Electric Scooter down at $499.99 shipped, and which seems to have disappeared from Amazon’s marketplace. Carrying a $700 MSRP since launching back at the top of October, we’ve only seen this model given $100 price cuts in its launch deal and the brand’s Halloween and early Black Friday sales. Now, with things having ramped up with increased savings now that Black Friday is in full swing, you can score a larger-than-ever $200 markdown to a new all-time low price, giving you an advanced upgrade to your commute that I have been loving so far since getting one a short time ago.

I’ve been riding around Brooklyn for a short time now with my own Segway E3 Pro Electric Scooter and have been loving my experience so far, as it’s a MAJOR step up from the very basic E22 model I’ve had for short travels since 2020. While power has been significantly ramped up from its E2 Pro predecessor, this new generation still retains a fairly lightweight 40-pound design, which I am able (as a not-so-strong person) to carry easily with one hand/arm up and down my second-story stoop.

Segway’s E3 Pro comes bearing a 400W motor (with 800W peaking) alongside a 368Wh battery, the combination of which delivers up to 34 miles of commuting support for your travels at up to 20 MPH speeds. The regenerative brake paired with the brand’s SegRange Optimization tech really lends towards the extended travel times here, with safety taken into mind with the SegRide stability enhancement tech, the latest traction control system, turn signaling, RGB ambient lighting for nighttime journeys, and a bright headlight. What’s more, security is bolstered by the Apple Find My inclusion for those worried about tracking it down should theft (or forgetfulness) occur.

One thing I have really been enjoying, especially when riding over more pot-hole lined streets, is Segway’s E3 Pro’s dual elastomer suspension, which does a great job of smoothing out overall rides, while providing added cushioning when sudden, jolting sections of the road (or debris/trash) are driven over. Along with all those, there are also additional features, including the previously mentioned rear electronic regen brake getting a companion front drum brake, as well as 10-inch self-sealing jelly tires, an IPX5 water-resistant build, a 265-pound total payload, and a 3-inch full-color LED screen for setting adjustments.

Be sure to check out Segway’s full official Black Friday Sale while it lasts for a short while longer, which can save you hundreds at the best prices of the year starting from $150.

Score up to 47% Black Friday savings on NIU EVs, like the 2025 KQi 200F e-scooter at its $529 low (Reg. $799), more from $279

NIU’s Black Friday EV Sale is in full motion now, taking up to 47% off its lineup of e-scooters and e-bikes, like the KQi 200F Foldable Handlebar Electric Scooter for $529 shipped, which you can currently only find in a used condition at Amazon. This is one of the brand’s newer 2025 models that fetches $799 at full price, which dipped down to this rate for the first time earlier in the month before these Black Friday savings. Now, you’re getting another shot at this all-time low price with $270 savings, giving you a solid commuter that sits among the mid-range models from NIU.

You can view the full lineup of NIU’s Black Friday e-scooter and e-bike deals in our original coverage here.

Anker’s SOLIX C300X 90,000mAh portable power station + solar bundle option at new Black Friday lows from $160

As part of Amazon’s ongoing Black Friday Week Sale, and running parallel to Anker’s SOLIX Black Friday Sale, the brand’s official storefront is offering the C300X 90,000mAh Portable Power Station (misnamed on page as C200X) for $159.99 shipped. Normally going for $300 at full price, this alternate darker colorway beats out its standard grey colorway’s direct sale pricing by $40, with its Amazon pricing on that model also beaten out by the same amount. Discounts before October kept things above $189, with increased falls lower to 169 and $161 over last month and mid-way through this month, before this Black Friday deal dropped things to a new all-time low. Not only are you saving a total $140 here, but you’ll also be getting the best price tracked on the station’s 60W foldable solar panel bundle that’s down at a low of $240 shipped.

If you want to learn more about this model, be sure to check out our original coverage of these deals here, and be sure to also browse through Anker’s extended/expanded SOLIX Black Friday Sale in full here.

Best Fall EV deals!

- Velotric Nomad 2X e-bike (camo) with DELTA 3 Plus station: $3,048 (Reg. $3,298)

- Velotric Nomad 2X e-bike (sage or fig) with DELTA 3 Plus station: $2,948 (Reg. $3,298)

- Velotric Nomad 2X Multi-Terrain Full Suspension e-bike w/ $96 bundle: $2,299 (Reg. $2,399)

- Heybike Hero 750W Mid-Drive Carbon-Fiber All-Terrain e-bike: $2,299 (Reg. $3,099)

- Rad Power Radster Road Commuter e-bike: $1,999 (Reg. $2,199)

- Rad Power Radster Trail Off-Road e-bike: $1,999 (Reg. $2,199)

- Lectric XPedition 2.0 35Ah Cargo e-bike w/ $893 bundle: $1,999 (Reg. $2,761)

- Ride1Up TrailRush German Mid-Drive e-bike (first discount): $1,995 (Reg. $2,095)

- Heybike Hero 1,000W Carbon-Fiber All-Terrain e-bike: $1,899 (Reg. $2,599)

- Tenways Wayfarer e-bike with $277 bundle (launch deal): $1,899 (Reg. $2,199)

- Velotric Fold 1 Plus e-bike (gray or white) with DELTA 2 station: $1,898 (Reg. $2,198)

- Velotric Fold 1 Plus e-bike (mango or blue) with DELTA 2 station: $1,828 (Reg. $2,198)

- Velotric Summit 1 Versatile Multi-Terrain e-bike with $160 bundle: $1,799 (Reg. $1,999)

- Aventon Aventure 3 Smart All-Terrain e-bike (first discount): $1,799 (Reg. $1,999)

- Aventon Aventure 3 Smart Step-Through All-Terrain e-bike (first discount): $1,799 (Reg. $1,999)

- Lectric XP Trike2 750 Long-Range eTrike with $558 bundle: $1,799 (Reg. $2,357)

- Rad Power RadExpand 5 Plus Folding e-bike (lowest price): $1,699 (Reg. $1,899)

- Lectric XPedition 2.0 26Ah Cargo e-bike w/ $744 bundle: $1,799 (Reg. $2,543)

- Aventon Level 3 Step-Over Smart Commuter e-bike (first discount): $1,699 (Reg. $1,899)

- Aventon Level 3 Step-Through Smart Commuter e-bike (first discount): $1,699 (Reg. $1,899)

- Lectric XPeak 2.0 Long-Range Off-Road e-bike with $583 bundle: $1,699 (Reg. $2,282)

- Rad Power RadWagon 4 Cargo e-bike with extra battery: $1,599 (Reg. $1,799)

- Aventon Abound Cargo e-bike: $1,599 (Reg. $1,999)

- Ride1Up VORSA Modular Multi-Use e-bike: $1,595 (Reg. $1,695)

- Rad Power RadRunner Cargo Utility e-bike with extra battery: $1,499 (No pirce cut)

- Lectric XPeak 2.0 Standard Off-Road e-bike with $434 bundle: $1,499 (Reg. $1,933)

- Lectric XP Trike2 with $257 bundle: $1,499 (Reg. $1,756)

- Rad Power RadWagon 4 Cargo e-bike: $1,499 (Reg. $1,799)

- Aventon Aventure 2 All-Terrain e-bike: $1,499 (Reg. $1,999)

- Lectric XPedition 2.0 13Ah Cargo e-bike with $346 bundle: $1,399 (Reg. $1,745)

- Aventon Level 2 Commuter e-bike: $1,499 (Reg. $1,899)

- Rad Power RadRover 6 Plus Step-Thru Fat Tire e-bike: $1,399 (Reg. $1,599)

- Heybike ALPHA All-Terrain e-bike with $266 bundle: $1,299 (Reg. $1,699)

- Lectric XPress 750 Commuter e-bikes with $439 bundle: $1,299 (Reg. $1,703)

- Lectric XP4 750 LR Folding Utility e-bikes with up to $514 bundle: $1,299 (Reg. $1,813)

- Heybike Hauler Dual-Battery Cargo e-bike (new low): $1,299 (Reg. $1,899)

- Rad Power RadWagon 4 Cargo e-bike: $1,299 (Reg. $1,799)

- Heybike Mars 2.0 Folding Fat-Tire e-bike with extra battery: $1,199 (Reg. $1,848)

- Lectric XP Lite 2.0 JW Black LR e-bike with $449 bundle: $1,099 (Reg. $1,548)

- Heybike Hauler Dual-Battery Cargo e-bike with $89+ bundle: $1,099 (Reg. $1,413)

- Lectric XP4 Standard Folding Utility e-bikes with $326 bundle: $999 (Reg. $1,325)

- Lectric XP Lite 2.0 Long-Range e-bikes with $449 bundles: $999 (Reg. $1,448)

- Heybike Mars 2.0 Folding Fat-Tire e-bike with Black Friday gift: $999 (Reg. $1,499)

- Heybike Ranger S Folding Fat-Tire e-bike with Black Friday gift: $999 (Reg. $1,499)

- Segway E3 Pro Electric Scooter: $500 (Reg. $700)

Best new Green Deals landing this week

The savings this week are also continuing to a collection of other markdowns. To the same tune as the offers above, these all help you take a more energy-conscious approach to your routine. Winter means you can lock in even better off-season price cuts on electric tools for the lawn while saving on EVs and tons of other gear.

- Rad Power expands Black Friday e-bike lineup and increases savings to new lows starting from $999

- Anker’s eufy solar security cameras, smart locks, more get up to 50% Black Friday savings to new lows starting from $50

- EcoFlow Black Friday flash sale up to 69% off four power station and accessory bundles from $399

- GE’s 2-in-1 Profile smart ventless electric washer/dryer combo with heat pump at $2,000 (Reg. $2,700)

- Heybike drops new Mars 3.0 folding e-bike back to its $1,199 low during Black Friday sale for first time since launch

- Heybike’s new-gen Ranger 3.0 Pro folding commuter e-bike gets first post-launch cut to $1,399 low for Black Friday

- Tesla’s Universal Wall Connector with dual NACS + J1772 connectors and customizable 48A speeds retains $50 cut to $600

- Aiper’s Black Friday Sale offers up to 50% savings on robot pool cleaners, skimmers, monitors, more from $120

- Get up to 53% Black Friday savings + bonus discounts on Hiboy e-scooters and e-bikes at lows starting from $150

- Leviton’s 48A level 2 smart hardwired EV charger falls to new $479 Black Friday low (Save $270), more from $400

- Velotric’s Black Friday Sale switches gears with up to $750 increased savings and new lows starting from $999

- Upgrade off-road commutes and adventures with Lectric’s XPeak 2.0 e-bikes and up to $583 in FREE gear from $1,499

- Anker’s 4-day SOLIX Black Friday flash sale drops latest C2000 gen 2 power station to new $679 low ($820 off), more

- Anker’s popular PowerCore Reserve 192Wh power station with a pop-up light drops to $80 for Black Friday (Save $70)

- Upgrade your lawn care with up to 35% Black Friday savings on Mammotion RTK robot mowers from $649

- Save up to 49% on Govee’s smart appliances, like the electric kitchen composter at its $200 low ($103 off), more

- AeroGarden’s 6-plant Harvest Elite 360 indoor hydroponic system hits new $62 Black Friday low, more from $29

- Expand your Greenworks arsenal with up to 50% Black Friday savings on a massive lineup starting from $20

- Save up to 33% on Worx tools and lawn care equipment during Black Friday starting from $60

- Get up to 40% Black Friday savings on Husqvarna tools & robots at new lows starting from $217

- Schumacher’s 12A level 1 portable EV charger is perfect for stowing in trunks at a $110 Black Friday low (Save $50)

- Electrified Weekly – expanded and increased Black Friday savings of up to 80% from EcoFlow, Anker SOLIX, Segway, more

FTC: We use income earning auto affiliate links. More.

Tesla’s much-awaited entry into the Indian market has resulted in very slow sales to start, but it may not all be bad.

We’ve covered the years-long effort of Tesla to enter the Indian auto market. There have been a lot of intentions and fits and starts, but due to protectionist schemes in the country it never made a lot of sense for Tesla to enter.

That changed this year in March, when India waived EV import duties, allowing foreign firms to bring their cars in for sale. While India does have some strong local brands in Mahindra and Tata, this opened the gates to Chinese, German, Korean and American brands – namely, Tesla.

So far, other American companies have declined to bring their EVs to India, but Tesla opened its first showroom in Mumbai, India’s most populous city and financial capital, in July of this year. It opened a larger “Tesla Center” showroom in Gurugram, outside Delhi, this week.

So, Tesla is only getting started in India, but by all measures it has been an exceedingly slow start, according to the BBC.

Dealership data shows that Tesla has only sold “just over” 100 cars in India since July, an exceedingly low number by any measure – especially when considering the India is now the most populous country in the world, with a population of just under 1.5 billion.

Tesla’s rocky start included losing its head of Indian operations just before launching its first store, among a slew of other executive departures this year and last.

The numbers look a little less bad when comparing against EV sales in the country. While India has sold an impressive 2 million electric vehicles this year, the vast majority of them have been electric scooters.

Electric passenger cars are a much lower share at around 160k total unit sales this year so far, making up only around 3% of the passenger car market. And the majority of those are lower-cost domestic brands Mahindra and Tata or a growing section of Chinese challengers, with very few sales from overseas luxury brands.

Tesla could be included in that “luxury brand” list, largely due to the price of its imported vehicles. While the Model Y starts at $40k in the US, that price rises to 5,989,000 Rupees in India (~$67k USD). This is simply an unaffordable price for the vast majority of Indians – indeed, only around 1% of India’s auto sales are in the “luxury” category.

Further, EV infrastructure is not very well developed in the country. Tesla has one Supercharger in India, and two listed as “coming soon” in the Gurugram area. There are thousands of other charging points across India (and of course, drivers can charge overnight at home), but the number is still relatively low compared to the country’s population.

Meanwhile, other brands’ EV sales are growing well in India. The auto market as a whole has grown by about 13% this year in the developing country, but EV car sales have grown by 57% in the same period, rapidly outpacing the auto industry as a whole.

Much of that sales growth has been driven by Chinese EVs, which make up around a third of the market. That’s around ~60k Chinese EVs sold this year in India.

Even luxury German EVs from Mercedes, BMW and Audi have sold around 4,000 units so far this year, not a large number, but certainly dwarfing Tesla’s.

So while it’s tempting to look at Tesla’s poor numbers and make excuses about the size of the EV market, ability of Indians to afford luxury vehicles, or state of India’s charging network, it’s hard to compare that low ~100 sales number at any of the competition and label it as anything other than an extremely poor showing.

But, you do have to start somewhere, and the company is only a few months in. So we’ll have to see where it goes from here – though with the sales we’ve seen so far in Mumbai, entering the Delhi market is unlikely to forestall Tesla’s current global sales decline.

The 30% federal solar tax credit is ending this year. If you’ve ever considered going solar, now’s the time to act. To make sure you find a trusted, reliable solar installer near you that offers competitive pricing, check out EnergySage, a free service that makes it easy for you to go solar. It has hundreds of pre-vetted solar installers competing for your business, ensuring you get high-quality solutions and save 20-30% compared to going it alone. Plus, it’s free to use, and you won’t get sales calls until you select an installer and share your phone number with them.

Your personalized solar quotes are easy to compare online and you’ll get access to unbiased Energy Advisors to help you every step of the way. Get started here.

FTC: We use income earning auto affiliate links. More.

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024