Nigel Farage calls bank’s apology ‘a start’ but ‘no way near enough’ after account row

Nigel Farage has called on MPs to hold an inquiry into NatWest after one of the group’s banks, Coutts, closed his account.

The former UKIP and Brexit Party leader has claimed the elite bank took the action because his views did not align with the firm’s “values”.

But other media reports suggested it was down to his finances not reaching the company’s threshold, and Coutts insisted it did not close accounts “solely on the basis of legally held political and personal views”.

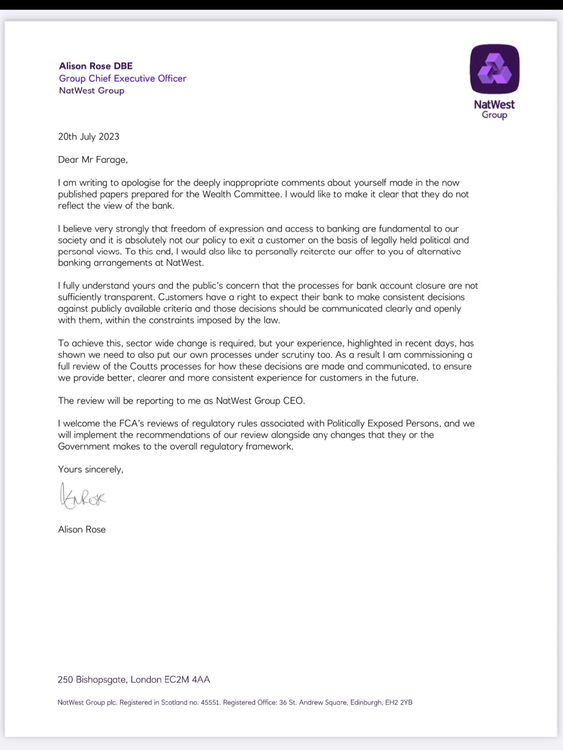

Earlier, the chief executive officer of NatWest, Alison Rose, wrote to Mr Farage offering him an apology, after he claimed to have a 40-page document that proved Coutts “exited” him because he was regarded as “xenophobic and racist” and a former “fascist”.

In the letter, she said “deeply inappropriate comments” had been made about him in documents prepared for the company’s wealth committee, and the remarks “did not reflect the view of the bank”.

She added: “I believe very strongly that freedom of expression and access to banking are fundamental to our society and it is absolutely not our policy to exit a customer on the basis of legally held political and personal views.”

The bank has now offered “alternative banking arrangements” at NatWest.

Speaking to reporters on Thursday night, Mr Farage called the apology “a start, but it is no way near enough”.

“It is always good to get an apology, particularly from somebody running a bank with 19 million customers, so thank you for the apology,” he added. “But it does feel ever so slightly forced.

“It also felt a bit like, ‘not me guv’.”

The apology letter written to Nigel Farage

The letter came as the Treasury announced new stricter measures on banks closing accounts to protect freedom of expression.

The government said the organisations will now have to inform customers of the reasons why they are closing accounts, and extend the notice period from 30 days to 90 – giving customers more time to challenge the decision or find a new bank.

Economic Secretary to the Treasury, Andrew Griffith, said: “Freedom of speech is a cornerstone of our democracy, and it must be respected by all institutions.

“Banks occupy a privileged place in society, and it is right that we fairly balance the rights of banks to act in their commercial interest, with the right for everyone to express themselves freely.”

Mr Farage praised the “superb” and “rapid reaction” of the government. But he also claimed his apology from Ms Rose only came about due to pressure from the Treasury.

The now-TV presenter added that wanted to know “what was said at a dinner” between Ms Rose and a BBC journalist.

Sky News has contacted Coutts and Mr Farage for comment.

Asked if he did have enough money to hold an account with Coutts, whose website states clients are “required to maintain at least £1m in investments or borrowing [mortgage], or £3m in savings”, Mr Farage said: “I have been a customer of the group for 43 years, I have been a customer of Coutts since 2014. At no point did anybody say you have to have this amount of money.

“These things are all discretionary [and] they were using this, frankly, as a mask to cover up the truth.

“This is not about money in the account, this is about the fact they don’t like me.”

Asked if he thought Ms Rose should resign, Mr Farage added: “I think rather than just saying right now [Ms Rose] ought to go, I think now what needs to happen is the Treasury Select Committee needs to reconvene, come out of recess, and lets give her the opportunity to tell us the truth.”

Read more:

What happened to Nigel Farage’s bank account?

Are banks allowed to close accounts?

Farage: ‘I was shocked with the vitriol’

In her letter, Ms Rose said she “fully understands” both Mr Farage’s and the public’s concerns that the processes for bank account closures were not “sufficiently transparent”, adding: “Customers have a right to expect their bank to make consistent decisions against publicly available criteria and those decisions should be communicated clearly and openly with them, within the constraints imposed by the law.”

She agreed that “sector-wide change” was needed but, following the incident with Mr Farage and Coutts, she would now commission a full review of the bank’s processes “to ensure we provide better, clearer and more consistent experience for customers in the future”.

In a further statement released after Sky News broke the story of the letter, Ms Rose reiterated her apology, but added: “It is not our policy to exit a customer on the basis of legally held political and personal views.

“Decisions to close an account are not taken lightly and involve a number of factors including commercial viability, reputational considerations, and legal and regulatory requirements.”

Representatives of the Bitcoin Policy Institute (BPI), a nonprofit Bitcoin advocacy organization, warned that US lawmakers have not included a de minimis tax exemption for Bitcoin transactions below a certain threshold.

“De Minimis tax legislation may be limited to only stablecoins, leaving everyday Bitcoin transactions without an exemption,” Conner Brown, BPI’s head of strategy, said on X, adding that the decision to exclude Bitcoin (BTC) is a “severe mistake.”

In July, Wyoming Senator Cynthia Lummis introduced a bill proposing a de minimis tax exemption for crypto transactions of $300 or less, with a $5,000 annual limit on tax-free transactions and sales.

The bill proposal also included tax exemptions for digital assets used for charitable donations and tax deferment for crypto earned through mining proof-of-work (PoW) protocols or staking to secure blockchain networks.

Allowing a tax exemption for small Bitcoin transactions would increase its use as a medium of exchange rather than just as a store of value asset, allowing a new financial system built on a Bitcoin standard, BTC advocates say.

The discussion around de minimis tax exemptions has also raised questions about whether such relief should apply to stablecoins, which are designed to maintain a stable value.

“Why would you even need a De Minimis tax exemption for stablecoins,” Marty Bent, founder of media company Truth for The Commoner (TFTC), wrote on X. “They don’t change in value. This is nonsensical.”

Cointelegraph reached out to BPI about the proposed legislation, but had not received a response at time of publication.

Related: Japan’s new crypto tax could wake ‘sleeping giant’ of retail investors

Bitcoin is gaining value, but it isn’t being used as peer-to-peer electronic cash

The Bitcoin white paper, authored by its pseudonymous creator Satoshi Nakamoto in 2019, describes Bitcoin as a “peer-to-peer electronic cash system.”

However, relatively high transaction fees, average block times of about 10 minutes, and capital gains taxes on Bitcoin stifle BTC’s use as a payment method for goods and services.

Many Bitcoin investors choose to hold BTC for the long term, sometimes borrowing fiat currency against their BTC holdings to pay expenses and fund everyday purchases.

The Bitcoin Lightning Network is a second-layer protocol designed for BTC payments, which works by locking a specific amount of BTC in a payment channel between two or more people.

Users connected through a payment channel can conduct multiple transactions offchain, with only the final net balance recorded on the Bitcoin ledger for settlement once the channel is closed.

This makes Bitcoin transactions faster and cheaper, as the users in the payment channel do not have to wait for new blocks to be mined or pay a network fee for each transaction between parties in the channel.

Magazine: The one thing these 6 global crypto hubs all have in common…

A US court is once again being asked to weigh in on maximal extractable value practices after a judge allowed new evidence to be added to a class-action lawsuit tied to a memecoin platform.

The judge granted a motion to amend and refile to include new evidence a class-action lawsuit against memecoin launch platform Pump.fun, the maximal extractable value (MEV) infrastructure company Jito Labs, the Solana Foundation, which is the nonprofit organization behind the Solana ecosystem, and others.

The motion said over 5,000 pieces of evidence in the form of internal chat logs were submitted by a “confidential informant” in September that were previously unavailable. The filing said:

“Plaintiffs assert that the logs contain contemporaneous discussions among Pump.fun, Solana Labs, Jito Labs, and others concerning the alleged scheme, and that they materially clarify the enterprise’s management, coordination, and communications.”

The lawsuit, originally filed in July, alleges that the Pump.fun platform deliberately misled retail investors by marketing memecoin launches as “fair,” but engaged in a scheme with Solana validators to front-run retail participants through maximal extractable value (MEV).

Maximal extractable value is a technique that involves reordering transactions within a block to maximize profit for MEV arbitrageurs and validators.

The plaintiffs allege that Pump.fun used MEV techniques to give insiders preferential access to new tokens at a low value, which were then pumped and dumped onto retail participants, who were used as exit liquidity by insiders.

Cointelegraph reached out to Burwick Law, the legal firm representing the plaintiffs, as well as Pump.fun, Jito Labs and the Solana Foundation, but did not receive any responses by the time of publication.

The lawsuit could set a precedent for MEV cases in the United States, as the ethics of the practice continue to be debated within the crypto industry and legal bodies struggle to define proper regulations about the highly technical subject.

Related: Pump.fun co-founder denies $436M cash out, claims it was ‘treasury management’

The MEV bot trial leaves questions unanswered

Anton and James Peraire-Bueno, the brothers accused of using a MEV trading bot to make millions of dollars in profit, went to trial in November in the US.

Prosecutors argued that the brothers tricked victims out of their funds, but defense attorneys said that they were executing a legitimate trading strategy and did not do anything illegal.

The jury struggled to reach a verdict in the case, and several jurors requested additional information to clarify the complexities surrounding the technical specifics of blockchain technology.

The case ended in a mistrial after the jury was deadlocked and failed to reach a verdict, highlighting the complexity of adjudicating legal disputes surrounding the application of nascent financial technology.

Magazine: Meet the onchain crypto detectives fighting crime better than the cops

Reports a female MSP had a secret recording device planted in her office by a member of her own staff are “completely and utterly unacceptable”, SNP leader John Swinney has said.

Scottish parliament officials are investigating the alleged bugging incident by a man, which is said to have taken place in 2023 at Holyrood.

The Scotsman newspaper reported the staffer is still involved with the SNP and moved on to work with a male MP after the issue came to light.

Sky News has yet to independently verify the details, but one senior party source with knowledge of events has said it is “100% true”.

The source alleges “the SNP did nothing; indeed he simply got moved and continued to be promoted by very senior members of executive”.

It is suggested the female MSP, who has not been publicly named, is liked, rated and respected by her colleagues.

The Scottish parliament building in Edinburgh. Pic: PA

First Minister Mr Swinney was stopped by reporters in Edinburgh on Thursday where he said he was “not familiar with all of the details… but that type of conduct is completely and utterly unacceptable”.

“Individuals are entitled to operate in an open and transparent environment that shouldn’t be subjected to that kind of behaviour,” he concluded.

Read more from Sky News:

Millions could see council elections delayed again

Bank of England rate cut to 3.75% following fall in inflation

MPs and MSPs employ staff directly, rather than the political party.

Sky sources confirmed the victims of the incident had to get counselling in the aftermath before suggesting the SNP “definitely has a woman problem”.

The source claims it is “not a one-off incident”, adding: “Women are habitually treated differently.”

An SNP spokesperson said: “The SNP has no involvement in the employment processes of parliamentarians. That is a confidential matter between elected members, employees, and Scottish parliament authorities.

“The reports outline a very traumatic situation for those involved and nobody should ever have to experience fear or harassment for doing their job.”

Scottish Labour deputy leader Jackie Baillie said: “These jaw-dropping revelations pose serious questions for the SNP top brass.

“It appears a grave breach of privacy and potentially criminal behaviour has been swept under the carpet by the SNP.

“Once again it looks like the SNP chose to close ranks and protect their own, rather than dealing with serious misconduct head-on.”

A spokesperson for the Scottish parliament said: “Each MSP is an employer in their own right and is responsible for managing staff welfare issues and employment disputes.

“Complaints about staff conduct are investigated by an independent adviser, and it is for the member to act on their findings accordingly.

“As a matter of standard practice, we do not comment upon or confirm any individual cases.”

-

Sports2 years ago

Sports2 years agoStory injured on diving stop, exits Red Sox game

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports3 years ago

Sports3 years agoButton battles heat exhaustion in NASCAR debut

-

Sports3 years ago

Sports3 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Environment3 years ago

Environment3 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment1 year ago

Environment1 year agoHere are the best electric bikes you can buy at every price level in October 2024