Nigel Farage calls bank’s apology ‘a start’ but ‘no way near enough’ after account row

Nigel Farage has called on MPs to hold an inquiry into NatWest after one of the group’s banks, Coutts, closed his account.

The former UKIP and Brexit Party leader has claimed the elite bank took the action because his views did not align with the firm’s “values”.

But other media reports suggested it was down to his finances not reaching the company’s threshold, and Coutts insisted it did not close accounts “solely on the basis of legally held political and personal views”.

Earlier, the chief executive officer of NatWest, Alison Rose, wrote to Mr Farage offering him an apology, after he claimed to have a 40-page document that proved Coutts “exited” him because he was regarded as “xenophobic and racist” and a former “fascist”.

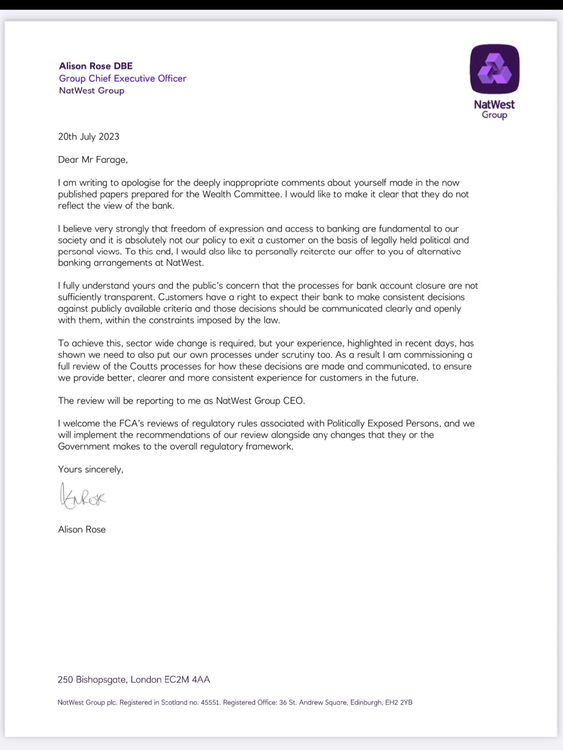

In the letter, she said “deeply inappropriate comments” had been made about him in documents prepared for the company’s wealth committee, and the remarks “did not reflect the view of the bank”.

She added: “I believe very strongly that freedom of expression and access to banking are fundamental to our society and it is absolutely not our policy to exit a customer on the basis of legally held political and personal views.”

The bank has now offered “alternative banking arrangements” at NatWest.

Speaking to reporters on Thursday night, Mr Farage called the apology “a start, but it is no way near enough”.

“It is always good to get an apology, particularly from somebody running a bank with 19 million customers, so thank you for the apology,” he added. “But it does feel ever so slightly forced.

“It also felt a bit like, ‘not me guv’.”

The apology letter written to Nigel Farage

The letter came as the Treasury announced new stricter measures on banks closing accounts to protect freedom of expression.

The government said the organisations will now have to inform customers of the reasons why they are closing accounts, and extend the notice period from 30 days to 90 – giving customers more time to challenge the decision or find a new bank.

Economic Secretary to the Treasury, Andrew Griffith, said: “Freedom of speech is a cornerstone of our democracy, and it must be respected by all institutions.

“Banks occupy a privileged place in society, and it is right that we fairly balance the rights of banks to act in their commercial interest, with the right for everyone to express themselves freely.”

Mr Farage praised the “superb” and “rapid reaction” of the government. But he also claimed his apology from Ms Rose only came about due to pressure from the Treasury.

The now-TV presenter added that wanted to know “what was said at a dinner” between Ms Rose and a BBC journalist.

Sky News has contacted Coutts and Mr Farage for comment.

Asked if he did have enough money to hold an account with Coutts, whose website states clients are “required to maintain at least £1m in investments or borrowing [mortgage], or £3m in savings”, Mr Farage said: “I have been a customer of the group for 43 years, I have been a customer of Coutts since 2014. At no point did anybody say you have to have this amount of money.

“These things are all discretionary [and] they were using this, frankly, as a mask to cover up the truth.

“This is not about money in the account, this is about the fact they don’t like me.”

Asked if he thought Ms Rose should resign, Mr Farage added: “I think rather than just saying right now [Ms Rose] ought to go, I think now what needs to happen is the Treasury Select Committee needs to reconvene, come out of recess, and lets give her the opportunity to tell us the truth.”

Read more:

What happened to Nigel Farage’s bank account?

Are banks allowed to close accounts?

Farage: ‘I was shocked with the vitriol’

In her letter, Ms Rose said she “fully understands” both Mr Farage’s and the public’s concerns that the processes for bank account closures were not “sufficiently transparent”, adding: “Customers have a right to expect their bank to make consistent decisions against publicly available criteria and those decisions should be communicated clearly and openly with them, within the constraints imposed by the law.”

She agreed that “sector-wide change” was needed but, following the incident with Mr Farage and Coutts, she would now commission a full review of the bank’s processes “to ensure we provide better, clearer and more consistent experience for customers in the future”.

In a further statement released after Sky News broke the story of the letter, Ms Rose reiterated her apology, but added: “It is not our policy to exit a customer on the basis of legally held political and personal views.

“Decisions to close an account are not taken lightly and involve a number of factors including commercial viability, reputational considerations, and legal and regulatory requirements.”

TRM Labs says the Embargo ransomware group has moved over $34 million in ransom-linked crypto since April, targeting US hospitals and critical infrastructure.

The cypherpunk ethos is retreating from the limelight, as institutions and centralized players take center stage, driving new narratives.

The new law will allow investment banks, which can underwrite companies, issue securities, and are institutionally focused, to hold BTC.

-

Sports3 years ago

Sports3 years ago‘Storybook stuff’: Inside the night Bryce Harper sent the Phillies to the World Series

-

Sports1 year ago

Sports1 year agoStory injured on diving stop, exits Red Sox game

-

Sports2 years ago

Sports2 years agoGame 1 of WS least-watched in recorded history

-

Sports2 years ago

Sports2 years agoMLB Rank 2023: Ranking baseball’s top 100 players

-

Sports4 years ago

Team Europe easily wins 4th straight Laver Cup

-

Sports2 years ago

Sports2 years agoButton battles heat exhaustion in NASCAR debut

-

Environment2 years ago

Environment2 years agoJapan and South Korea have a lot at stake in a free and open South China Sea

-

Environment2 years ago

Environment2 years agoGame-changing Lectric XPedition launched as affordable electric cargo bike